Private money lenders can close significantly faster than banks and traditional lenders, making them ideal for real estate investors looking to beat fast cash buyers to undervalued properties.

But the lender you choose still plays an important role in how fast and reliably you can close. Many lenders, particularly lower-quality ones, promise to close in 7 to 14 days, only to drag out for 30+ days. Sometimes, they’ll even reject your loan application right before closing.

Here are two questions that can help you identify and avoid slow, flaky lenders:

- How quickly can they issue quotes, pre-approval letters, and term sheets? If this takes multiple days, it shows they have slow internal processes, which will likely affect how fast you can close. The fastest lenders can issue quotes, pre-approval letters, and term sheets in under 24 hours.

- Are they a direct lender or broker? Many “private lenders” are actually brokers submitting your application to another lender. This is a problem because they only know if you qualify after underwriting. If a lender finds issues late into underwriting, it can lead to last-minute rejections. Instead, choose a direct lender. They know their requirements and can tell if you qualify immediately after reviewing your paperwork.

In this article, we discuss the top five private money lenders for residential real estate while considering the two factors mentioned above.

We start by exploring how we, Constitution Lending, use tools like our automated pricer and documents portal to reliably close within 7 to 14 days and avoid last-minute rejections and other unnecessary drama.

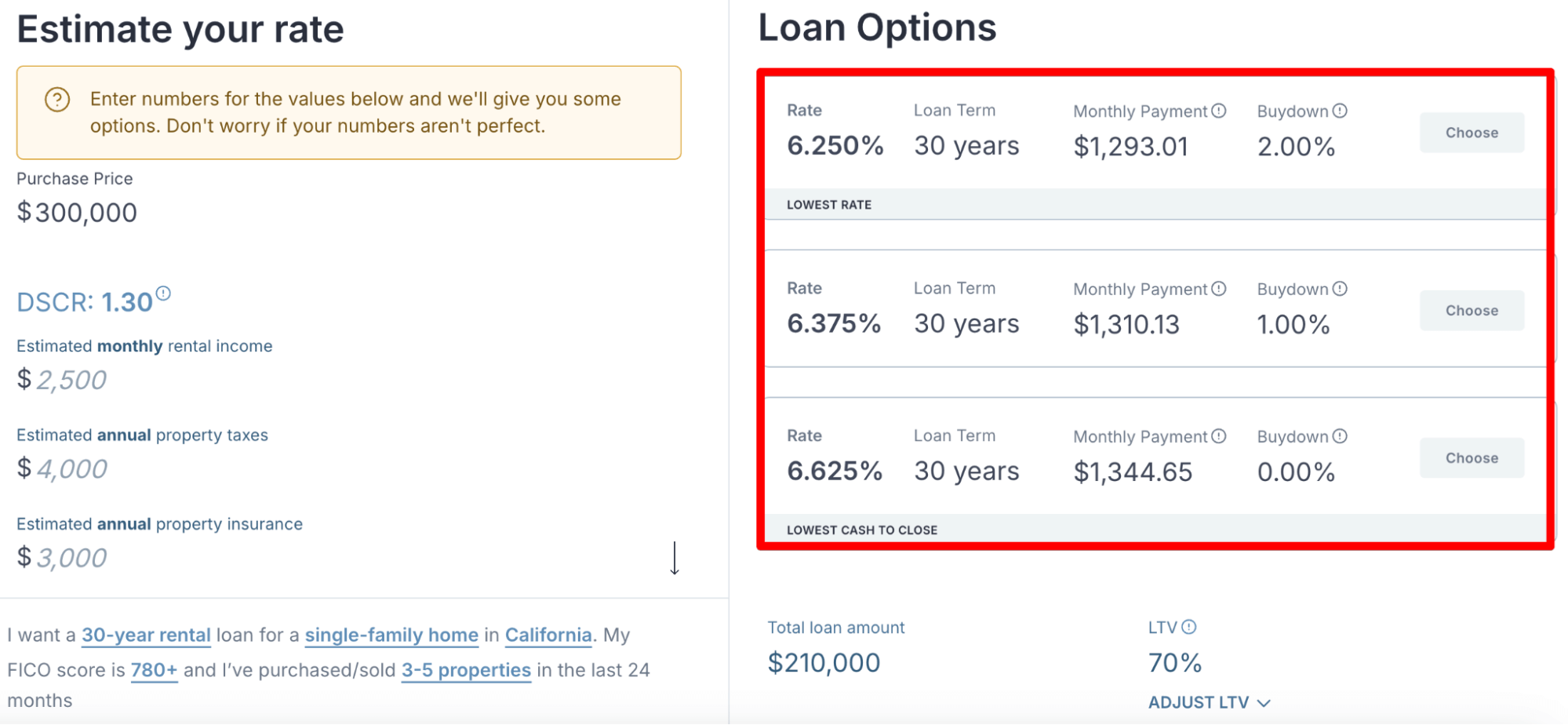

Use our automated pricer to experiment with different loan scenarios and generate instant quotes.

1. Constitution Lending: A Direct Private Lender That Helps Borrowers Compete with the Speed of Cash Buyers

We founded Constitution Lending after investing in real estate for several years and struggling with slow and flaky lenders.

Most hard money lenders promised on their website that they would close in 7 to 14 days. But when we partnered with them, we learned how slow they actually were and that we’d be lucky to close in 30 days.

In addition, many hard money lenders said we could qualify with no problem, but when it was time to close, they’d reject our loan application without an explanation. (We later learned this was due to brokers and not issues with our applications; more on that below.) This caused us to lose out on millions of dollars in undervalued real estate.

We intentionally designed Constitution Lending’s internal processes with these experiences in mind.

Here’s what borrowers say about our lending process and closing times:

Factor #1: How Quickly Can They Issue Quotes, Pre-approval Letters, and Term Sheets?

The entire application and approval process takes under five minutes, thanks to our automated pricer and documents portal. Here’s what it looks like:

- Use our automated pricer to generate instant quotes and see what interest rates and loan terms you qualify for. Simply answer a handful of questions, such as where the property is located, the type of property, whether you plan to flip, construct, or buy and hold, your desired loan amount, and what your FICO score is.

- You’ll find three quotes on your right, each outlining your interest rates, monthly payments, loan terms, and buydowns.

- It’s worth testing various rental income scenarios, down payments, purchase prices, and LTV ratios to see how each variable influences your quotes and closing costs.

- Choose the quote you prefer, enter your full name and email address, and download a pre-approval letter and term sheet.

- At the same time, we email you a link to our documents portal that explains the required paperwork for the loan you applied for. This may include proof of insurance, entity documents, and scope of work, among others. You can submit these documents through the portal and message a loan officer if you have any questions.

- We provide a guaranteed answer on whether you qualify within one to two hours of receiving your paperwork. No last-minute rejections or surprises.

- We close the loan with the title company within 7 to 14 days. If you need to close even faster and you have all the necessary documents ready, we can close in 4 days.

Compare this to many other private money lenders, where you need to book an appointment with a loan officer, talk with them for an hour explaining the deal, wait 3 to 5 business days for a quote, pre-approval letter, and term sheet; and only then can you begin submitting documents so they can start underwriting.

Factor #2: Are They a Direct Lender or Broker?

As we alluded to earlier, loan brokers are a big reason behind why last-minute rejections are so common in real estate lending. We’ve heard cases of borrowers getting rejected on the day of closing.

This is because brokers don't lend money themselves. They are middlemen and, therefore, not the decision-maker on your loan.

So, it’s common for loan brokers to think you can qualify, but they can’t be 100% sure until after the actual lender has completed underwriting, which can take weeks. If the lender flags something deep into underwriting that the broker missed, you may get rejected at the last minute despite being told early on that you can qualify.

With Constitution Lending, we are a direct hard money lender since we’re lending you our own money.

Our advantage is that we know our requirements through and through since we’ve originated hundreds of loans. We can look at your application, immediately know if you qualify, and guarantee a smooth closing.

If we spot an issue in your application, we flag it immediately after you submit your documents, allowing you to correct it before reapplying and avoid wasting time waiting.

Being a direct lender also allows us to tailor loan terms to your unique needs and make exceptions that most brokers cannot make; we don’t have to wait on another lender’s approval. For example, if you purchased an undervalued property but your credit score or LTV prevents you from qualifying, we can make exceptions to help you qualify.

Read more: 5 Best DSCR Lenders & How to Choose

Types of Residential Real Estate Loan Programs We Offer

Constitution Lending offers three main types of real estate loans:

- DSCR loans: These are 30-year financing options used to purchase or refinance rental properties. They are underwritten on the rental property’s income and expenses. We don’t consider the borrower’s finances and don’t require tax returns or pay stubs. This makes them perfect for real estate investors with non-W2 income and high debt-to-income ratios who can no longer qualify for conventional bank loans. You can learn more about the pros and cons of DSCR loans here.

- Fix-and-flip loans: These are short-term loans used to purchase and rehab investment properties. Like DSCR loans, our fix-and-flip loans are underwritten on the property’s financials, particularly its as-is value relative to its after-repair value. We don’t consider the borrower’s financial profile. You can learn more about our fix-and-flip borrower requirements here.

- New construction loans: These hard money loans are used for building rental or commercial properties from the ground up. We fund both the purchase of the land and the materials required for the construction. Our primary underwriting focus is on the total cost to build the property versus its post-construction market value. No tax returns, income verification, or other personal financial documents needed.

Apply for Affordable and Flexible Terms with Constitution Lending

Answer 8 quick questions in our automated pricer to instantly see the interest rates and loan terms you qualify for.

2. Griffin Funding

Griffin Funding is a private hard money lender based in San Diego that serves real estate investors across the U.S. Many reviewers like how they are willing to make exceptions and structure loans around real-world scenarios rather than rigid, traditional lending criteria.

This means that regardless of whether you’re purchasing an investment property, refinancing, or scaling a rental portfolio, they can help you qualify.

Many reviewers also talk about the quality of their team and how they will take the time to understand your investment goals. They can also recommend loan products that align with your strategy, whether it’s DSCR loans, bridge financing, or bank-statement financing options for self-employed borrowers.

Execution speed is another advantage. Griffin Funding claims on its website that it can close quickly, though it doesn’t provide a concrete timeframe.

That said, there are a few limitations with Griffin Funding that are worth noting. Namely, they don’t say anything about using automated tools, such as a loan pricer or a documents portal, to speed up the application and underwriting process. Instead, borrowers will have to complete an application form or speak with one of their loan officers.

3. Insula Capital Group

Insula Capital Group is a private money lender that helps investors who cannot qualify for bank loans purchase residential real estate and close quickly.

Founded in 2015, Insula combines deep real-estate experience with efficient underwriting to offer a broad suite of loan products, including short-term fix-and-flip loans, construction financing, and long-term permanent loans.

One of Insula’s biggest competitive advantages is its speed. According to their website, they can underwrite within 24 hours and fund most loans within a week.

Insula also prioritizes building long-term relationships with borrowers: their Investor Support Program provides mentorship, education, and private lending solutions for first-time real estate investors.

Importantly for residential and commercial real estate investors, Insula offers hard-money-style loans that don’t require mountains of documentation or credit checks during the prequalification stage. That makes them more accessible, especially for buyers who may not fit the rigid credit profile that traditional banks demand.

4. Vaster

Vaster is a direct private money lender that operates in Florida and New York. They serve a wide range of borrowers such as buy-and-hold investors, beginner investors, foreign nationals, construction companies, flippers, and more. This makes them a good option for anyone needing creative real estate financing that traditional banks often can’t provide.

One of Vaster’s standout strengths is its fast execution. Many reviewers talk about how their team can turn around loan approvals and closings much quicker than big banks, which is crucial when you’re competing for undervalued investment opportunities.

Vaster offers a broad mix of residential investment loan products, including bridge loans, acquisition financing, and cash-out options.

Another advantage is the professionalism of their lending team. They communicate clearly, keep the process moving, and support borrowers at every step of the transaction, reducing the usual friction that comes with fast-moving real estate deals.

5. RCN Capital

RCN Capital is an alternative real estate lender based in Connecticut and one of the largest in the U.S. They have built a reputation over the years as a dependable option for residential real estate. Their main financing products include fix-and-flip projects, rental portfolios, and short-term bridge loans.

One of RCN’s biggest advantages is the structure of their loan products. Their programs are designed with real-world investing in mind: competitive leverage, straightforward terms, and underwriting that focuses on the asset’s potential rather than only the borrower’s credit profile. This makes them accessible to borrowers who may not qualify for traditional bank financing but still operate strong, profitable investment strategies.

Investors often highlight RCN’s speed and communication. Their process is streamlined from application to closing, with a team that stays responsive and proactive throughout the deal.

RCN also stands out for its consistency. Many investors appreciate that their guidelines are transparent and applied predictably, which helps avoid the last-minute surprises that are common with other private lenders. Their experience in residential investment financing also means they understand renovation budgets, ARVs, and cash-flow models at a deeper level than generic lenders.

Qualify for Affordable Private Money Loans with Constitution Lending

Get instant quotes and find out which interest rates you qualify for with our automated pricer.

Frequently Asked Questions

What are the benefits of using a private money lender for real estate investments?

The main benefit of using a private money lender is that you can close faster than with banks. Private money lenders like Constitution Lending can close within 7 to 14 days, while banks usually take 60 to 90 days. In addition, many banks often reject your application at the last minute and right before closing. Private money lenders have simpler requirements, so they can tell if you qualify immediately after submitting your application.

What are the disadvantages of private money lenders?

The main disadvantage of private money lenders is that they charge slightly higher interest rates and upfront costs than large banks. However, many borrowers don’t mind this due to the fast closing speeds of private money lenders. They’d rather pay a higher rate and guarantee a smooth and fast closing than wait 60 to 90 days for a lower interest rate at a bank.

How does private money lending work in real estate?

Private money lending is when private companies or investors lend money to real estate borrowers instead of a large bank. The advantage of private lenders is that borrowers can close in 7 to 14 days, instead of waiting 60 to 90 days with banks.