Investors typically seek out Yieldstreet alternatives for three reasons:

- Higher returns: Yieldstreet’s primary real estate fund yields 6.6% annually, which is low given the risks involved with their construction and fix-and-flip investments. Safer investments such as REITs and broad-market index funds generate annualized returns of 10%.

- Better liquidity: Yieldstreet has holding periods of multiple years, and early withdrawals are penalized. In addition, Yieldstreet only allows withdrawals during “periodic liquidation events,” and even then, you cannot withdraw your full principal at once.

- More safety: The Yieldstreet Alternative Income Fund invests in real estate equity, not the debt secured by the property. This is riskier because equity investors are only paid after all debt holders are paid in full. This risk became clear in May 2025, when Yieldstreet informed investors that a Nashville real estate project was a total loss. A CNBC investigation found that out of 30 deals, four resulted in total losses and 23 were placed on an internal watchlist.

So, when choosing a Yieldstreet alternative, consider the three factors mentioned above. A high-quality real estate investment platform should (1) offer higher returns than the stock market and REITs, (2) provide strong liquidity, and (3) reduce risk by investing in real estate debt and not real estate itself.

In this article, we cover how Constitution Lending meets those three criteria. We discuss how retail investors can earn 10% to 14% annually, receive their entire principal investment in just 6 to 12 months, and protect against market and execution risk.

Towards the end, we cover additional Yieldstreet alternatives that invest in art investing, startups, private equity, cryptocurrency, and pre-IPOs, among other private market investments.

Sign up for a free investment account to learn more about our real estate debt investment options and investment strategies.

1. Constitution Lending

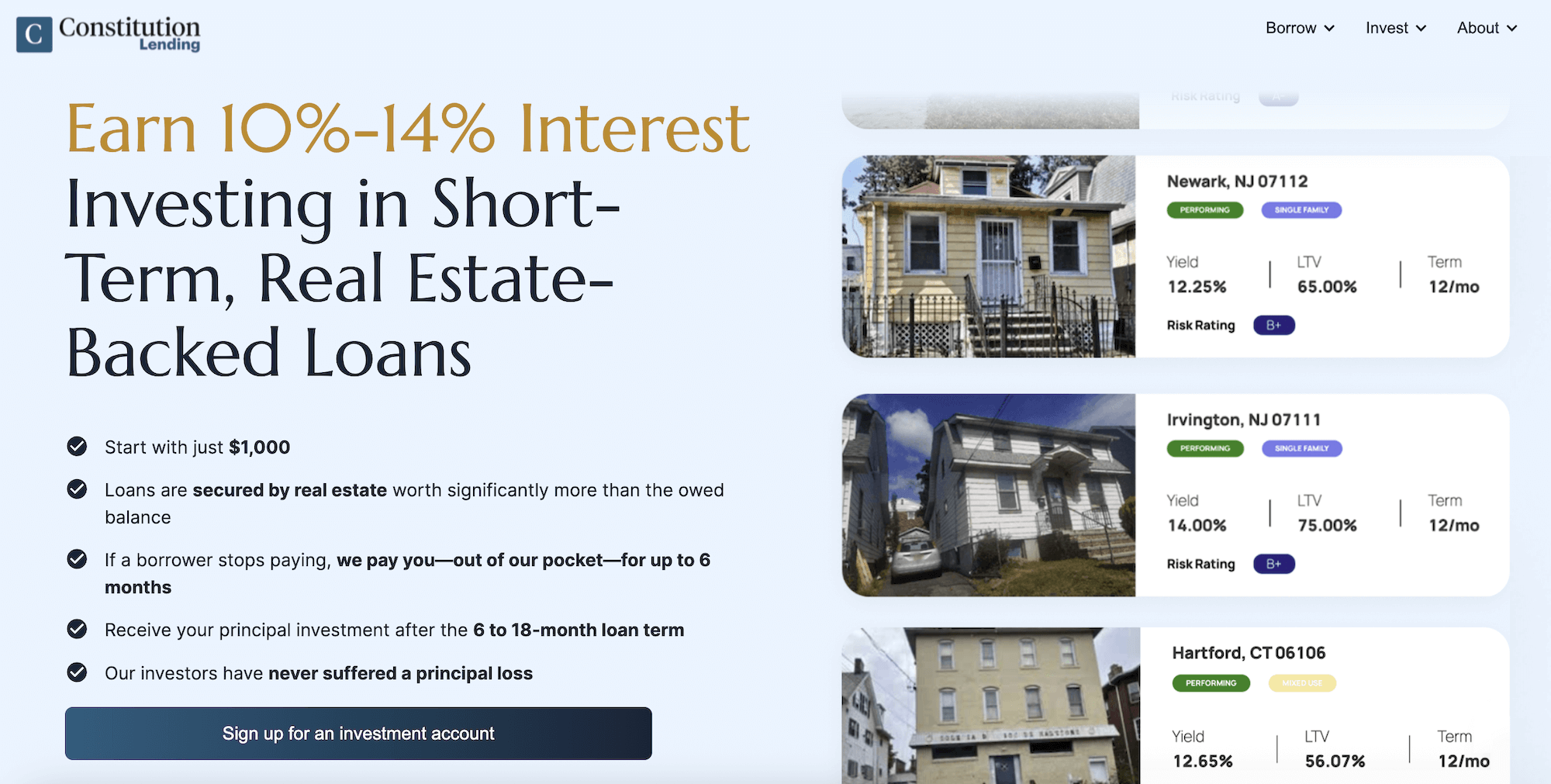

Earn 10% to 14% Annualized Returns Investing in Real Estate Debt

Constitution Lending is a direct lender for real estate investors looking to fix-and-flip and construct residential properties, and who need funds fast.

Retail investors can purchase shares in our loans with as little as $1,000 and earn 10% to 14% interest from borrowers.

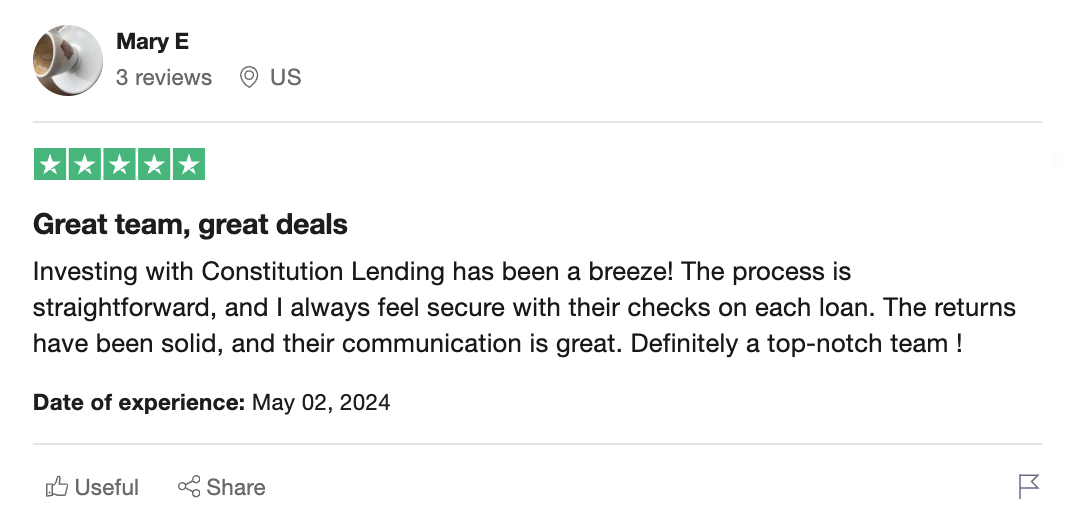

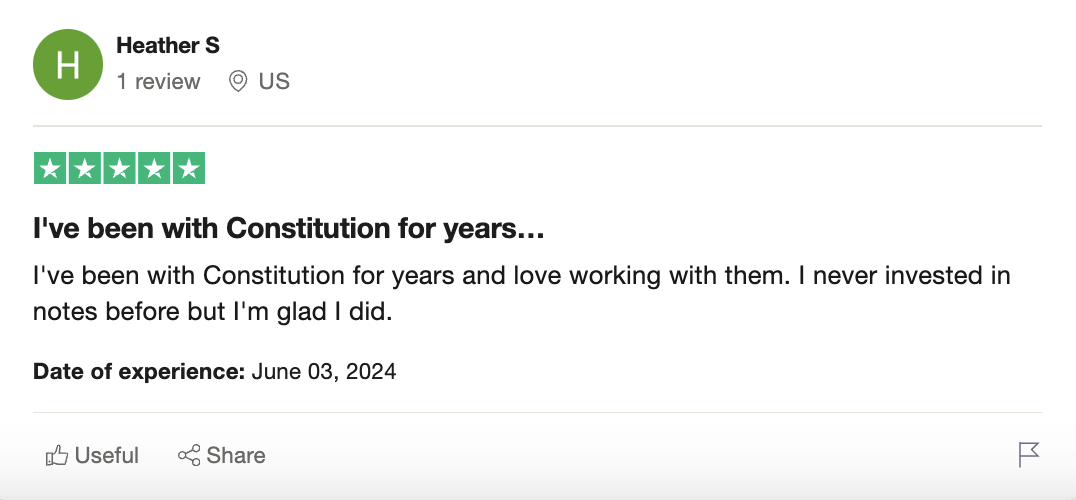

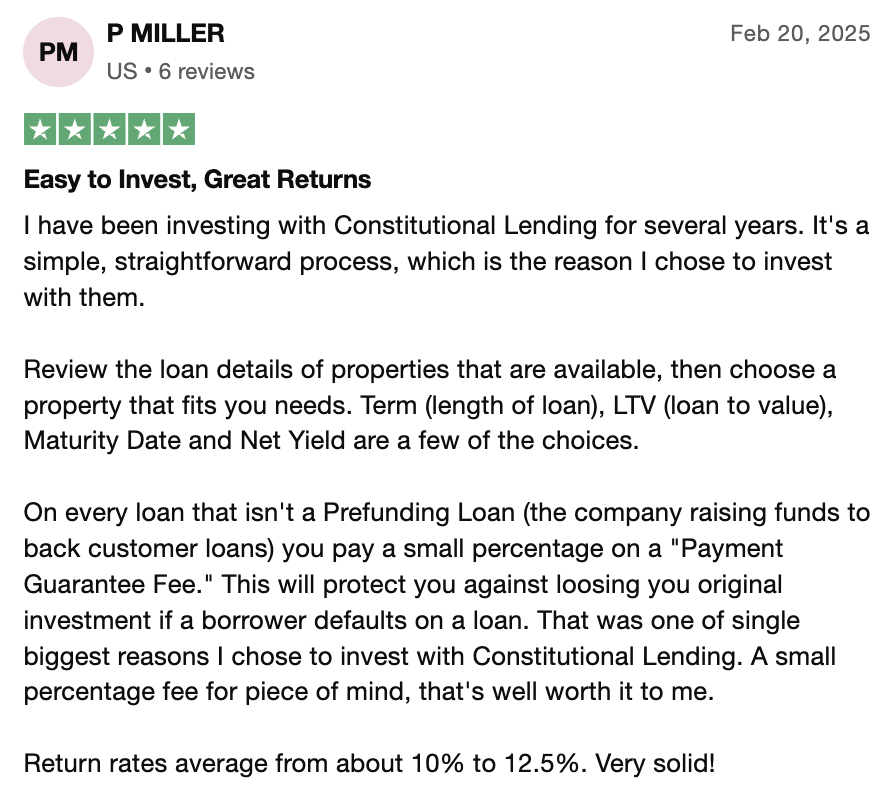

Here’s what investors say about our commercial real estate loans:

Below, we discuss how Constitution Lending solves the three issues with Yieldstreet mentioned above.

Factor #1: 10% to 14% Annualized Returns

Interest rates on our short-term notes (fix-and-flip and construction loans) range from 10% to 14%.

As an investor in our loans, you receive borrower interest payments every month until the end of the term. This allows you to earn significantly higher annualized returns than Yieldstreet and most investment platforms.

In addition, all our loans include a payment guarantee that pays you up to 6 months of interest if the borrower defaults. During this time, we can either renegotiate loan terms and have the borrower resume payments, or we can liquidate the underlying property and use the proceeds to recover the principal investment and interest.

However, as we discuss below, this payment guarantee is rarely needed given the quality of our borrowers.

Factor #2: 6 to 12-Month Investment Horizon

Our fix-and-flip and construction loans have terms of 6 to 12 months. At this point, the borrower sells the investment property and uses the sale proceeds to repay the full loan balance.

You receive your entire principal investment after 6 to 12 months. You can choose to reinvest in more short-term notes, diversify into other investments, or withdraw for personal reasons. You aren’t locked in for years.

Yieldstreet and other commercial real estate investment platforms are illiquid because you typically can’t sell allocations before maturity, which is sometimes 5 to 7 years. Even after the holding period ends, many platforms limit how much of your principal you can withdraw at a time.

Factor #3: Strong Principal Protection

With Yieldstreet, you’re investing directly in a piece of real estate, rather than the loan used to acquire it.

This is riskier because commercial real estate investors only get paid from sale proceeds after all debtors are paid in full. This means you’re the first one to lose money if property values decline.

For example, say you invest in a property on Yieldstreet worth $10 million. Out of the $10 million, $3 million is funds collected from investors and $7 million is debt. If property prices fall and the real estate can only sell for $7 million, you’ll lose your entire principal. The $7 million in sale proceeds are used to pay debtors.

However, when you invest in real estate debt, you’re protected by the borrower's equity, which absorbs losses in the property’s value. Staying with the above example, it means that the property can lose $3 million in value and you can still recover your entire principal; the real estate investor takes the hit. They must lose their entire equity investment before your principal investment is affected.

At Constitution Lending, we lend up to 75% of a property’s purchase price, giving our investors a healthy 25% borrower equity cushion to protect against potential losses in the property value.

Read more: Investing in Performing Notes: What They Are, Benefits & How to Start

Additional Benefits of Investing in Constitution Lending Real Estate Debt

Payment Guarantee Feature

As we alluded to earlier, all our loan options come with payment guarantees that automatically kick in if a borrower misses a payment. We pay you interest payments for up to six months, giving us enough time to get the borrower to pay again or foreclose on the property and use the sale proceeds to recover the principal and owed interest.

Low Borrower Default Rate

Our payment guarantee is rarely needed because the percentage of borrowers who default on our loans is very low. Out of every 100 loans we originate, fewer than 2 borrowers default, giving us a default rate of under 2%. For context, the nationwide default rate on real estate loans is around 4%.

This low default rate is because of the quality of borrowers we lend to. Over the past decade, we’ve built and financed a network of experienced real estate flippers and construction companies across Connecticut and the surrounding region. We have strong relationships with these borrowers and full confidence in their expertise.

We Invest Alongside You

Yieldstreet typically doesn’t invest its own capital into the projects in its fund. Instead, it acts as an investment manager that pools investor capital and deploys it across real estate deals.

In other words, Yieldstreet doesn’t directly invest alongside you on a deal-by-deal basis, which can limit incentive alignment around downside risk and capital preservation.

Compare that to Constitution Lending, where we originate every loan with our own capital and maintain a 50%+ stake throughout the term. We only make money if you do, aligning our incentives with yours and giving you confidence in the quality of our debt investment opportunities.

How to Start Investing with Constitution Lending

- Create an investment account with Constitution Lending to get started.

- Once you’re logged in, you’ll land on your main dashboard. Here, you can do your due diligence by reviewing the loans we’ve originated. Each listing includes key metrics such as loan-to-value (LTV), purchase price, exit strategy, projected yield, loan term, and our internal risk rating.

- If you want deeper insight into a specific short-term note, simply click on it, and you can view a detailed breakdown that includes the remaining loan balance, current and post-renovation LTV, the borrower’s credit profile, and any management fees.

- To invest, link either a bank account or an individual retirement account (IRA) to your Constitution Lending wallet. After that, choose the “Fund This Loan” button in the bottom-right corner and enter your desired investment amount. Once you’ve made an investment, you’ll be taken to a dashboard where you can see the performance of your real estate debt investment portfolio.

- You receive passive income in the form of borrower interest payments on the first day of each month, and your full principal is returned when the loan reaches maturity.

Earn 10% to 14% Annualized Returns Investing in Constitution Lending Real Estate Notes

Create an investment account to learn more about our real estate debt investing options.

2. Fundrise

Fundrise is an alternative investment platform that enables you to invest in a mix of alternative asset classes, including real estate, fine art, venture capital, private credit, and others.

Its Flagside real estate fund offers an accessible entry point into real estate investing for retail investors who don’t want to buy and manage rentals directly. Many reviewers like Fundrise’s low minimum investment requirements on its REITs and eFunds.

For newer investors or those with limited capital, this accessibility is a major advantage, as you can participate in large-scale real estate projects with just a couple of thousand dollars — projects that would typically require millions.

Users also like how Fundrise’s reporting dashboards make it easy to track performance, monitor project updates, and see how their capital is allocated across different property types and regions. This level of visibility is uncommon in most traditional private real estate funds.

That said, investors should be aware that most Fundrise investments aren’t liquid. Holding periods, early redemption fees, and market-driven suspension of withdrawals can limit your flexibility.

Fundrise’s annualized returns are also quite low. Since inception, they have generated only a 4.5% annual return.

Finally, it’s worth noting that Fundrise doesn’t offer a payment guarantee feature, so investors are exposed if tenants stop paying.

Read more: 5 Best Fundrise Alternatives for Higher Yields and More Liquidity

3. Roofstock

Roofstock is a real estate investment platform for investors who want to own single-family rental homes without managing them directly. Its marketplace model allows you to review detailed financials, tenant information, inspection summaries, and neighborhood metrics of numerous rental properties across the U.S before making an offer.

Returns on Roofstock generally come from two places: ongoing rental income and long-term appreciation. Many of the properties listed are already leased, so investors receive immediate cash flow and reduce the uncertainty that typically comes with finding quality tenants.

Where the platform is less flexible is liquidity. Buying through Roofstock still means buying real estate, so exiting an investment isn’t as simple as selling stocks. If you decide to sell, you’ll need to go through a full listing and closing process, and the timeline depends on market conditions and buyer demand. Roofstock’s fractional product offers a lighter version of ownership, but it’s still not a liquid investment.

Another important consideration is that Roofstock doesn’t offer a payment guarantee, so it’s unclear what will happen if tenants don’t pay.

4. Fidelity

Fidelity is a financial services provider with over $15 trillion in assets under management and offers REITs, crypto, stocks, and ETFs, among other alternative asset classes.

What stands out is their low investment requirements. You can start investing in REITs with just $1 and slowly build up a diversified portfolio over time. You don’t need tens of thousands of dollars like with many online platforms.

In terms of returns, Fidelity doesn’t promise performance because it’s a brokerage, but it empowers you with the resources to pursue strong, long-term results. The investment lineup includes commission-free stocks and ETFs, actively managed mutual funds, high-yield money market options, and sophisticated research tools.

Fidelity’s in-house funds, particularly its low-fee index funds, are another highlight; they’ve become a go-to choice for investors looking for broad exposure at minimal cost.

Liquidity is one of Fidelity’s strengths. Unlike private real estate or alternative platforms, most assets held in a Fidelity account can be bought or sold instantly during market hours.

5. Arrived Homes

Arrived Homes is an online platform that provides non-accredited investors with access to single-family rentals and vacation properties without the responsibilities of direct ownership. Unlike many platforms, there aren’t any accreditation requirements.

Instead of buying an entire home, you purchase fractional shares in individual properties, allowing you to build a diversified real estate portfolio with far less capital, similar to a crowdfunding platform.

The return profile is straightforward. Accredited investors earn through rental income distributions and potential property appreciation over time. Because Arrived handles acquisitions, management, leasing, and maintenance, the income you receive is passive.

However, shares cannot be freely traded, and investments typically carry a multi-year holding period. While Arrived has been rolling out limited redemption programs, they are not guaranteed, and accredited investors should assume their capital will be tied up until the property is sold. This makes Arrived more comparable to a long-term real estate fund than a brokerage account.

FAQ

Which is better, Fundrise or Yieldstreet?

Yieldstreet’s real estate fund has slightly higher annualized returns than Fundrise. Their Flagship fund yields returns of around 6.6% while Fundrise only returns around 4.3%. Fortunately, with Constitution Lending, investors can earn 10% to 14% by investing in the short-term, hard money loans we originate. They can start with $1,000 and receive their entire principal after 6 to 12 months.

Has anyone lost money on Yieldstreet?

Yes. Some Yieldstreet offerings have resulted in significant investor losses, including deals where investors lost most or all of their principal.

For example, media investigations have reported that several real estate investments offered on the Yieldstreet platform entered distress or were written down, including a Nashville luxury apartment project disclosed in May 2025, where investors were informed their principal was lost.

CNBC has also noted that a meaningful portion of Yieldstreet’s historical offerings were placed on internal watchlists due to performance issues, with a small number resulting in total losses for investors.

What are the best alternative investments?

Real estate debt is one of the best alternative investments due to its principal protection. As an investor in real estate debt, you get paid first and in full before the borrower. This protects your principal investment from market volatility as the borrower’s equity cushions losses in the property’s value. Few alternative investments offer this level of capital protection.

What are some good alternatives to Yieldstreet for investing?

Constitution Lending is a good alternative to Yieldstreet because investors in our real estate loans earn between 10% and 14% interest returns. We also offer payment guarantees on all loans, which means that if the borrower defaults, we pay you out of our own pocket. With Yieldstreet, their annualized returns since inception are only 6.6% and they don’t offer payment guarantees.