Earn 10%-14% Interest Investing in Short-Term, Real Estate-Backed Loans

What Sets Constitution Lending Apart from Other Investment Platforms

What Investors Say About Our Loan Investment Options

How to Invest in Our Real Estate-Backed Loans in 3 Steps

Constitution Lending vs other real-estate investment platforms

Frequently Asked Questions

What Types of Loans Does Constitution Lending Originate?

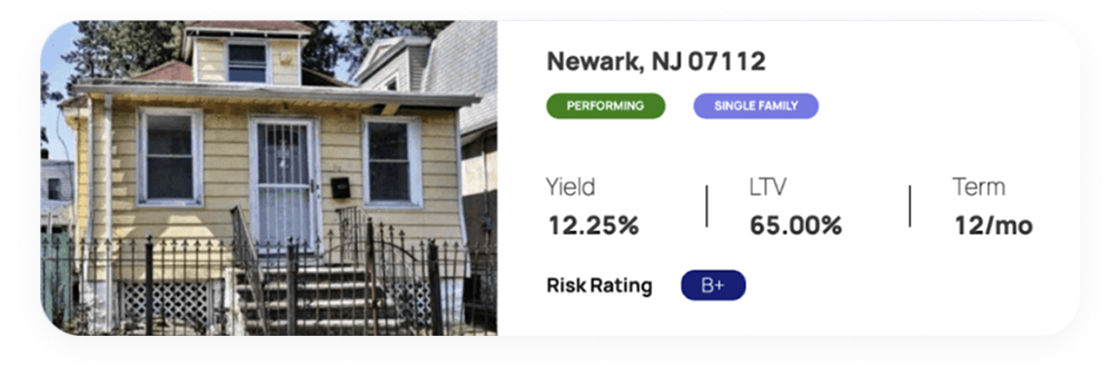

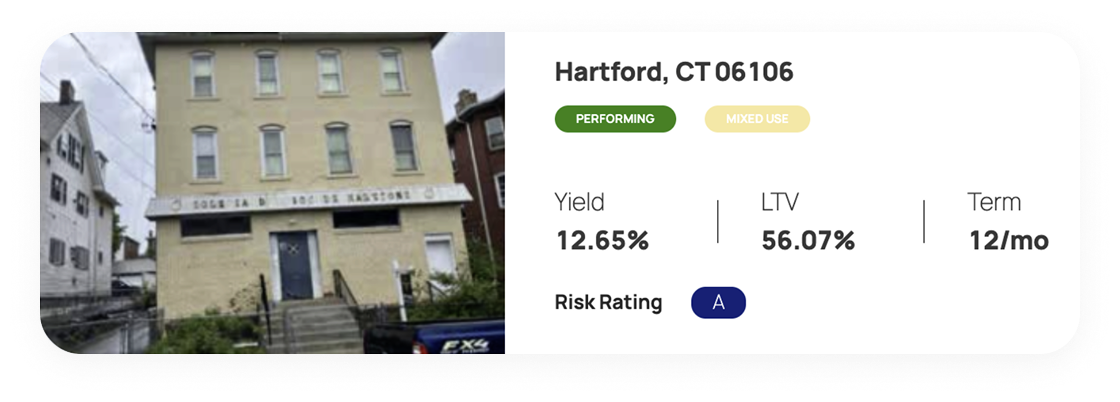

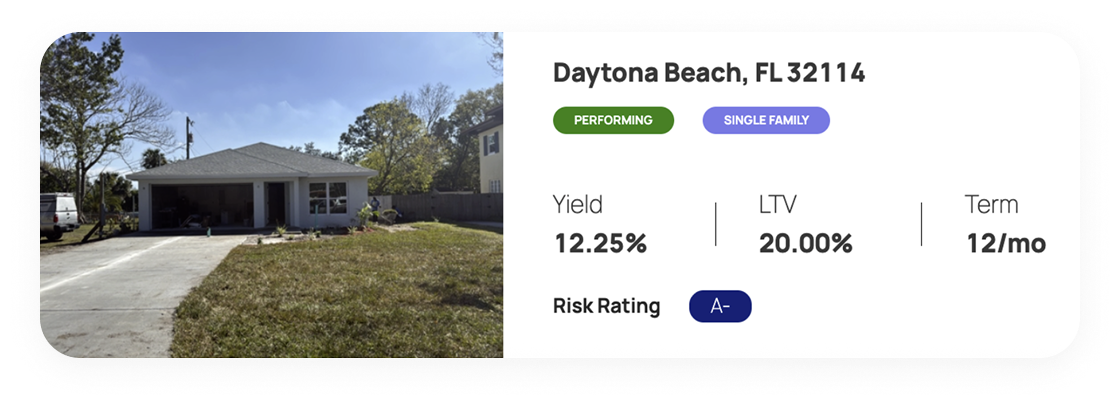

Constitution Lending primarily originates 6 to 18-month-long commercial loans used to rehab or construct investment properties. Due to the short-term nature of these loans, investors typically earn higher interest rates than they would with longer-term investments, ranging from 10% to 14% annually.

How Is My Investment Secured?

Our loans are secured by a first-lien position on the underlying real estate. This real estate is significantly more valuable than the owed balance, providing strong capital protection. Investors can recover their full principal by liquidating the property, even in worst-case scenarios, like the property losing value and the borrower defaulting.

Will I Lose Money if a Borrower Defaults?

Because we originate loans where the property is worth substantially more than the outstanding amount, it provides an equity cushion protecting you from default risk. It means the borrower can default, the property can lose value, and we can still liquidate it and recover the owed amount. Additionally, with our payment guarantee, we cover up to 6 months of interest payments in the meantime.

What Is the Typical Return on Investment?

Interest rates on our short-term commercial loans range from 10% to 14%, paid to investors on a monthly basis. When the property is flipped or constructed and sold at the end of the loan term, the borrower pays the outstanding balance, returning your principal investment.

What Is the Minimum Investment Amount?

Investors can start with as little as $1,000 — far less than the capital typically required to originate or buy loans outright.

How Quickly Do I Get My Money Back?

Our loans have terms ranging from 6 to 18 months. As a result, investors typically receive their full principal back much faster than with traditional fixed-income investments.

What Happens if a Borrower Defaults?

If a borrower defaults, we step in to cover your monthly interest payments for up to 6 months. During that time, we initiate foreclosure and sell the property — using the proceeds to return your principal. This is possible because we only fund loans backed by real estate worth significantly more than the loan amount, creating a strong equity cushion that protects your investment.

How Are Deals Selected and Underwritten?

Our primary consideration when underwriting loans is the loan-to-value ratio (LTV). LTV compares the loan amount to the property’s value (e.g., a $750K loan secured by a $1MM property = 75% LTV). We originate loans with a LTV ratio under 75%, providing investors with significant protection against market volatility and borrower defaults.