Dear Partners,

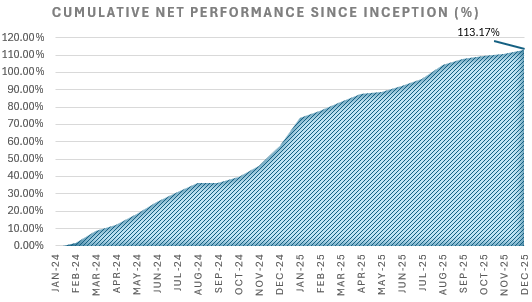

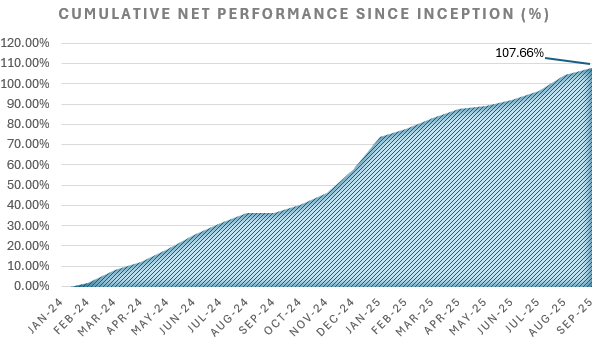

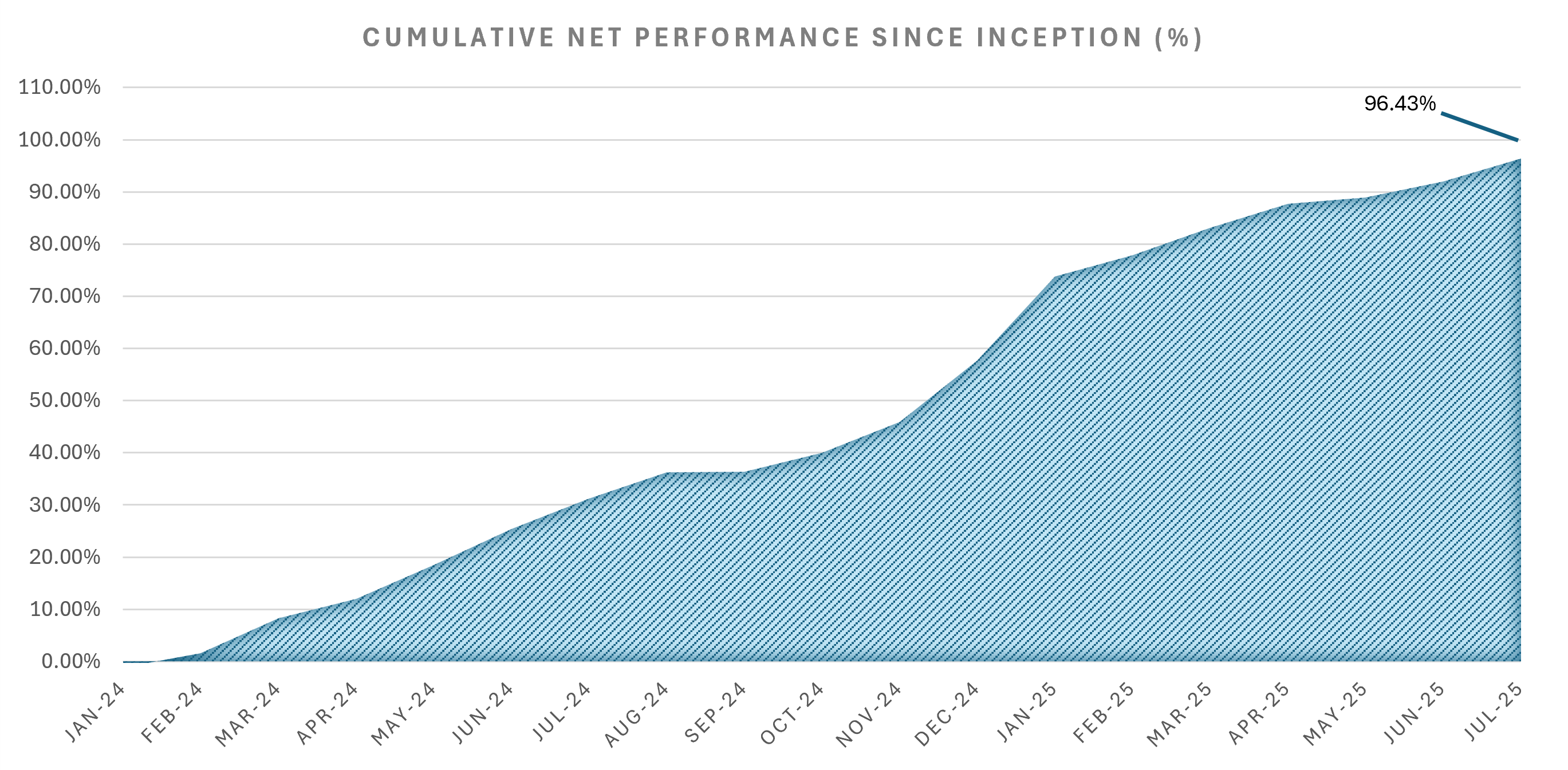

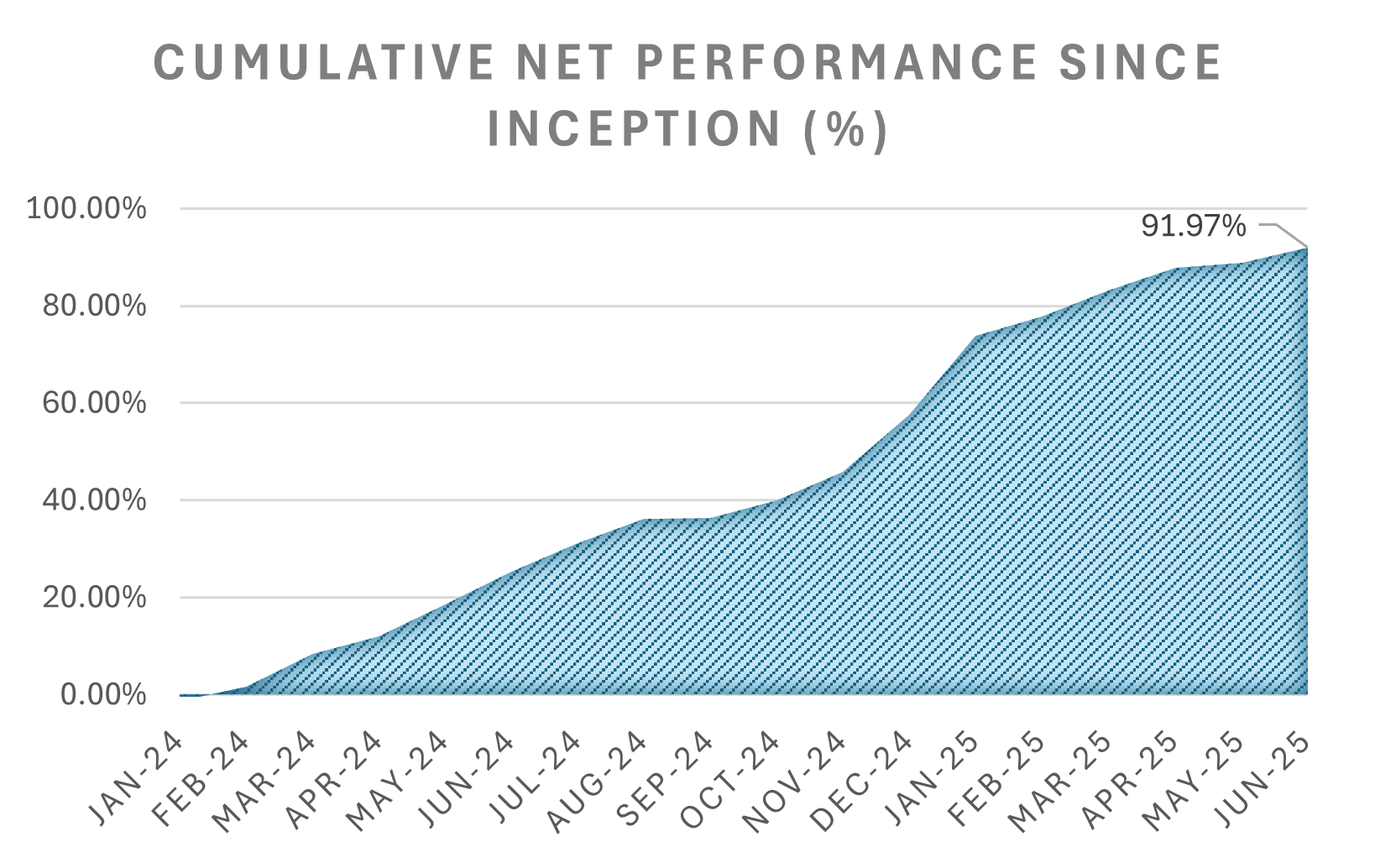

- The Constitution Real Estate Credit Fund closed Q1 2025 with strong performance, ending March with a net year-to-date return of 15.21%. The Fund held 12 positions at the end of March. We look forward to sharing April and May performance shortly, after which we’ll return to monthly updates.

-

Performance

- The fund generated a net return of 15.21% YTD through March 31, 2025.

- The fund generated a net return of 57.60% for FY 2024.

Net P/L Performance by Month Breakdown

Jan 2024

-1.21%

Feb 2024

2.85%

Mar 2024

6.59%

Apr 2024

3.38%

May 2024

5.84%

Jun 2024

5.78%

Jul 2024

4.68%

Aug 2024

3.83%

Sep 2024

0.06%

Oct 2024

2.69%

Nov 2024

4.11%

Dec 2024

8.02%

YTD 2024

57.60%

Jan 2025

10.27%

Feb 2025

2.18%

Mar 2025

2.25%

YTD 2025

15.21%

Portfolio Insights and Highlights

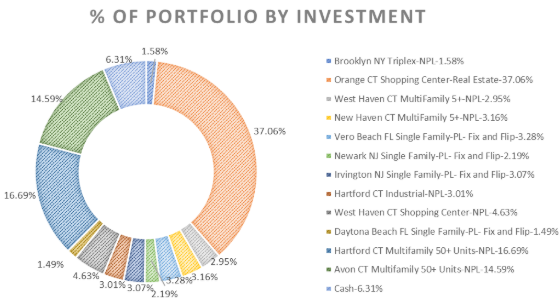

- As of March 31, the Fund holds 12 investments. Two new deals were added in February and March, and several existing positions are progressing toward resolution, with monetizations expected in Q3 and Q4.

- A few updates of note:

- Hartford, CT Multifamily NPL:

We’ve signed a stipulation agreement allowing the full payoff to be calculated as the new principal balance—including accrued interest. With a 24% default rate, this means we’re earning interest on interest, compounding returns for the Fund. The borrower must pay off by February 2026 or the Fund receives title to the properties. While we expect a payoff, resolution paths for NPLs often surprise even us. Either outcome is quite favorable. - Orange, CT Shopping Center:

The asset continues to generate consistent monthly cash flow for the fund despite not being fully leased. Just 4,000 square feet of space remains vacant. - Performing Loans:

Many of the Fund’s current performing loans are expected to pay off in the coming months. As capital is returned, we plan to recycle it into select NPL opportunities currently in our pipeline.

Market Thoughts

- The environment for acquiring nonperforming loans remains highly favorable.

- We continue to see a growing pipeline of distressed debt hitting the market as lenders adjust to the reality of higher-for-longer interest rates.

- Many sellers who previously held out for better pricing are now recognizing the need to transact at today’s lower values rather than waiting for rate relief that may not come soon.

- This shift is creating even more opportunities to acquire loans at attractive prices, and we expect this trend to accelerate.

- Mind you, the most interesting thing relative to many other cycles where the assets themselves are in some sort of distress, the assets today (except office) are mostly fine. High occupancy, low future supply, etc..

- The problems with most distress today were driven by sponsors overpaying and overlevering in the hopes that double digit rent growth would continue and rates would stay near zero. Unfortunately for them (fortunately for us) this has not been the case.

Distributions & Administration

- Q1 and Q2 distributions will be paid in mid-July. We’ll reach out to each investor via email with an estimate and ask whether you prefer a cash distribution or reinvestment. As a reminder, distributions below $1,000 will be retained until that threshold is met to avoid unnecessary fund transaction costs.

- K1s and 2024 Audit will be out by the end of June.

Looking Ahead

- We’ve built deep infrastructure in Connecticut—from data scraping and legal expertise to our own in-house property and construction management—and it's now near impossible for us to not know of a distressed loan in the state.

- We're now applying that same sourcing engine and playbook to New York City and Long Island. That includes the tech stack, the underwriting discipline, and most importantly, the ability to manage the asset all the way through resolution using our in-house team. Unlike many funds that outsource property management or servicing, we stay in control—because that’s where most of the value is created (or lost).

- We’ve already gone through a dozen full New York foreclosures, and let’s just say: if Connecticut is a 10K race, New York is a Tough Mudder in dress shoes. The timelines are longer and the bureaucracy is thicker. But we’re equipped for it. Our team knows the local rules, has relationships with key players, and knows how to operate effectively even in the least efficient environments.

- With broader geographic reach and better data than ever, we’re positioned to capture more of the region’s distressed debt opportunities.

- The environment continues to reward those with the tools and local expertise to act decisively. We’re well-positioned to take advantage of that and appreciate your continued partnership.

Learn more about investing in the Constitution Real Estate Credit Fund

-

Yours truly,

Ricardo, Kyle, and Joe

200 Pemberwick Road

Greenwich CT 06831

Invest@ConstLending.com

203-423-3534