Alternative investment platforms allow retail investors to access high-barrier asset classes with substantially less capital than if they invested directly. These asset classes include real estate, private credit, venture capital, and farmland, among others.

Investors often turn to alternative investment platforms to diversify away from stocks and bonds and earn higher returns.

But from what we see, most platforms actually generate lower returns than broad-market index funds, REITs, and other more traditional investments.

For example, Yieldstreet and Fundrise, two of the most popular alternative investment platforms, generate annualized returns of 6.6% and 4.3%, respectively. Compare this to the S&P 500 and REITs, which yield around 10% annually.

With this in mind, we recommend considering three factors when evaluating an alternative investment platform:

- What are their returns? A high-quality alternative investment platform should deliver annualized returns higher than those of traditional index funds and REITs to compensate for the additional risk.

- How liquid is your investment? We recommend choosing a platform that repays your principal investment and returns it soon after you invest. This gives you the flexibility to reinvest more often, rather than having your capital locked up for years.

- What principal protections do they have in place? Principal protections are features of certain investments that preserve your original principal if the asset loses value. So, consider how much value your investments must lose before your principal is affected.

In this article, we review seven alternative investment platforms in the context of the three factors mentioned above.

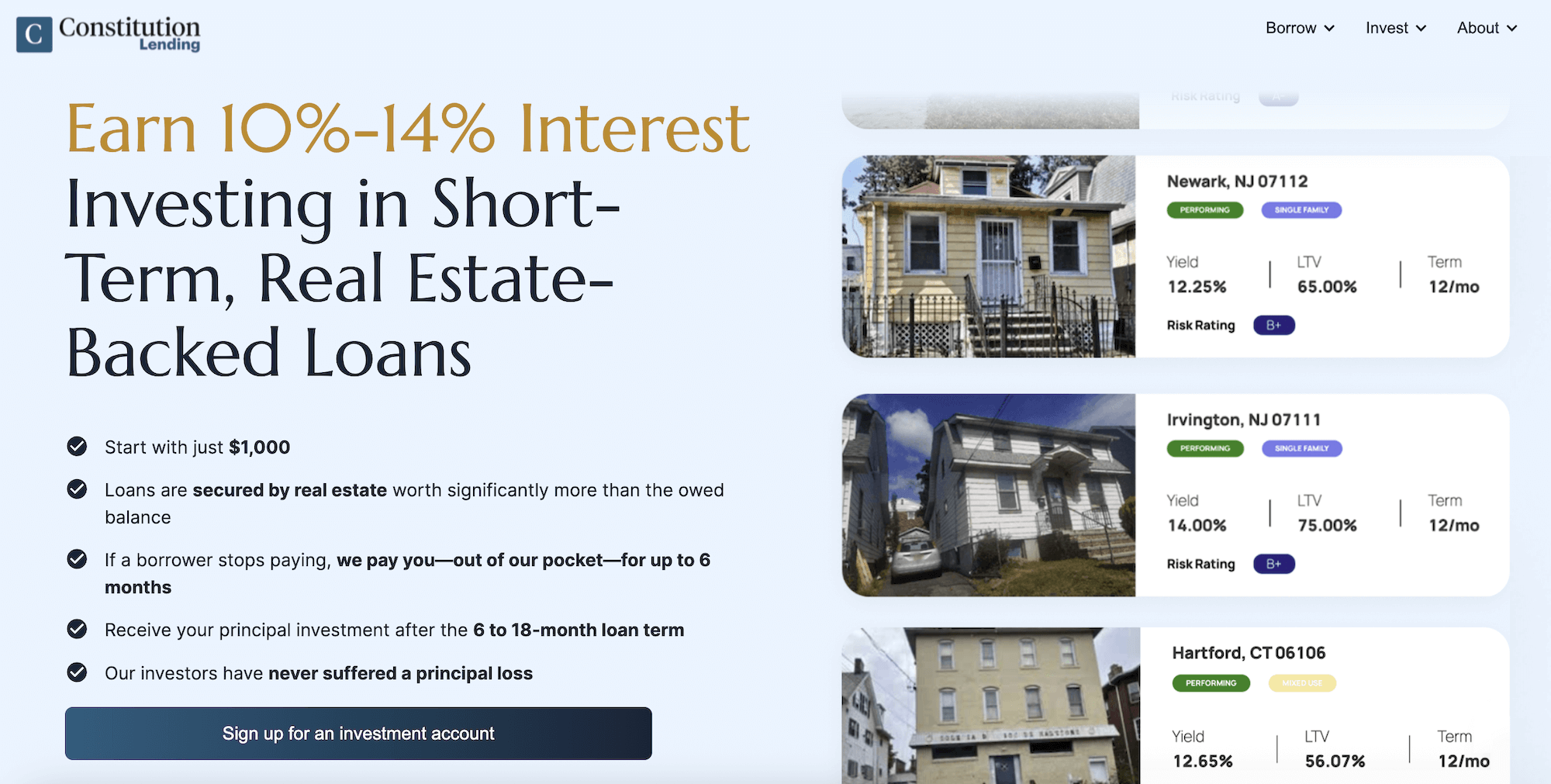

We’ll start with ourselves, Constitution Lending, discussing how investors can fractionally invest in real estate loans that we originate with just $1,000.

Toward the end, we cover platforms that specialize in venture capital, pre-IPO investments, commercial real estate projects, farmland, and other investment strategies, so you can compare your options with the three factors above in mind.

Open an investment account here to start investing in our real estate loans and earn 10% to 14% interest returns.

1. Constitution Lending: Invest in Short-Term Real Estate Loans Yielding 10% to 14% Annually

Constitution Lending is a private lender based in Connecticut that offers fix-and-flip and construction loans to flippers, construction companies, and other qualified real estate borrowers. Investors can purchase shares in these loans and earn returns through borrower interest payments.

Here’s a summary of how Constitution Lending addresses the three factors above:

- Borrowers pay 10% to 14% interest: This allows you to earn higher annualized returns than stocks, bonds, REITs, and other alternative investment platforms.

- Our loans are only 6 to 12 months long: At the end of the loan term, the borrower sells the flip-and-flip or new construction and uses the sale proceeds to pay off the loan balance. Your capital isn’t locked in for several years.

- Our loans have strong principal protection: You are protected by a first-lien claim on the underlying property, which is worth much more than the total owed amount. This protects your principal from market downturns. For example, if we lend $700,000 secured by a $1 million property, but it can now only be sold for $700,000 after a market crash, debt investors still receive their full principal while the borrower takes the loss.

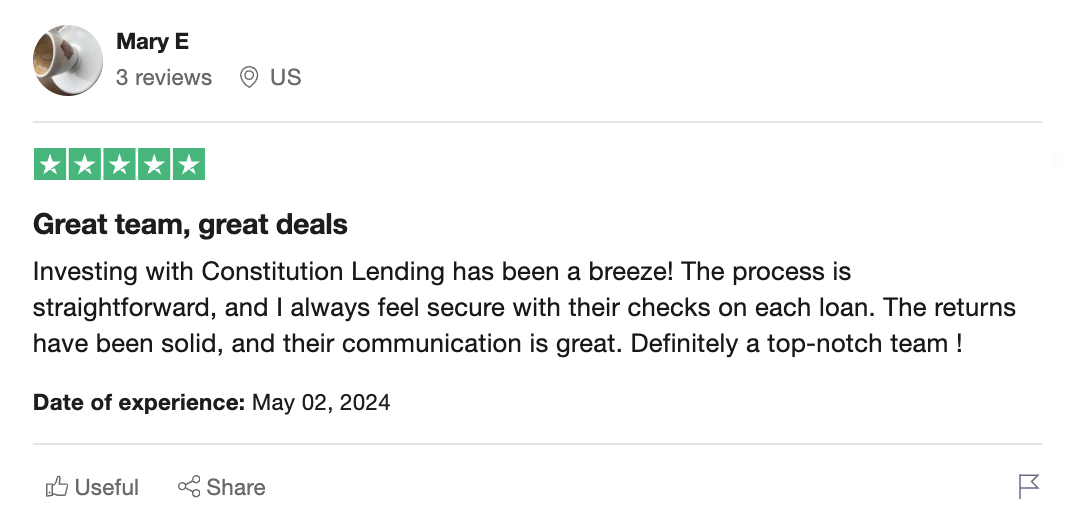

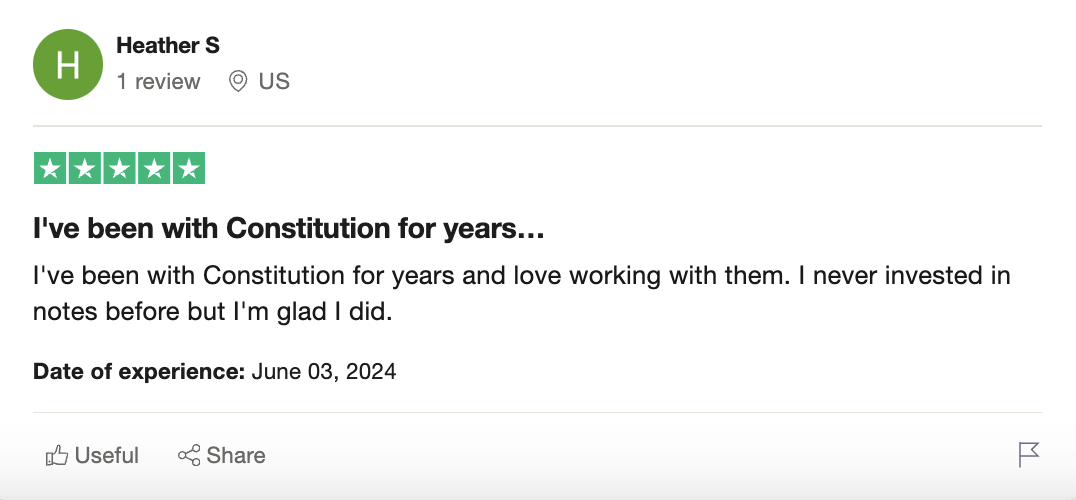

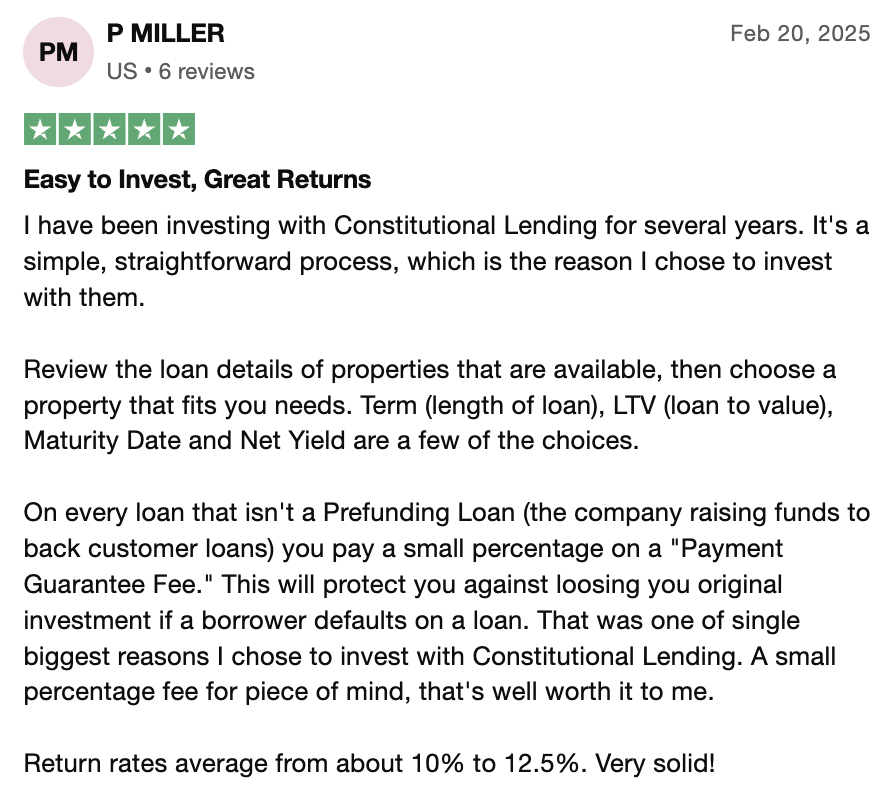

Here’s what investors say about our real estate debt investment products:

Let’s dig deeper into these factors.

Factor #1: Earn 10% to 14% Interest Returns

Our loans have interest rates of 10% to 14%, which the borrower pays monthly until the end of the term.

This interest rate allows our investors to earn higher annualized returns than what’s typical with most asset classes.

Borrowers pay this higher rate due to our fast closing times. We can fund loans in as little as 4 days, while banks take 60 to 90 days. Many borrowers prefer paying a higher rate to ensure a smooth closing, rather than waiting 60 to 90 days and risk losing the deal.

Additionally, if a borrower misses a monthly interest payment, we cover it ourselves for up to six months. This gives us enough time to renegotiate with the borrower or go through the foreclosure process, sell the property, and use the sale proceeds to recover the loan balance. (More on this below)

However, our investors almost never need the payment guarantee because our borrowers are experienced, have strong track records, and rarely miss a payment.

Factor #2: Collect Your Entire Principal Investment After 6–12 Months

Another limitation with many alternative investment platforms is their long holding periods. Alternative assets are typically illiquid, so platforms often prevent withdrawals for multiple years. Even when the holding period is over, some platforms only let you withdraw a certain percentage of your principal at a time.

However, at Constitution Lending, we maximize investor liquidity by originating short-term, hard money loans with terms between 6 and 12 months. When the loan ends, your entire principal investment becomes available again, which you can withdraw, reinvest into more real estate loans, or diversify into other asset classes. This type of liquidity is uncommon among alternative assets.

Factor #3: You are Secured by a Property Worth Significantly More Than the Loan Amount

The third benefit of investing in Constitution Lending real estate loans is that your principal is protected by a first claim on a property worth more than the owed amount. We typically lend up to 75% of a property’s value, with the borrower providing the remaining funds as a down payment.

This 25% borrower equity cushion protects your principal investment from market downturns or losses in the property’s value. It means that the property’s market value can fall by 25%, and because debtors are paid first and in full from any sale, you can still recover your entire principal investment.

For example, say you invest in a $750,000 loan secured by a $1 million single-family home. If property values decline and that $1 million property can now only be sold for $750,000, you’ll recover your entire principal investment, and the borrower’s $250,000 equity takes the hit. The borrower has to lose their entire equity investment before the principal is affected.

Read more: How to Invest in Debt Secured by Real Estate (Earn 10% to 14% Annually)

Additional Benefits of Constitution Lending Real Estate Loans

You Get a Payment Guarantee on All Loans

We’re so confident in the quality of our borrowers that we offer a payment guarantee on all loans.

This means that if the borrower stops paying, we pay you up to 6 months of interest payments out of our own pocket. During these 6 months, we try to reach a resolution with the borrower so they start paying again, or liquidate the underlying property and use the proceeds to recover the owed amount.

Our Borrower Default Rate is Less Than 2%

Our payment guarantee is rarely needed due to the quality of our borrowers: experienced real estate investors with deep expertise and spotless payment histories.

As a result, the percentage of borrowers who stop paying, also known as the default rate, is less than 2%. The average default rate on real estate loans in the U.S hovers around 4%.

Our Financial Interests Align with Yours

A major factor that sets Constitution Lending apart from most alternative investment platforms is that we actually have our money in all the investment options featured on our platform. That’s because we’ve made these loans ourselves; our money is invested alongside yours, ensuring our financial incentives align to keep the loan performing.

Most alternative investment platforms don’t invest their own money in the listed opportunities. They pool investor capital like a fund manager, and choose what to invest in, but they aren’t personally invested. If investors lose money, the platform doesn’t lose a cent.

How to Start Investing in Our Real Estate Loans

- Create an investment account with Constitution Lending. All you need to do is enter your full name and email address; it takes under 5 minutes.

- Once you’re logged in, you’ll land on your main dashboard. This displays all currently available loans that Constitution Lending has originated and made available for fractional investment. Each loan listing provides information you need to conduct proper due diligence, including LTV, interest rate, loan term, purchase price, exit strategy, and internal risk rating.

- Click on any loan listing to get a deeper look at the details, such as as-is and after-repair LTV, remaining loan balance, borrower credit score, management fees, and note position.

- Before you invest, you'll need to link a funding source to your Constitution Lending wallet. The platform accepts funding from two primary sources: bank accounts or individual retirement accounts (IRA).

- Upon funding your wallet, investing in a specific loan is straightforward. Navigate to the loan you want to invest in and click the "Fund This Loan" button located in the bottom-right corner of the loan details page.

- Once you've made an investment, you'll be taken to your portfolio dashboard, where you can track the performance of all your investments. This dashboard displays your active investments, monthly income, portfolio performance, payment history, and upcoming maturities.

- You receive interest payments from borrowers on the first day of each month, which you can withdraw or reinvest.

- When a loan reaches maturity, you receive your full principal investment back. Since most of our loans have terms of 6-12 months, you can access your capital relatively quickly.

Invest in Our High-Yield Real Estate Notes Starting with Just $1,000

Open an investment account here to browse our real estate note options and start investing.

2. Yieldstreet

Yieldstreet has positioned itself as a prominent alternative investment platform for investors seeking exposure beyond traditional assets. Its core appeal lies in providing access to private market investments — such as real estate debt, private credit, private equity, art finance, and other niche asset classes — that were once reserved exclusively for institutions or ultra-wealthy individuals.

The platform streamlines access to these opportunities by packaging them into curated offerings, making the private markets ecosystem more approachable for everyday investors.

For those looking for built-in diversification, Yieldstreet also offers multi-asset investment funds that spread exposure across several sectors. This provides a practical entry point for investors who don't want to evaluate individual deals one by one.

However, Yieldstreet comes with significant limitations that investors should consider. Many offerings are illiquid, meaning funds are typically locked up until the investment reaches maturity, sometimes for several years. Some deals are only open to accredited investors, limiting accessibility for many potential participants.

Most importantly, the risk profile can vary significantly from one offering to another. While the platform emphasizes due diligence, these investment opportunities still involve substantial credit risk, market risk, and the potential for total losses. Unlike regulated financial services with SIPC protection or guaranteed payment features, Yieldstreet investments offer no capital protection. Past performance of individual offerings has been mixed, and the platform's disclosures make clear that investors could lose their entire investment.

Read more: Top 5 Yieldstreet Alternatives | Higher Returns & More Liquidity

3. Fundrise

Fundrise has become one of the most widely recognized alternative investment platforms, primarily due to its ability to simplify access to private real estate investment. Rather than requiring investors to analyze individual properties or large development deals, Fundrise bundles real estate assets into portfolios, called eREITs and eFunds, designed to offer diversified exposure with relatively low minimums.

One of Fundrise's strengths is its accessibility for wealth management purposes. Non-accredited investors can participate, and minimums start low, which is rare in the alternative investment space. The interface is user-friendly, and the investing process is straightforward, making it well-suited for beginners seeking passive real estate exposure.

However, there are significant trade-offs that financial advisors often point out to clients. Fundrise is not designed for liquidity, and redemptions are severely limited. The platform may even deny redemption requests entirely during certain periods.

The investment funds also carry the risks typical of real estate development, such as market downturns, construction delays, cost overruns, or lower-than-expected cash flow. Unlike first-lien real estate notes, Fundrise investors have no direct claim on underlying properties and must rely entirely on the platform's management decisions.

For informational purposes, investors should understand that past performance has varied significantly across different time periods and market cycles.

Read more: 5 Best Fundrise Alternatives for Higher Yields and More Liquidity

4. AcreTrader

AcreTrader has carved out a distinctive niche as an alternative investment platform by giving investors access to farmland, an asset class that has historically been stable and difficult to enter.

Instead of purchasing entire farms, users can invest fractionally in individual parcels, allowing them to gain exposure to agricultural land without operational responsibilities.

The platform operates with a rigorous due diligence process that rivals traditional asset managers. Each farm undergoes soil analysis, valuation reviews, and tenant vetting before it reaches the marketplace. Investors typically earn returns through a combination of annual cash distributions from rental income and long-term land appreciation.

Given farmland's reputation as a resilient, low-volatility asset class, one that often performs independently of traditional assets, AcreTrader appeals to those building a diversified portfolio beyond conventional equities and real estate investment trusts.

However, farmland investments come with substantial limitations. Namely, they are inherently illiquid, with typical holding periods of 5 to 10 years. Minimums can be significantly higher than other alternative platforms, often $15,000 or more, and most offerings require accredited investor status.

5. American Hartford Gold (AHG)

American Hartford Gold (AHG) has grown into a well-known precious metals provider for high-net-worth individuals looking to diversify their portfolios with physical gold and silver. The company focuses on coins and bars, offering both direct purchases and precious metals IRAs for investors who want to hold these assets inside retirement accounts.

One of AHG's strengths is its emphasis on customer support and advisory services. Investment representatives guide investors through each step, from account setup to product selection, which can be helpful for first-time precious metals buyers. The platform also provides access to secure storage options for IRA accounts, giving investors a way to hold physical metals without managing logistics themselves.

However, investors should be aware of the significant challenges associated with precious metals. Pricing can be far less transparent than other investment platforms, and premiums over spot price may vary substantially depending on the products recommended. These premiums directly impact returns, especially in the short term.

Another critical consideration is liquidity. Precious metals are not liquid in the same way as traditional assets; selling often involves working through the company's buyback program, where resale values may fall well below expectations depending on market conditions.

Unlike regulated broker-dealer platforms subject to FINRA oversight, precious metals dealers operate under different regulatory frameworks. For informational purposes, investors should verify any provider's credentials through appropriate regulatory databases and understand that precious metals investments offer no principal protection or guaranteed returns.

6. Vinovest

Vinovest is an alternative investment platform that allows individual investors to access fine wine and whiskey as physical assets. Rather than buying shares in investment funds, investors actually own bottles or casks, with Vinovest handling sourcing, storage, insurance, authentication, and sale.

One of Vinovest's key strengths is accessibility: you can begin with as little as $1,000 for wine or $1,750 for whiskey, which significantly lowers the barrier to entry in these luxury asset markets.

The platform offers two main investing paths: a managed portfolio, where Vinovest makes selection and rebalancing decisions, and a trading marketplace that functions like a stock exchange for wine. On this marketplace, you can place bids for individual bottles, trade in real time, and potentially liquidate holdings without fixed lock-up periods.

However, Vinovest carries substantial risks and limitations that make it unsuitable for most serious alternative investment strategies. Wine and whiskey are illiquid compared to traditional assets; selling can take months, and many bottles never find buyers at expected prices.

There are ongoing management fees covering storage, insurance, and valuation, plus additional selling fees when transactions occur. Since this asset class is highly niche, market demand is unpredictable and subject to changing consumer preferences. The platform's disclosures acknowledge that past performance varies widely and that investors may experience significant losses.

7. Hiive

Hiive is a fintech platform specializing in secondary markets for pre-IPO private company shares. It functions as a marketplace for late-stage, venture-backed companies, allowing accredited and institutional investors to buy or sell equity before companies go public.

One of Hiive's advantages is transparency relative to other private market investment providers. Users can view live bids and asking prices, as well as historical trade data, providing insight into how the private markets are valuing different companies.

For sellers, Hiive makes it easier for early employees, founders, and existing investors to unlock value from private shareholdings. For companies, the platform provides a regulated venue to facilitate secondary transactions while maintaining some control over share transfers.

However, Hiive involves substantial risks that make it unsuitable for most investors' core allocations. Because publicly available information on private companies is limited, valuation data can be incomplete or highly speculative. The platform provides estimates but warns they may not reflect material, non-public information that could dramatically affect company values.

The securities traded on Hiive are unregistered and carry extremely high risk levels. These are speculative investments with a real possibility of total loss. Unlike regulated investment funds or platforms with payment guarantees, Hiive offers no capital protection whatsoever.

Invest in Our Capital-Protected First-Lien Real Estate Notes and Earn 10% to 14%

You can learn more about our real estate debt options by opening an investment account here.