Dear Partners,

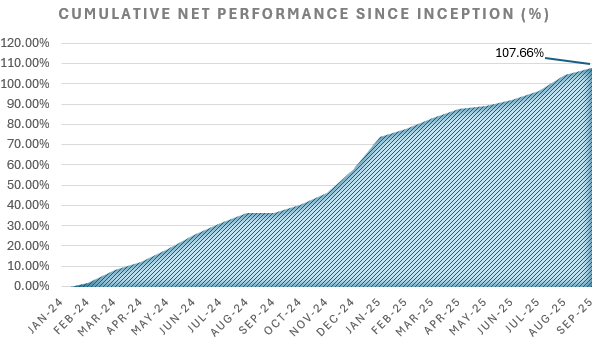

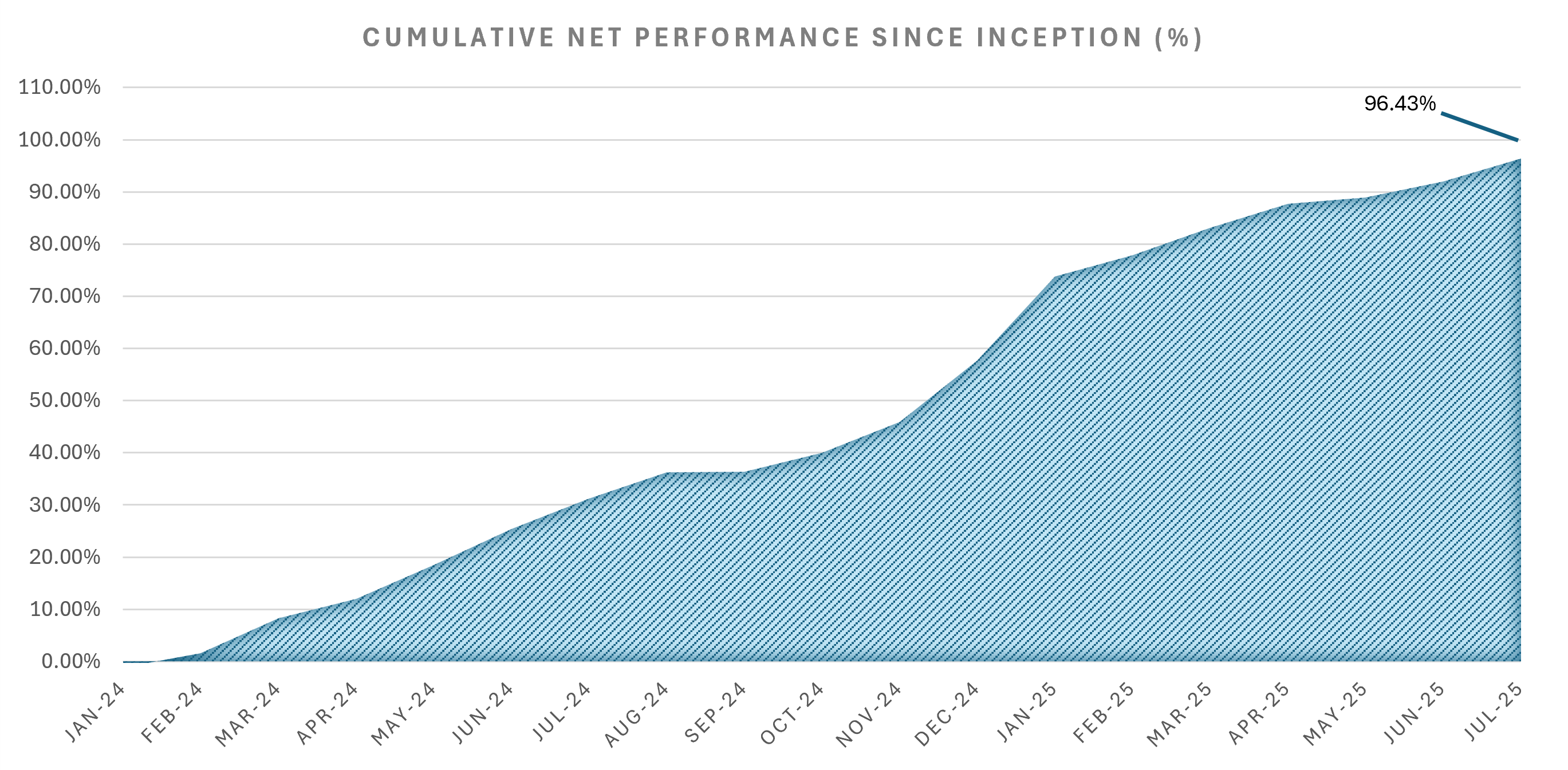

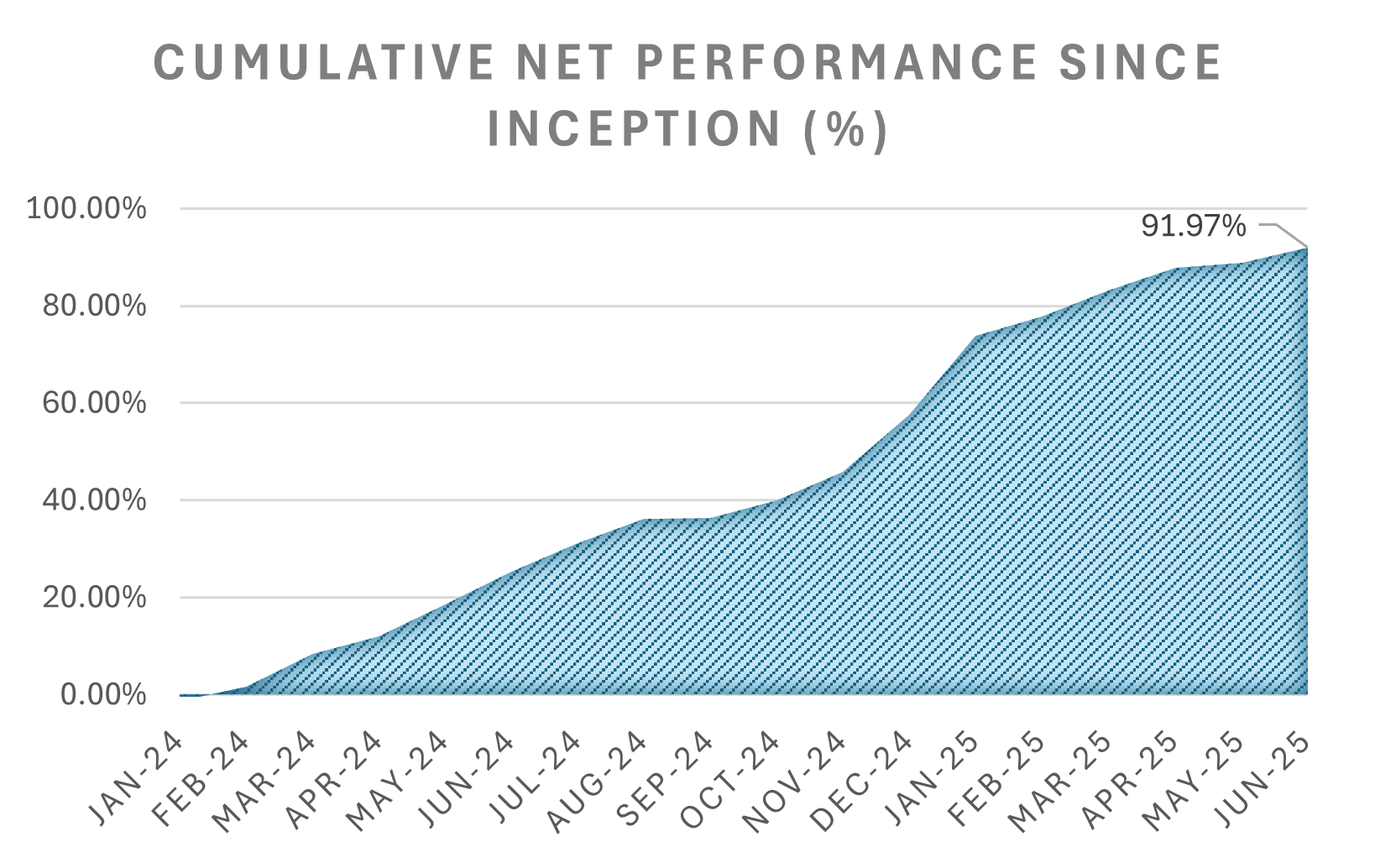

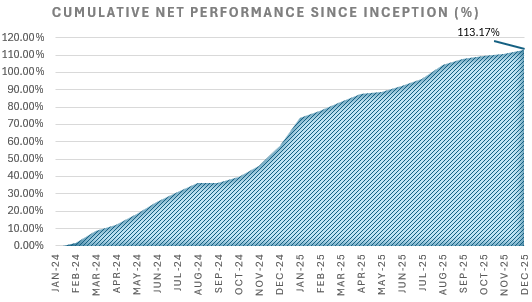

The Constitution Real Estate Credit Fund closed Q4 2025 with 0.92% in October, 0.11% in November, and 3.05% in December, bringing full year net performance to 37.67%.

Please find below our reflections on 2025 and thoughts on the year ahead.

Performance

- Net Return FY 2025: 37.67%

- Net Return FY 2024: 57.60%

- NAV as of December 31, 2025: $18,081,984

Net P/L Performance by Month Breakdown

Jan 2024

-1.21%

Feb 2024

2.85%

Mar 2024

6.59%

Apr 2024

3.38%

May 2024

5.84%

Jun 2024

5.78%

Jul 2024

4.68%

Aug 2024

3.83%

Sep 2024

0.06%

Oct 2024

2.69%

Nov 2024

4.11%

Dec 2024

8.02%

YTD 2024

57.60%

Jan 2025

10.27%

Feb 2025

2.18%

Mar 2025

2.25%

Apr 2025

2.52%

May 2025

0.61%

Jun 2025

1.63%

Jul 2025

2.32%

Aug 2025

3.92%

Sep 2025

1.70%

Oct 2025

0.92%

Nov 2025

0.11%

Dec 2025

3.05%

Portfolio Insights and Highlight

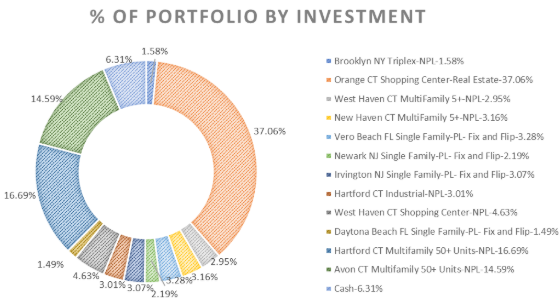

- As of December 31, the Fund holds 16 active investments. The portfolio is now the most diversified it has ever been, while our sourcing pipeline continues to expand as our ability to acquire and manage larger transactions at scale increases.

- During Q4, we added 6 new investments: 3 in October, 1 in November, and 2 in December. The Avonwood position was fully resolved at the end of October and earned the fund a great return. This one exceeded our resolution timeline by a lot.

- The Fund reached $18 million in NAV, and across the broader Constitution platform, we now manage over $105 million in capital, inclusive of the Fund, actively managed individual notes, prefunding structures, and joint ventures.

- The Fund now counts over 100 limited partners, with more than 400 accredited investors having participated across the platform.

-

Asset Updates

- 44 Avonwood Road, Avon CT | 188 Unit Multifamily NPL:

Constitution acquired a non-performing senior loan secured by a 188-unit multifamily property in Avon, Connecticut following an extended period of payment default driven by prolonged operational underperformance and sponsor inattention. - While the loan was acquired at par, the investment thesis was anchored in strong collateral fundamentals, stabilized cash flow, and multiple expedient resolution paths supported by real-world operating data.

- Read Case Study on this trade

- Resolution Path:

Following the acquisition, Constitution promptly commenced a foreclosure proceeding when the borrower subsequently filed for bankruptcy, which initiated a contentious process involving a variety of complex litigious matters. Through a disciplined and legal strategy, the process was complete in 10 months and culminated in a court-effectuated sale. The fund earned an unlevered 25.2% IRR on this NPL. - Sheldrake NY | Mobile Home Park:

The Fund acquired its first NPL secured by a mobile home park, sourced directly through one of our limited partners, who received a finder’s fee for originating the opportunity. - The loan has a principal balance of approximately $550,000, with estimated payoff due to accrued default interest and fees exceeding $1.0 million. We estimate the underlying collateral value at $2.0+ million, providing substantial downside protection and multiple resolution options.

- Orange NJ | 50+ Unit Multi Family NPL:

The largest investment made in Q4 2025 was the Fund’s acquisition of a 50+ unit multifamily non-performing loan in New Jersey. As the asset remains in active foreclosure, we cannot disclose the property address or other identifying details at this time. - This investment follows the same strategy as our prior multifamily NPL acquisitions. The borrower is no longer in a position to complete the project and is seeking to avoid a prolonged and costly legal process.

- Our objective is to obtain title as efficiently as possible, complete the remaining ~10% of construction using our in-house construction team, and then stabilize operations and lease-up through our in-house property management platform.

- We will continue to provide updates as the foreclosure progresses and the business plan advances.

Looking Ahead

- Many of the market dynamics that supported our growth and strong results in 25 remain intact

- Debt funds have less room to maneuver with rates still high

- Sponsors have limited recap options with static in-place NOI and low to mid-single debt yields

- Office and retail leasing are picking up

- Multifamily rents across our core markets are up 4% or more YoY

- We have nearly $300mm of NPL pipeline

- Among the upcoming opportunities are infrastructure bonds and SASBs; both new instruments for us

- We are actively sourcing more NPL opportunities; if you see something say something!

- We are always in the market for institutional capital to collaborate on deals; reach out if you’re interested.

- We are actively looking to better understand public debt capital markets for CRE; if you (or a friend) touch securitized products there’s a beer with your name on it!

- If you’d like to discuss the Fund or upcoming opportunities, schedule a call with us

- We are working on improving the speed of our reporting in 2026 so that statements are provided within 30 days of the end of the month

-

2025 Recap

The fund began its second year in a market much like the first. CRE values either static or declining, rates holding steady at higher levels across the curve, and looming maturities making equity sponsors sweat.

For the fund, 2025 was a year of firsts and highlights, below are some of our favorites:

- First NPL resolution exceeding $30mm

- First resolved land NPL

- First office loan origination

- First loan with a contract rate higher than the LTV

- Resolved a mid-stage construction NPL in ~60 days

- First mobile home park NPL

- First NPL over 70mm under contract (More details to come)

- First New Jersey NPL

The Fund achieved new high-water marks across capital deployed, assets resolved, dollar profits, and NAV growth.

Multiple deals that had been in the works for 12 to 36 months or more came to fruition; a testament to our persistence on sourcing (and the increasing inflexibility of lenders’ warehouse lines). Counterparties for 2025 were a broad cross section: seller financed notes, bank loans, bridge lenders, and CMBS trusts were among our sellers last year.

We are excited about a market that broadly looks very similar to the beginning of 2025, but with some better fundamentals in office and retail.

Thanks to the support of our limited partners; 2025 saw NAV grow more than 3x. We are grateful for your continued trust and support.

Learn more about investing in the Constitution Real Estate Credit Fund

All the best,

Ricardo, Kyle, and Joe

200 Pemberwick Road, Greenwich CT 06831

Invest@ConstLending.com

203-423-3534