Short-term notes are loans with a term of 12 months or less.

When you invest in short-term notes, you effectively act as the lender, providing capital in exchange for monthly interest payments and the return of principal at the end of the loan term.

Good-quality short-term notes can offer higher annualized returns than long-term investments — interest on short-term loans (such as fix-and-flip, bridge, and construction loans) is currently at 10% to 14%. They are also more liquid because you receive your principal in under 12 months.

While notes can be an effective short-term investment vehicle for generating higher returns with strong principal protection, investors often make critical mistakes that expose them to unnecessary risk.

To help investors make informed decisions and avoid common mistakes, we wrote this guide on seven key factors to consider when investing in short-term notes.

We also recognize that most individual investors lack the capital, expertise, or time to originate their own short-term loans. Therefore, we discuss how Constitution Lending enables investors to purchase fractional shares in loans we’ve already originated, starting with just $1,000.

Who are we? Constitution Lending is a private money lender who has originated more than $200MM in short-term loans. Investors can purchase fractions of these loans through our investment platform. Due to the quality of our loans, our investors have never incurred a principal loss. Sign up for an investor’s account to learn more about our loan options.

Is the Note Secured by a Stable Asset Worth More Than the Loan Amount?

The most crucial factor to consider when determining the quality of a note is whether it's secured by a stable asset that increases in value over time, such as real estate. This stable collateral protects investors in worst-case scenarios. If borrowers default, investors have the legal right to seize and liquidate the collateral to recover the outstanding balance.

Investors should also consider the loan amount (i.e., the face value) compared to the value of the collateral and only invest in notes where the collateral is worth significantly more than the loan amount. This ratio is known as a loan-to-value ratio or LTV; for example, a $750K loan secured by a $1MM asset has an LTV of 75%.

Lower LTV ratios offer investors an added layer of capital protection as they create a cushion against market fluctuations or borrower default.

In the example above, even if real estate values decline by 25% — an unlikely scenario given the stable nature of real estate and the short duration of these notes — the collateral could still be liquidated for $750K, allowing investors to recover their full principal.

We originate loans with an LTV below 75%, providing our investors with a substantial borrower equity cushion to protect their capital.

What’s the Interest Rate on the Loan?

Another factor to evaluate is the interest rate and fees the borrower is paying, as well as the loan time frame, and repayment schedule, as these determine your returns.

Most of the short-term loans that we originate have interest rates between 10% to 14%. Borrowers pay this higher interest rate because of our closing speed and reliability. We close loans within 7 to 14 days, whereas borrowers who approach banks for financing typically wait 40 days or more.

However, interest rates on short-term notes vary significantly depending on the type of instrument. For example, short-term Treasury bills are considered the safest form of debt, backed by the full faith of the U.S. government. As a result, yields are currently low, ranging from 4.5% to 5.0%.

In contrast, unsecured promissory notes generally offer higher yields — ranging from 8% to 15% — to compensate for the increased risk. But these instruments carry no collateral, meaning investors are fully exposed to borrower default.

What’s the Borrower’s Credit Score?

Investors should consider the borrower’s credit score because it’s the most reliable indicator of their willingness to repay loans.

As a general rule, we recommend investing in real estate notes where the borrower has a credit rating of at least 660. Naturally, the higher the score, the stronger the borrower’s credit profile — and the lower the default risk.

It’s also a good idea to assess the borrower’s level of experience in real estate investing. Borrowers mainly use secured short-term notes to rehab properties, so a strong track record of successful fix-and-flip projects demonstrates the borrower’s ability to execute rehabs effectively, which reduces execution risk and the likelihood of default.

At Constitution Lending, we only lend to borrowers with a credit score of 660 or higher. Plus, our network of borrowers have extensive real estate experience.

Is the Note First or Second-Lien?

Investors should consider their position in the capital stack, that is, the order in which they’re repaid after the borrower sells the property.

In most capital stacks, once the property is sold, the proceeds are first allocated to first-lien note holders, then to mezzanine or preferred equity investors, and finally to common equity holders, i.e., borrowers.

We recommend investing in first-lien, short-term notes, as these are the safest — you get repayment priority over investors in other loans. You recoup your full investment before any other parties receive distributions.

As the issuer, Constitution Lending exclusively originates first-lien commercial loans, ensuring that our investors are paid first.

Factors to Consider When Investing Through a Lender

As we alluded to earlier, most individual investors lack the capital, time, and expertise necessary to underwrite, originate, and service short-term loans.

So, it’s common for investors to partner with an established lender and purchase fractions of the loans that they originate. This method requires less capital, and investors don’t need to learn the intricacies of loan underwriting and origination or handle any of the manual work themselves.

Here are additional factors to consider to ensure you’re partnering with a high-quality lender originating safe loans.

Does the Lender Invest Alongside You?

Check whether the lender is invested in the same promissory notes as you, as this indicates that their financial interests align with yours by promoting only high-quality investment options.

In our experience, many of the “lenders” in the market are note brokers who promote loans without having any personal investment in them. They earn fees for connecting buyers and sellers, which means they’re incentivized to push any loan, even those of low quality.

With Constitution Lending, we’ve originated all debt securities on our investment platform using our capital and hold more than 50% of each loan on our balance sheet. This assures investors that our financial goals align with theirs.

Does the Lender Have Payment Protections in Place in Case Borrowers Don’t Pay?

One of the main concerns people have when investing in short-term debt for the first time is what happens if the borrower doesn’t pay.

With most lenders, investors would have to wait for the lender to conduct the foreclosure process and liquidate the property before they receive their principal and interest.

We advise investors to consider whether lenders offer payment guarantees in the event that borrowers fail to make payments, as this ensures they receive stable cash flow for the entire loan term.

Constitution Lending is the only lender (that we are aware of) that offers payment guarantees. We will pay you up to 6 months of interest payments in the event borrowers default.

What’s the Lender’s Borrower Default Rate?

While it’s nice to have the insurance of a payment guarantee, it’s better to just invest in mortgage notes with high-quality borrowers who don’t miss payments in the first place. As a result, we advise asking a lender for their borrower default rate before investing in their loans.

The borrower default rate is the percentage of borrowers who stop making payments. For instance, if four borrowers out of 100 stop paying, the borrower default rate would be 4%. This metric is an excellent gauge of a lender’s loan quality.

The nationwide default rate on loans is 4% — At Constitution Lending, we have a borrower default rate of less than 2%.

How Individual Investors Can Access High-Quality Short-Term Notes

As previously discussed, fractional investment through a lender like Constitution Lending remains the most accessible path for individual investors to invest in high-quality commercial paper because:

- You only need $1,000: When originating short-term loans, investors typically require at least a couple hundred thousand dollars, given the prices of properties in the U.S. Fractionally investing through a lender provides an opportunity to invest in high-yield short-term debt for as little as $1,000.

- You don’t need to do all the manual work: To originate short-term loans, investors would need to negotiate with borrowers, conduct thorough due diligence, navigate state laws, and manage ongoing servicing and compliance. Most investors don’t have the time and expertise for this. However, when investing fractionally, you let us handle all the manual work, and you receive monthly interest payments.

- You’re better diversified: A consequence of the high costs of originating loans is the lack of diversification. Because it’s so expensive, most investors can’t diversify across multiple locations, borrower profiles, property types, and so on. With fractional investing, it’s much easier to diversify your portfolio because you can start with such a small amount.

What Sets Constitution Lending Apart From Other Lenders

- Low LTV loans: Constitution Lending originates short-term notes with LTVs below 75%, providing investors with substantial capital protection. A 25% borrower equity cushion protects against market and default risk.

- We invest alongside you: Because we use our capital to originate loans and hold them on our balance sheet, our financial interests are fully aligned with yours. We only present investment opportunities we believe in.

- We have low borrower default rates: Due to the quality of borrowers we lend to, our default rates are just 2%, some of the lowest in the U.S. For context, the average borrower default rate in the U.S. is 4%, and many private lenders have higher default rates.

- We offer payment guarantees: We are the only lender that provides a 6-month payment guarantee to mortgage note investors in the event of default.

- Our borrowers have years of experience and high credit scores: Due to the quality of borrowers in our network, investors have peace of mind knowing that borrowers possess the operational expertise to execute their fix-and-flip plans effectively.

- Our background lies in purchasing and resolving non-performing loans: We started our careers buying and recovering non-performing debt. To date, we’ve resolved more than $50MM of non-performing debt. As a result, we’ve developed deep expertise in foreclosure and asset liquidation.

How to Invest with Constitution Lending in Under 5 Minutes

- Create an account on the Constitution Lending platform.

- Connect a bank account or IRA and browse available investment opportunities.

- Select a loan that you’d like to invest in and enter an investment amount.

- Complete the investment process through our secure portal.

- Receive monthly payments directly to your Constitution Lending wallet.

- Collect your full principal at the maturity date.

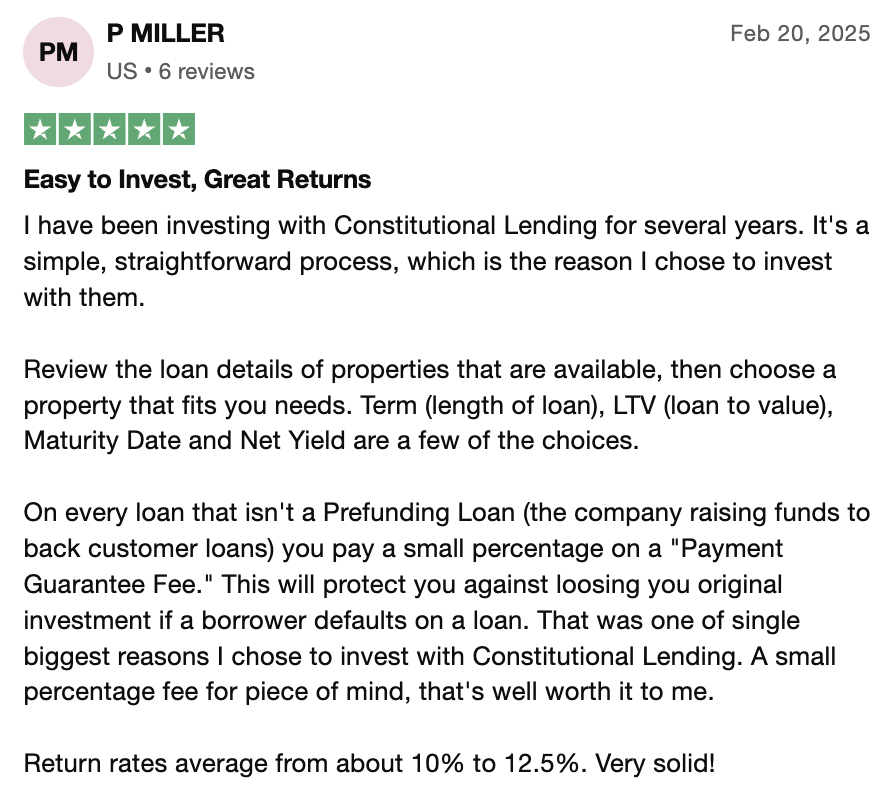

What Clients Say About Our Loan Options

Lend Money Directly to Borrowers

- Pros: Highest potential returns, complete control over underwriting and terms.

- Cons: Requires significant capital (typically $200K+), extensive expertise in real estate and lending, time-intensive for sourcing and servicing, high concentration risk.

Purchase Promissory Notes from a Marketplace or Broker

- Pros: Access to a variety of commercial paper, less capital required than direct lending.

- Cons: Brokerages aren't invested alongside you, quality control varies widely, no payment guarantees if borrowers default.

Purchase Treasury Bills and Other FDIC-Insured Fixed-Income Assets

- Pros: Extremely safe, backed by the U.S. government.

- Cons: Low yields (currently 4.5–5%) and no collateral backing.

Purchase CDs (Certificates of Deposit)

- Pros: FDIC-insured (in the U.S.) up to $250,000 per depositor, per bank, so your principal is safe.

- Cons: Your money is locked in until maturity, higher interest rate risk.

Grow Your Investment Portfolio with Constitution Lending

Sign up to our investment platform, browse available opportunities, and start investing with as little as $1,000.