There are several types of loans you can use to finance a rental property. In our experience as a private lender for over a decade, we see that DSCR loans tend to be the best choice for real estate investors because:

- You don’t have to submit tax returns or pay stubs: DSCR lenders mainly consider the property’s income and expenses. For instance, if a tenant pays $1,300 per month and the property’s expenses are $1,000, its DSCR is 1.3. This is what lenders consider — not your income or employment history.

- There’s no limit to the number of loans you can qualify for: Because DSCR lenders don’t assess your debt-to-income (DTI) ratio, you can qualify for unlimited rental loans as long as you meet the DSCR minimum. With conventional loans, qualifying becomes more difficult after your fourth mortgage due to DTI ratio limits.

- You can close faster: Since DSCR lenders don’t require extensive paperwork like banks do, borrowers can close faster. For instance, Constitution Lending can close in as little as 7 to 14 days, compared to the 40+ days it typically takes with a bank.

In this article, we review the top rental property lenders, factoring in their closing speed, loan terms, and dependability.

To begin, we walk through how we at Constitution Lending use our automated pricer and documents portal to help borrowers close quickly while securing some of the lowest interest rates available.

Use our automated pricer to pull an instant quote and see what terms you qualify for.

1. Constitution Lending: A Fast DSCR Lender Built to Help You Compete with Cash Buyers

Before founding Constitution Lending, we were real estate investors — buying, rehabbing, and renting properties.

Back then, most lenders we worked with were slow to respond and unreliable. They promised funding in 7 to 14 days but usually took over 40, costing us multiple properties that sold below market value to quick-cash buyers.

Another frustration was lenders backing out the week of — or even the day of — closing.

The problem? Many “lenders” were actually loan brokers who had to submit our application to the real lender and wait weeks for underwriting. They couldn’t confirm we qualified until we were near the closing date, often causing last-minute drama and rejections.

We created Constitution Lending to solve these issues.

Here’s what borrowers say about our lending process:

Let’s dive into detail about how Constitution Lending solves the two problems mentioned above.

We Use Our Automated Pricer and Online Documents Portal to Close Faster Than Other Lenders

As we mentioned above, most lenders promise a quick application and closing process but rarely deliver. That’s because they rely on inefficient, outdated systems — like endless emails and phone calls — to process loan applications.

We speed things up with our automated pricer and online documents portal.

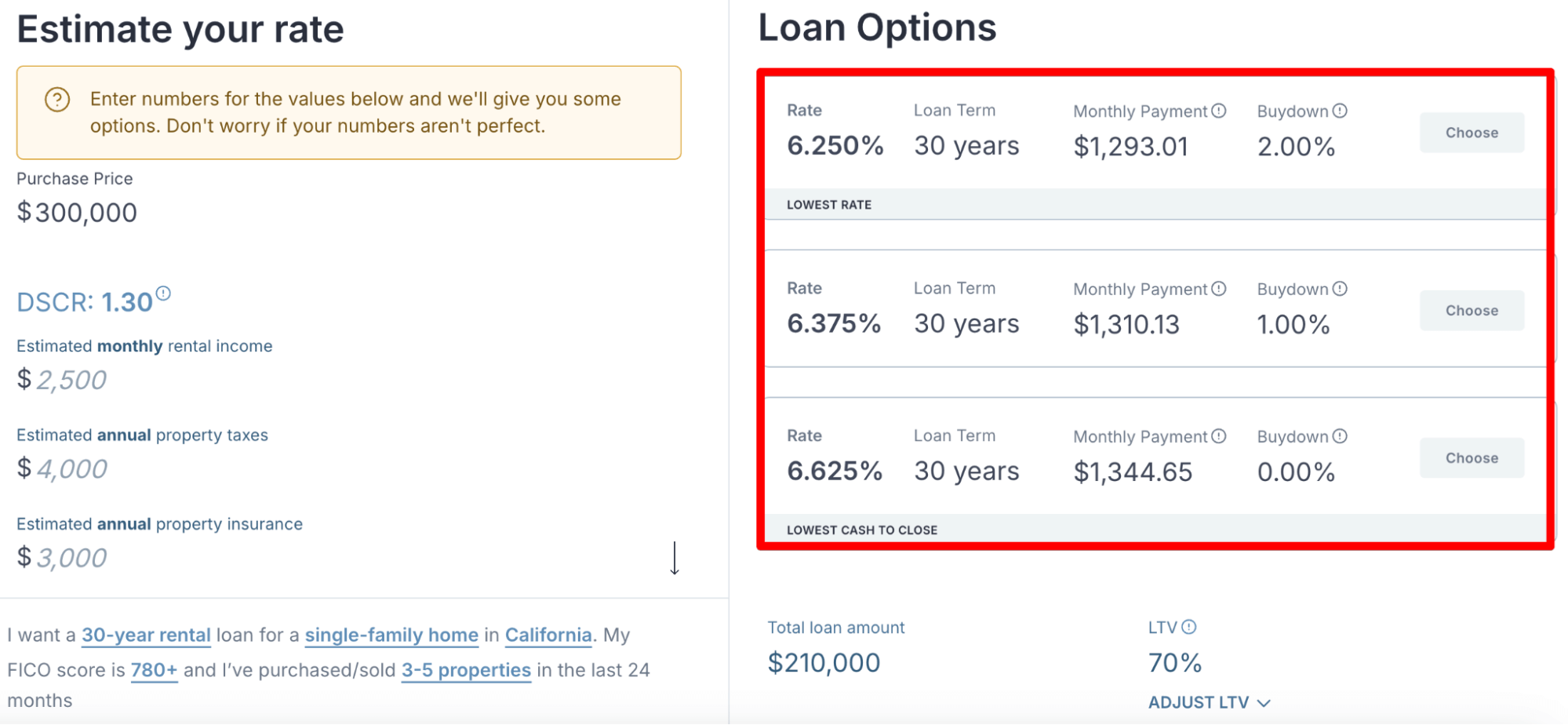

Simply answer eight questions in our automated pricer and you’ll receive three quotes showing your interest rate (fixed-rate or adjustable rate), monthly payment, and buydown options.

We encourage you to plot out different scenarios using various loan amounts, rental income figures, closing costs, and expense assumptions, to get an idea of how each affects your quotes.

Once you’ve decided on a quote, click on it, enter your full name and email address, and you’ll be able to download a term sheet and pre-approval letter.

From there, we’ll email you a link to our online documents portal, detailing the paperwork you need to submit, depending on the type of loan you’re applying for.

Once you’ve submitted everything, we’ll respond within an hour or two with approval and schedule closing in 7 to 14 days. We’ve even closed deals within four days!

Read more: 5 Best LLC Mortgage Lenders: Guide for Borrowers

We Are a Direct Lender, Not a Loan Broker

A common problem with many rental property lenders is that they’ll say you qualify when you first apply — only for complications to pop up right before closing.

That’s because many rental property “lenders” are actually brokers with no money to lend. They connect you to a real lender, collect a commission, and hope it works out. The trouble is, you’re not talking to the decision-maker:

- The broker may think you qualify based on your paperwork.

- But because they aren’t the decision-maker and often don’t know the lender’s exact criteria, they must send it to the lender for underwriting.

- Once the lender starts underwriting, they might find issues the broker overlooked.

- Those late discoveries can cause last-minute delays or even prevent the deal from closing.

At Constitution Lending, we're direct lenders and the sole decision-makers on your loan application, so we can guarantee closing immediately after reviewing your paperwork.

We don't have to file your loan application with another lender and wait for them to underwrite, eliminating the chance of last-minute drama.

We Offer Different Types of Rental Property Loan Products

We offer the following DSCR-based loan options:

- DSCR rental property loan: This is our flagship product that enables real estate investors to purchase or refinance rental properties at a low interest rate, using the property’s income to qualify.

- DSCR portfolio loan: Our portfolio loan can help real estate investors who have a portfolio of financed rental properties consolidate all their existing loans and mortgage payments at a lower interest rate. Since the mortgage loan is underwritten on the property’s financials and not yours, you don’t need pay stubs, W-2 forms, employment verification, and other information banks ask for.

- Cash out refinance or home equity line of credit (HELOC): If you have home equity, you can use it as a downpayment to purchase a rental property.

- Fix and flip: Our fix and flip loan helps investors purchase fixer-uppers, renovate them, and rent them out long-term. We can provide a short-term fix and flip loan and later convert it into a long-term DSCR loan, so you secure your short-term fix and flip loan and long-term mortgage loan in the same place.

Get Started

Use our automated rental property pricer to explore different loan scenarios and see what terms you qualify for.

2. U.S. Bank

U.S. Bank offers a variety of investment property loan products that real estate borrowers can use to purchase one to four-unit residential properties. They also allow homebuyers to use equity that they’ve built up in their primary residence as a down payment.

To qualify, U.S. Bank requires a strong credit score, a 20% down payment, and six to 12 months of cash reserves.

You can apply by completing the application form on their website, waiting for a call from a loan officer, explaining details about the deal, such as the property’s value and rental income, and the loan officer will get back to you with an approval.

That said, U.S. Bank is a traditional bank lender, so it’s unclear how quickly they can close compared to a private lender like Constitution Lending, which prioritizes speed. They don’t have automated tools such as a DSCR pricer and documents portal to speed up the application process.

3. Lima One Capital

Lima One Capital is a private hard money lender based in Greenville, South Carolina, offering a single-family rental loan product that allows investors to purchase non-owner-occupied properties. Lima One doesn’t ask for income verification documents, making it ideal for self-employed homeowners who don’t earn a W-2 income.

Lima One’s single-family rental home loan can be used to purchase one to nine-unit properties. Loan amounts range from $75K to $2.5MM, and real estate investors can secure an LTV of up to 80%. They also offer a portfolio loan that borrowers can use to consolidate multiple hard money loans into one payment at a lower interest rate.

For those looking to purchase a residential or commercial property and rent it on Airbnb, Lima One has a short-term rental loan that’s underwritten using STR data.

However, it’s worth noting that Lima One still relies on outdated processes; borrowers need to wait for a loan officer’s phone call, explain the deal over the phone, and then receive a quote and a term sheet. They don’t have an automated pricer for generating an instant quote.

4. Griffin Funding

Griffin Funding is a mortgage lender based in San Diego, California, that specializes in providing alternative financing solutions to real estate investors, self-employed borrowers, and individuals with non-traditional income sources.

They offer multiple loan types that can be used to purchase rental properties, including DSCR loans, bank statement loans, and asset-based loans. These loans enable investors to qualify based on the property's income-generating potential, rather than the borrower’s overall financial profile.

Their DSCR loans are especially popular among borrowers seeking to scale quickly, since the loans are primarily qualified based on the property's rental income rather than personal income.

Additionally, Griffin Funding is a direct lender, and many online reviews mention how they are reliable at closing, so you won’t have to stress about the 11th-hour rejections and complications.

However, we feel it’s essential to note that Griffin Funding doesn’t offer an automated pricing tool or document portal that can expedite the application process, so we aren’t sure how quickly they can close.

5. Visio Lending

Visio Lending is a real estate lender that offers investor-friendly DSCR loan products that help borrowers qualify based on a property’s income. Borrowers can secure long-term 30-year DSCR loans as well as short-term rental loans used to purchase Airbnb and Vrbo properties.

To qualify, borrowers must have a credit score of at least 620. However, scores of 700 or above are typically required to secure the most favorable mortgage rates. In addition, the property must meet a minimum DSCR threshold of 0.75, and the borrower must provide a down payment of at least 20%.

Borrowers can apply for Visio Lending’s DSCR loans by simply completing a short application on their website, filling out their loan file, and then submitting documents to their loan officer.

While Visio Lending claims to be able to close quickly, they don’t provide a clear timeline, making it difficult to determine if they are a practical option for borrowers who need funds urgently.

6. Stratton Equities

Stratton Equities is a private mortgage lender specializing in real estate investment loans. They have a wide range of flexible financing options tailored to professional real estate investors, including DSCR loans, fix-and-flip loans, blanket loans, FHA loans, and portfolio loans.

Unlike conventional mortgages that often have rigid underwriting guidelines, Stratton Equities focuses on common-sense underwriting.

Stratton Equities doesn’t require perfect credit or W-2 income to qualify. Instead, the borrower’s eligibility is determined by the cash flow generated by the property. This makes it easier for self-employed borrowers, full-time investors, and landlords to secure property financing.

Their DSCR loan programs typically require a minimum credit score of 620 and a down payment of 20% to 25%, depending on the property and loan structure. The qualifying DSCR ratio usually needs to be at least 1.0, but more favorable terms are available for properties with stronger cash flow.

However, just like the options mentioned above, Stratton Equities doesn’t offer automated tools to speed up the application process, so it’s not clear how quickly you’ll receive a quote and term sheet.

Secure Fast Low Interest DSCR Loans with Constitution Lending

Generate an instant quote using our automated DSCR pricer and we’ll close within 7 to 14 days.