DSCR loans are financing products approved based on a property’s cash flow and not the borrower’s personal financial profile. This means your real estate borrowers can qualify without submitting tax returns, proof of income, or other paperwork banks usually require.

But even with these benefits, the lender you choose determines the service quality you can deliver to borrowers and their overall experience working with you.

We regularly hear from brokers that they lost borrowers because the lender said they could close within 7 to 14 days, and after communicating that timeframe to the borrower, closing dragged out for 30 to 60 days.

It’s also common for lenders to review a borrower’s paperwork, say they can qualify no problem, but then reject their application at the last-minute, sometimes on the day of closing. This damages the trust you’ve built with borrowers.

Here are two ways brokers can spot slow and flaky DSCR lenders:

- How fast can they issue quotes, term sheets, and pre-approval letters? If this takes 24 hours or more, it’s a sign their internal processes are slow, and this will likely delay closing. Choose a lender that can issue instant term sheets, quotes, and pre-approvals; this shows they have the tools to move applications forward quickly.

- Verify that they are a direct lender. The leading factor behind last-minute rejections is when brokers work through other brokers instead of going to a direct lender. (We explain this in more detail below.) Instead, confirm that the lender you’re partnering with is the one actually making the loan. This gives you a direct line to the decision-maker and reduces the likelihood of last-minute rejections.

In this article, we compare 7 DSCR wholesale lenders against the factors listed above.

We start by discussing our DSCR wholesale program and how we help brokers consistently close within 7 to 14 days, without stressing over last-minute rejections and drama.

Use our automated DSCR loan pricer to generate instant quotes, term sheets, and underwriter-reviewed pre-approval letters for your borrowers.

1. Constitution Lending: A DSCR Wholesale Lender that Closes in 7 to 14 Days

Constitution Lending is a direct DSCR lender designed to help brokers close fast and reliably.

We founded Constitution Lending after being real estate investors for nearly a decade and getting stuck working with lender after lender who can’t deliver.

Many lenders promised they could close quickly, but they rarely kept their word. Additionally, they would review our application and say we qualify, but then reject it on the day of closing without giving a reason. We lost millions of dollars of undervalued real estate because of this.

We know these delays and last-minute rejections can strain your relationships with borrowers and put you in awkward situations, so we designed our application, underwriting, and approval process specifically to avoid that.

Here’s what clients say about our fast and reliable closing times:

Factor #1: Our Automated Pricer and Documents Portal Allows You to Reliably Close within 7 to 14 Days

With our automated DSCR loan pricer, you can generate instant term sheets, quotes, and underwriter-reviewed pre-approval letters, giving us the foundation to underwrite and close within 7 to 14 days.

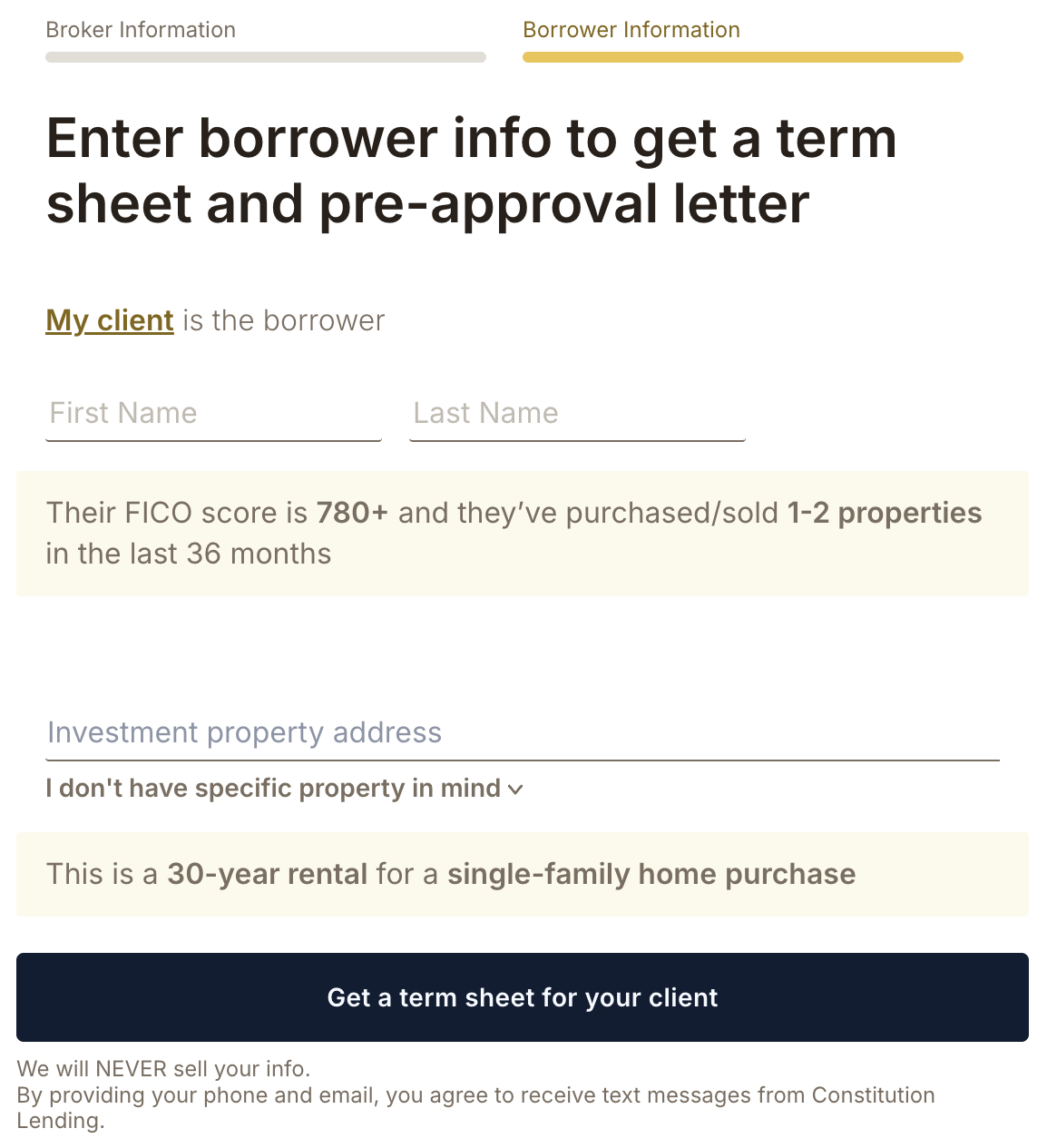

Here’s what the application process looks like for brokers:

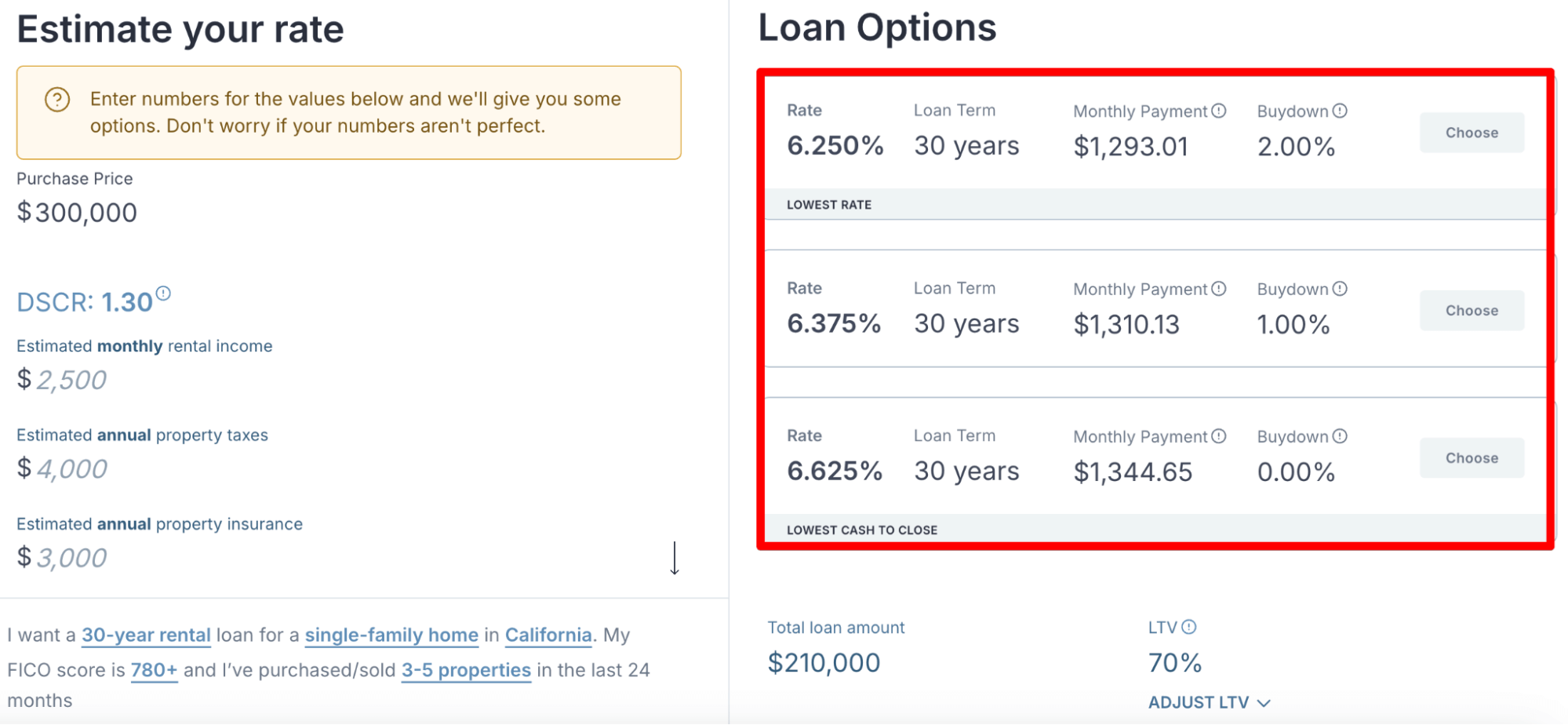

- Enter your borrower’s credit score, years of real estate experience, desired loan amount, the property purchase price and location, and estimated rental income into our automated pricer.

- On the right-hand side of your screen, you’ll see the interest rates, terms, and buydowns your borrower can qualify for.

- We recommend testing various LTVs, DSCRs, and rental income figures to see how each of these factors influences quotes.

- Enter your full name and email address, and you’ll be able to download a copy of the quote, an underwriter-reviewed pre-approval letter, and a term sheet, which you can send to your borrower.

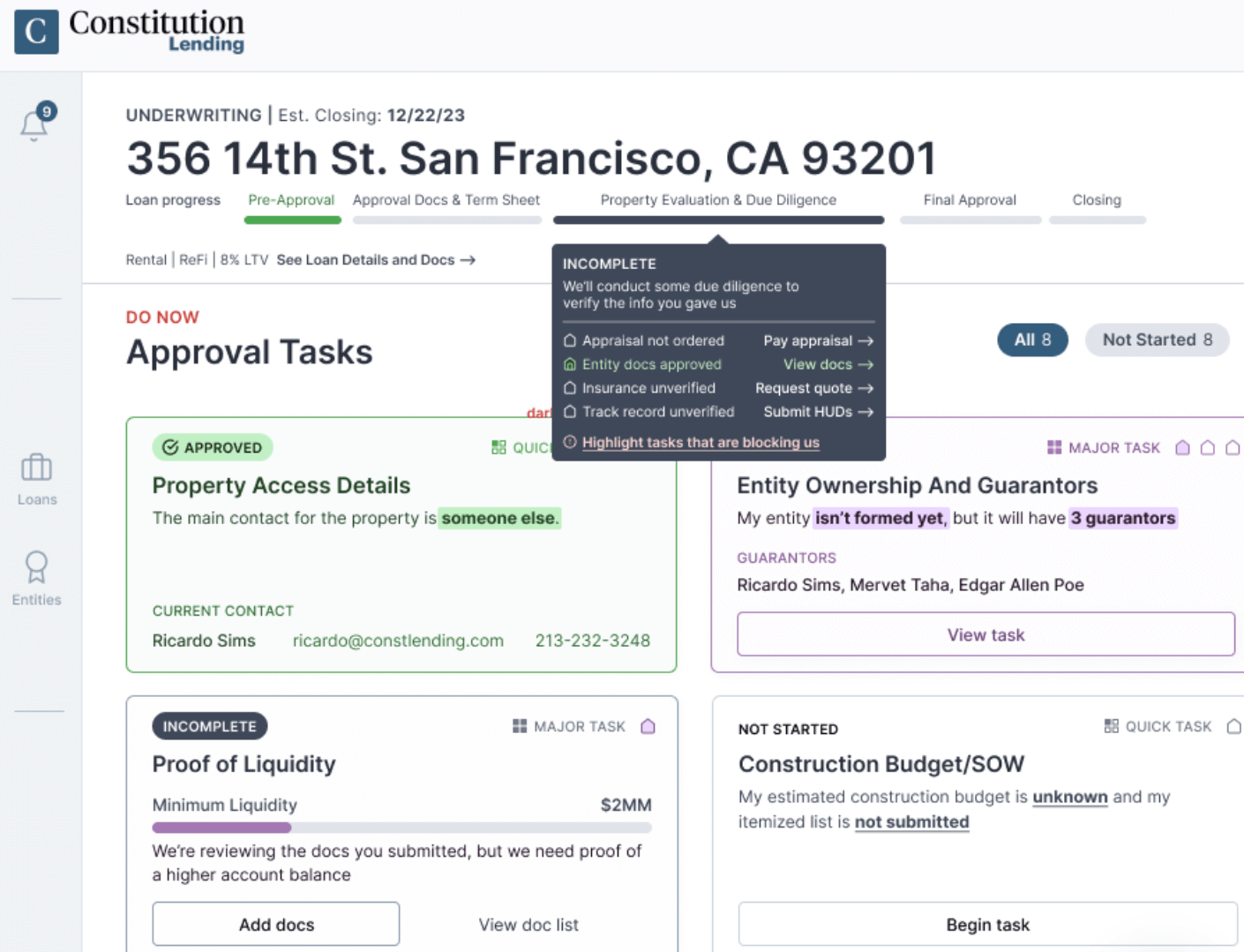

- You get access to a documents portal that lists all the required paperwork and lets you submit everything directly. That way, you don’t have to worry about last-minute paperwork requests or going back and forth with a loan officer about required documents. You can also message or call your loan officer through the portal if you have any questions or requests.

- As soon as you submit the required documents, we review them and email you immediately to let you know whether your borrower qualifies. We won’t send you a rejection at the last minute.

- We close the loan within 7 to 14 days. In some instances where brokers needed to close faster than this and had all the required paperwork ready, we’ve closed in just 4 days. Essentially, we can close as quickly as you can submit documents.

Compare our process to how most DSCR lenders operate.

You’ll need to talk with a loan officer for an hour to explain the deal, and it may take multiple business days for them to get back to you with a quote. Due to slow, inefficient internal processes, your application often sits untouched for days before someone reviews it and sends you a term sheet and a pre-approval letter.

Factor #2: We Are a Direct Lender, So You Don’t Have to Stress About Last-Minute Rejections

As we mentioned above, last-minute rejections are a major challenge brokers face when sourcing funds for borrowers. It’s common for lenders to say a borrower will qualify, only to reject their application shortly before closing. This reflects poorly on you because borrowers may view you as unreliable.

Last-minute rejections happen when brokers unknowingly partner with other brokers instead of going straight to the source of the funds. This is surprisingly common in real estate lending; we’ve even seen deals with up to 3 brokers on it.

The problem with partnering with another broker is that they aren’t the ones making the loan, and therefore, aren’t the decision-maker. They may think your borrower can qualify, but for a concrete answer, they need to submit your application to the lender for underwriting. If the lender finds problems weeks into underwriting, you can get rejected at the last minute, and after already telling your borrower they can qualify.

But when you partner with a direct lender like Constitution Lending, you’re talking to the people funding the loan.

We know our requirements inside and out because we’ve lent hundreds of millions of dollars, so we can give you a concrete yes-or-no immediately after reviewing your borrower’s application. This way, you get guarantees early in the application process that you will close. We don’t have to send your application to another lender and wait for them to finish underwriting before telling you whether you qualify.

If we see an issue with an application, we will let you know as soon as you submit paperwork, so you can notify your borrower early.

Read more: 5 Best LLC Mortgage Lenders: Guide for Borrowers

Secure Reliable Wholesale DSCR Loans with Constitution Lending

Use our automated DSCR loan pricer to generate and share instant quotes, term sheets, and pre-approval letters with your borrowers.

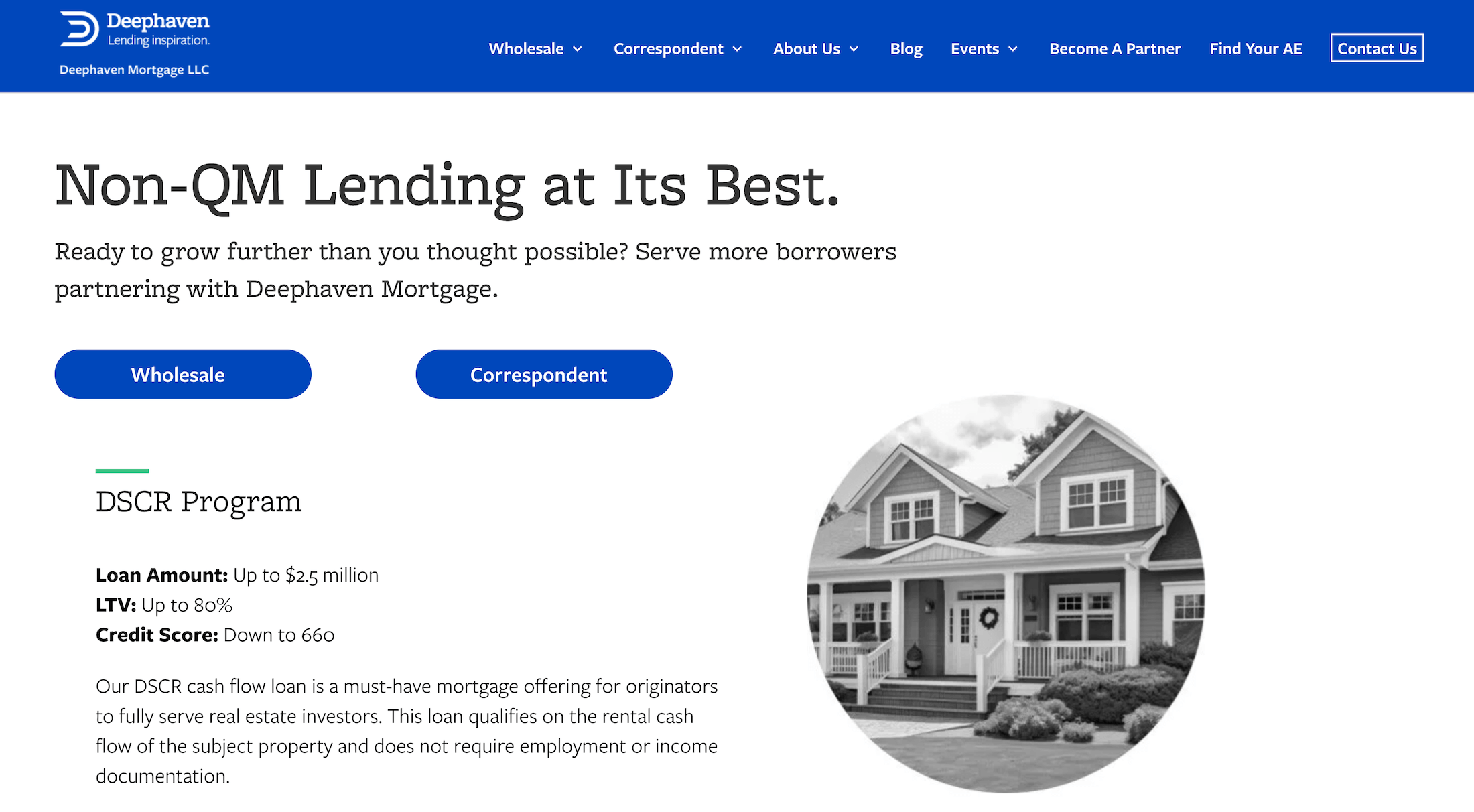

2. Deephaven Mortgage

Deephaven Mortgage is a non-QM lender specializing in alternative mortgage products for borrowers who don't qualify for conventional financing through traditional banks. As a wholesale lender, they work exclusively through approved mortgage brokers and correspondent lenders rather than directly with borrowers.

DSCR Loan Requirements:

- Minimum DSCR: 1.0 required

- Credit Score: Starting at 620 FICO

- Loan Amounts: $100,000 to $3,000,000

- Loan-to-Value: Maximum 80% LTV for purchases, 75% for refinances

- Loan Terms: 30-year fixed-rate terms available

- Income Verification: No personal income documentation required

Deephaven's credit score requirement of 620 makes their program accessible to borrowers with moderate credit, though this is higher than some competitors who accept scores as low as 600. Their maximum loan amount of $3 million accommodates most investment property purchases, from single-family homes to small multifamily properties.

How to Apply

As the broker, you’ll work with an account executive from Deephaven’s broker network who will support you through the full process, including the application, document collection, and underwriting requirements.

You’ll also act as the primary point of contact between your borrower and Deephaven from submission through closing. Because everything runs through the broker channel rather than directly with the lender, timelines can occasionally be longer than with a direct-to-consumer lender.

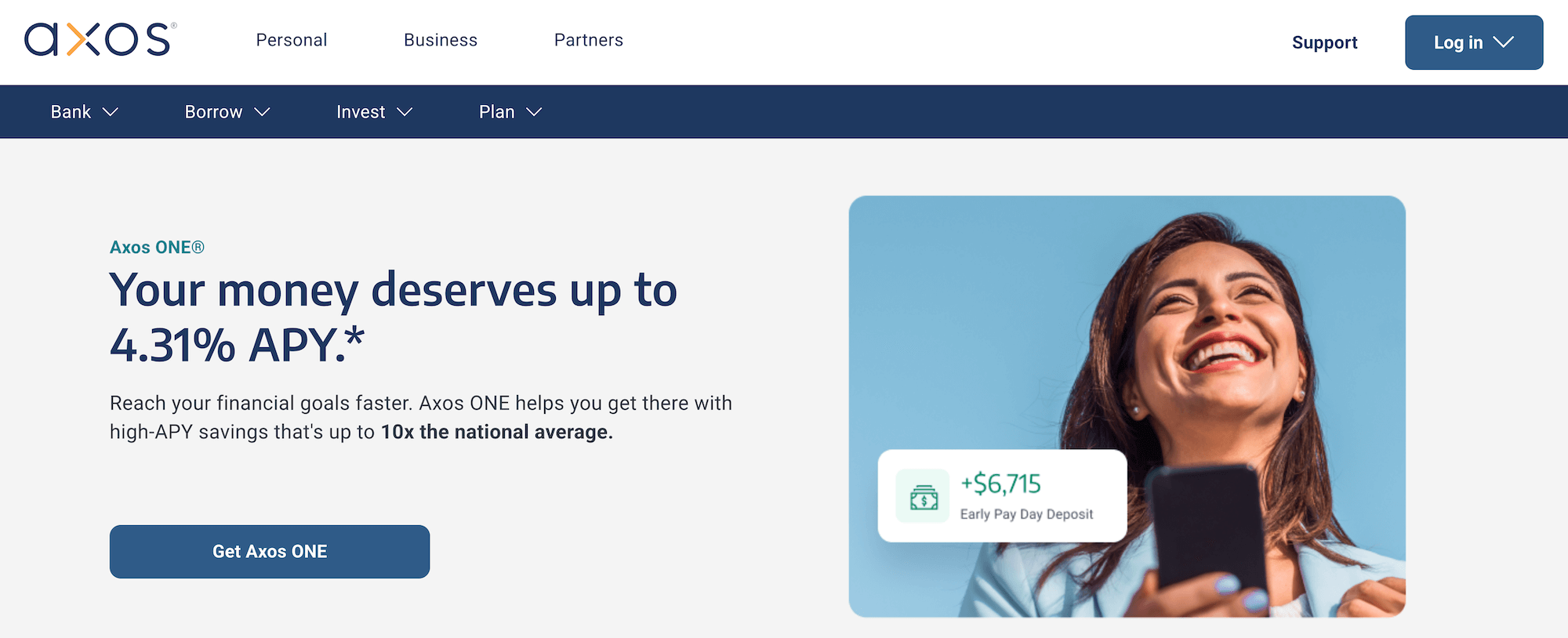

3. Axos Bank

Axos Bank is a strong lending partner for brokers, offering a wide range of competitive loan products and a streamlined digital platform. Brokers appreciate the efficient submission process, flexible underwriting options, and responsive account executives, making Axos a solid choice for both conventional and non-QM deals.

DSCR Loan Requirements:

- Minimum DSCR: 1.0 required

- Credit Score: Minimum 680 FICO

- Loan Amounts: $150,000 to $5,000,000

- Loan-to-Value: Maximum 75% LTV for both purchases and refinances

- Loan Terms: Fixed and adjustable-rate options available

- Property Requirements: Must be rent-ready at closing

Axos Bank's higher credit score requirement of 680 may exclude some investors, but their loan amounts up to $5 million make them suitable for larger investment properties. Their 75% maximum LTV for both purchases and refinances is more conservative than some competitors, requiring larger down payments or more equity for cash-out refinances.

The rent-ready requirement means the property must be in move-in condition at closing, which can be challenging for investors purchasing properties that need rehabilitation work.

How to Apply

You can begin the application process by completing an online form on Axos Bank's website or contacting their commercial lending team directly. As a direct lender, their loan officers can make underwriting decisions without consulting third-party funders, potentially reducing the risk of last-minute loan rejections.

Their digital banking platform may offer more streamlined document submission compared to traditional banks, though closing times will depend on property appraisals and underwriting complexity.

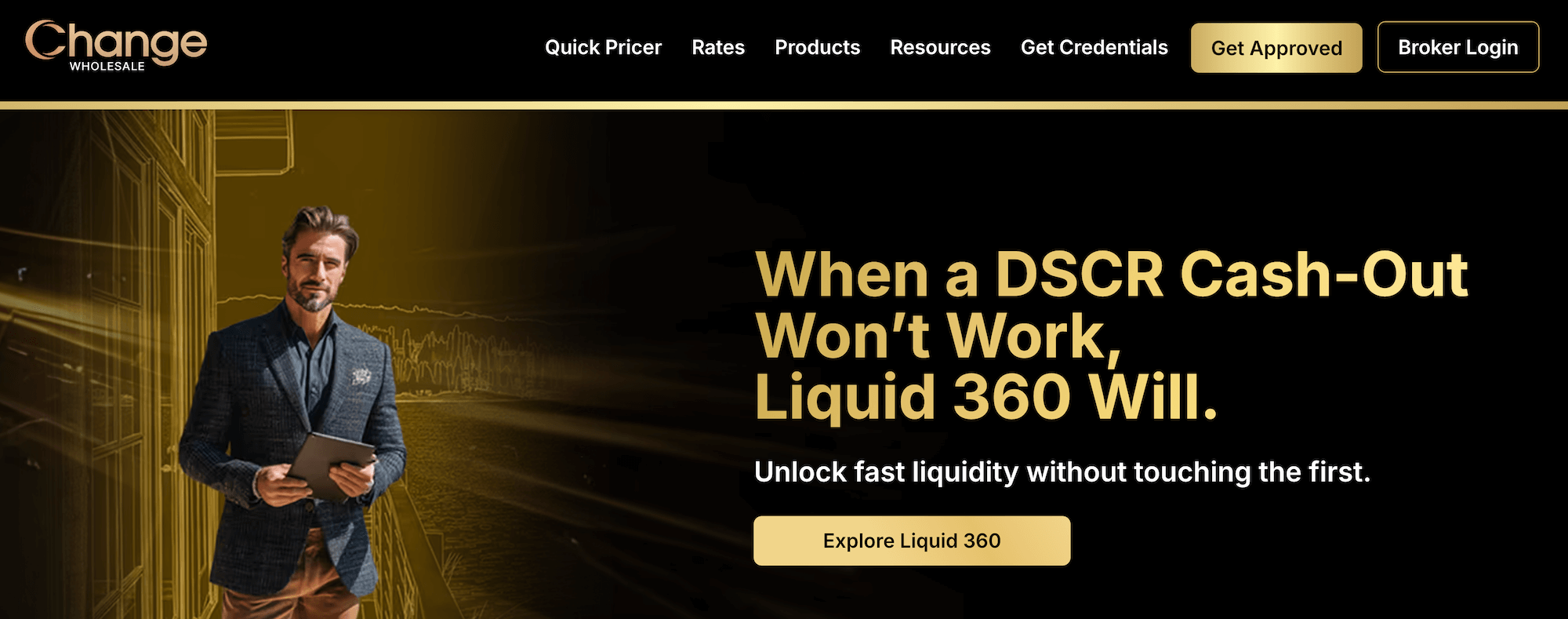

4. Change Wholesale

Change Wholesale focuses exclusively on non-QM mortgage products, including specialized DSCR programs for real estate investors. Like other wholesale lenders, they work through mortgage brokers rather than directly with borrowers.

DSCR Loan Requirements:

- Minimum DSCR: 0.75 accepted

- Credit Score: Starting at 640 FICO

- Loan Amounts: $75,000 to $3,000,000

- Loan-to-Value: Maximum 80% LTV for purchases, 75% for cash-out refinances

- Loan Terms: 30-year fixed terms available

- Property Types: Single-family and 2–4 unit properties eligible

Change Wholesale's minimum DSCR of 0.75 is notably flexible, accepting properties where rental income covers only 75% of debt obligations. This can be valuable in high-cost markets where properties may not achieve full debt service coverage but still represent solid investments.

Their lower minimum loan amount of $75,000 makes them accessible for investors purchasing properties in lower-cost markets, while the $3 million maximum accommodates most investment scenarios.

How to Apply

To apply as a broker with a wholesale lender, start by submitting your broker profile and NMLS information through the lender’s broker portal.

Once approved, you can submit borrower applications, upload required documents, and track loan status online. You’ll work closely with the lender’s account executives, who guide you through underwriting requirements and any additional documentation needed.

As the primary point of contact, you manage all communication with the borrower while ensuring the loan process runs smoothly from submission to closing.

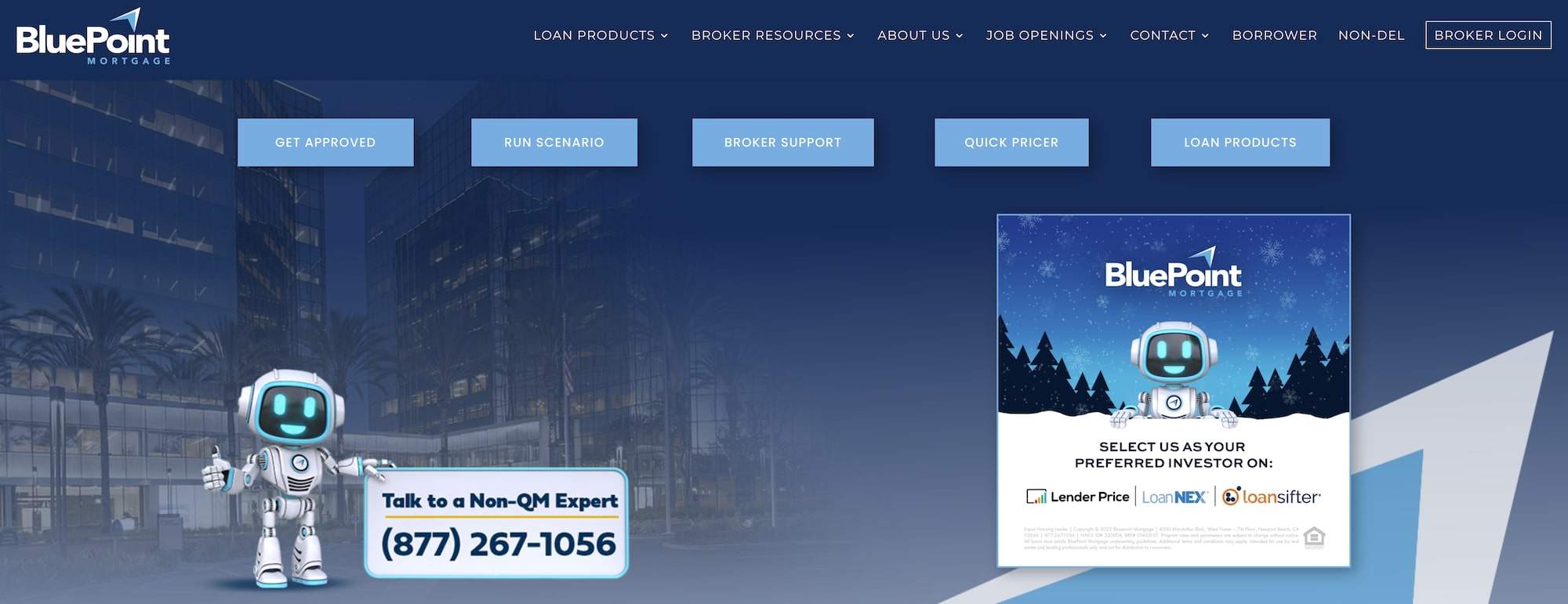

5. BluePoint Mortgage

BluePoint Mortgage offers DSCR loans alongside other investor loan programs across multiple states. They position themselves as a provider of flexible lending solutions for real estate investors who need alternatives to conventional financing.

DSCR Loan Requirements:

- Minimum DSCR: 1.0 required

- Credit Score: Minimum 660 FICO

- Loan Amounts: $100,000 to $2,500,000

- Loan-to-Value: Maximum 80% LTV for purchases, 75% for refinances

- Payment Options: Interest-only payment options available

- Property Types: 1–4 unit residential properties accepted

BluePoint's interest-only payment option can be attractive for investors focused on maximizing cash flow from their rental properties. This feature allows borrowers to pay only interest for a specified period, typically the first few years of the loan, before transitioning to principal and interest payments.

Their credit score requirement of 660 is moderate compared to other lenders, though still higher than the most flexible options available. The maximum loan amount of $2.5 million may limit options for investors purchasing higher-value properties.

How to Apply

Enter your borrower’s credit score, years of real estate experience, desired loan amount, property purchase price and location, and estimated rental income into BluePoint Mortgage’s Quick Pricer for fast, accurate, and tailored loan options.

6. JMAC Lending

JMAC Lending operates as a direct lender providing short- and long-term financing options for real estate investors nationwide. Their DSCR program is part of a broader portfolio of non-QM loan programs.

DSCR Loan Requirements:

- Minimum DSCR: 1.0 typically required

- Credit Score: Starting at 680 FICO

- Loan Amounts: $200,000 to $5,000,000

- Loan-to-Value: Maximum 75% LTV for most loan products

- Loan Terms: 30-year amortization available

- Property Types: Single-family and multifamily properties eligible

JMAC's higher minimum loan amount of $200,000 targets investors purchasing mid- to high-value properties, potentially excluding smaller investment opportunities. However, their maximum loan amount of $5 million accommodates larger multifamily acquisitions.

The 75% maximum LTV across all products requires larger down payments compared to lenders offering 80% financing, but may result in better interest rates due to the lower risk profile.

How to Apply

As a direct lender, JMAC allows you to apply online or speak directly with their loan officers. They evaluate properties based on cash flow potential rather than borrower income, focusing on the debt service coverage ratio during underwriting.

Direct lending relationships often provide clearer communication about loan status and requirements, potentially reducing surprises during underwriting.

7. Carrington Mortgage Services

Carrington Mortgage Services includes DSCR loans as part of their non-QM lending portfolio. As a full-service mortgage lender, they offer comprehensive financing solutions for first-time and experienced real estate investors seeking alternatives to conventional mortgage products.

DSCR Loan Requirements:

- Minimum DSCR: 1.0 required

- Credit Score: Minimum 640 FICO

- Loan Amounts: $100,000 to $3,000,000

- Loan-to-Value: Maximum 80% LTV for purchases, 75% for refinances

- Loan Terms: Fixed-rate loan terms available

- Property Requirements: Investment properties must be rent-ready

Carrington's credit score requirement of 640 is relatively accessible, though their rent-ready property requirement means the subject property must be in condition to generate immediate rental income. This can limit opportunities for investors who prefer to purchase properties needing renovation.

Their loan amounts of $100,000 to $3 million cover most investment property scenarios, from entry-level rental properties for first-time homebuyers to larger multifamily investments.

How to Apply

You can begin the application process by completing Carrington's online application or contacting their loan origination team directly. A loan officer will review your borrower’s investment property details and guide you through their underwriting requirements and documentation process.

As a full-service lender, Carrington handles all aspects of the loan process internally, which can provide more consistent communication compared to working through brokers.

Get Your Borrowers Funded Quickly and Reliably with Constitution Lending

Answer a few quick questions in our automated pricer and instantly provide your borrowers with quotes, term sheets, and pre-approval letters.

Frequently Asked Questions

How do I find the best DSCR wholesale lenders for real estate investments?

Find the best DSCR wholesale lenders by comparing their minimum DSCR requirements, maximum loan-to-value ratios, closing speeds, and whether they're direct lenders versus brokers. Look for lenders offering instant quotes, competitive interest rates starting around 6.75%, and the ability to close within 7–14 days.

How does a DSCR wholesale lender evaluate rental income for loan approval?

DSCR wholesale lenders evaluate rental income using appraisal rent schedules, comparable market rents, or existing lease agreements to establish the property's income-generating potential. They focus on the property's ability to cover its debt obligations with a minimum DSCR typically between 0.75 and 1.0, rather than the borrower's personal income or employment history.

How do DSCR wholesale lenders evaluate loan eligibility?

DSCR wholesale lenders evaluate loan eligibility primarily based on the property's cash flow capacity, loan-to-value ratio, and borrower credit score (typically 660 minimum). They consider property type, location, condition, and the calculated DSCR ratio while requiring minimal personal financial documentation compared to traditional mortgages, making qualification faster and more straightforward.

How do I find a reliable DSCR wholesale lender for my investment property?

Find reliable DSCR wholesale lenders by choosing direct lenders who can provide instant quotes and term sheets within 24 hours. Verify they offer competitive rates, high LTV options up to 80%, and can close within 7–14 days. Constitution Lending exemplifies reliability with automated pricing tools and definitive approval answers before underwriting begins.