As a DSCR lender, many first-time borrowers don’t realize they need to form an LLC (Limited Liability Company) before closing on a property. Borrowers can’t hold the property in their personal name.

DSCR loans require an LLC because they’re business-purpose loans approved based on the property’s income and expenses, not your personal income and debt-to-income ratio like a regular consumer loan.

To simplify things, we’ve put together this guide to walk you through how to set up an LLC for DSCR financing, the paperwork you need to prepare and submit, and the loan requirements you must meet.

We also explain how we designed our application process and paperwork requirements to help borrowers close as quickly and hassle-free as possible.

Use our automated pricer to generate an instant quote and see what interest rates and terms you qualify for. We can close in as little as four days.

How to Apply for a DSCR Loan Using an LLC

You’ll need the following LLC documents to close a DSCR (debt service coverage ratio) loan:

- Articles of Organization: These documents prove that you’ve legally formed an LLC with the state. You can create an LLC by applying on your state’s Secretary of State website and paying the filing fee. You’ll receive your Articles of Organization within 30 minutes.

- An EIN number: After receiving your Articles of Organization, use it to apply for an EIN number on the IRS website. You’ll need to complete a short form, and your EIN will be issued immediately.

- An operating agreement: You’ll need to draft an operating agreement outlining the structure and operation of your LLC. You can find plenty of operating agreement templates online. With these three documents, your LLC is now set up for a DSCR loan.

Note: You don’t need these documents to apply for or start processing a DSCR loan — you only need them at closing. Many borrowers simply form an LLC on the day of closing since the application only takes a few minutes. This is called a “To Be Formed” LLC.

Here’s what the entire DSCR loan application process looks like:

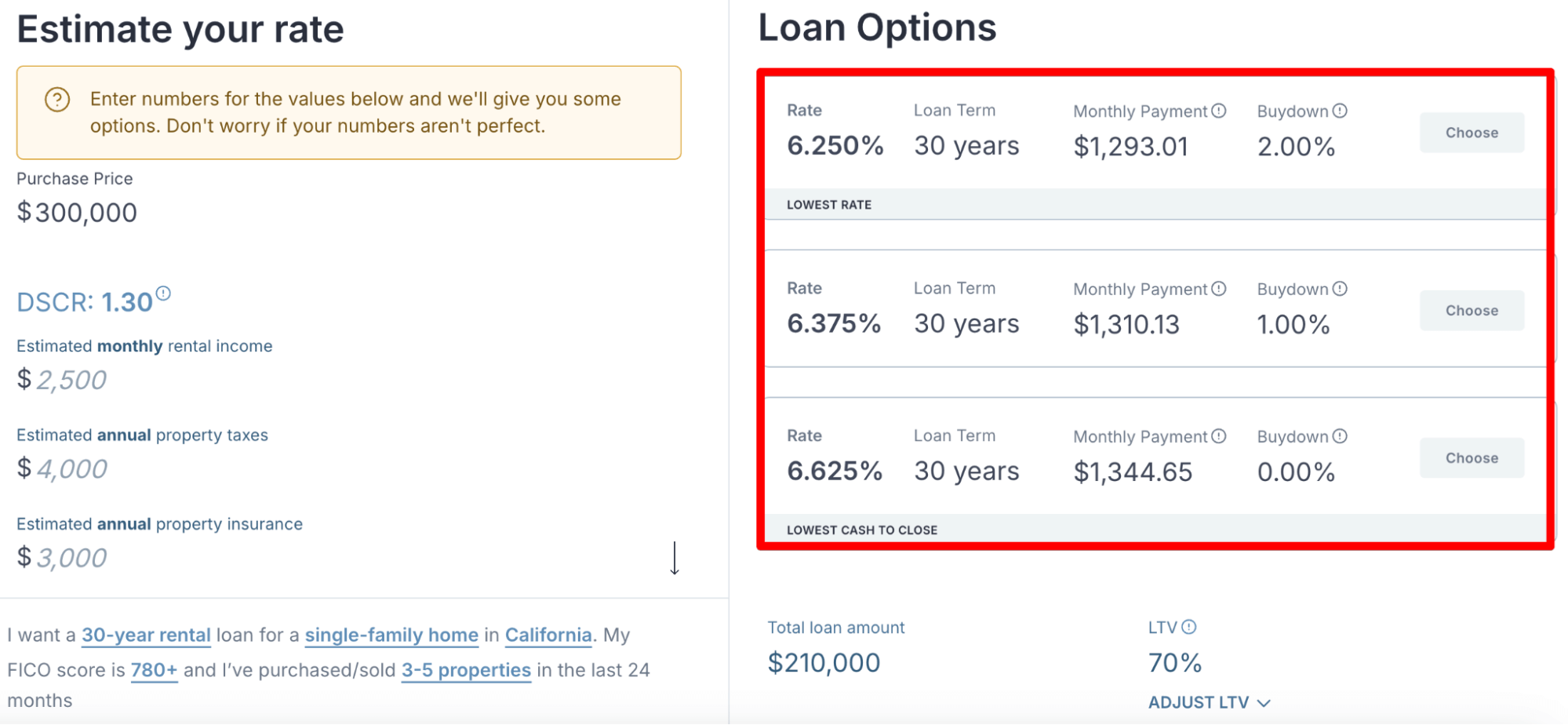

- Use our DSCR pricer to generate instant quotes specifying the interest rates, loan terms, and buydowns you qualify for. All you have to provide is the property’s type, location, purchase price, projected cash flow, your target loan amount, whether it's a purchase or cash-out refinance, and your FICO score.

- We suggest testing different rental income metrics, LTVs (loan-to-value), and loan amounts to see how they affect your quotes.

- Once you see a quote that you like, click on it, enter your name and email address, and you’ll be able to download a pre-approval letter and term sheet.

- We provide you with access to our borrower portal, which outlines all the necessary paperwork. This includes a purchase contract, three months' bank statements, an appraisal report, lease agreement (if applicable), and proof of insurance. You only need to submit the three LLC documents at closing.

- We begin underwriting and, within a few hours, provide you with a concrete answer on whether you qualify. You don’t have to worry about last-minute drama and rejections.

- On the day of closing, apply for your Articles of Organization and EIN, and draft an operating agreement.

- At closing, you’ll need to sign the following documents, either virtually or in-person: a promissory note, deed of trust, and closing disclosure. Once you wire the down payment, your LLC officially owns the property.

Read more: 7 Best DSCR Lenders Florida: No Income or Tax Returns Required

3 Main Eligibility Requirements for Securing a DSCR Loan

As we mentioned above, DSCR loans are real estate investing loans underwritten on a property’s income potential and expenses, not the borrower’s personal finances.

So you don’t have to worry about meeting personal income, debt-to-income, or tax return requirements like traditional loans.

Instead, DSCR lenders mainly look for:

- A down payment of 20% to 25%

- A DSCR of 0.75 or more

- A credit score of 660

Down Payment of 20% to 25%

Most DSCR lenders, including Constitution Lending, will finance between 75% and 80% of a property’s market value, with the borrower covering the rest as a down payment.

If you’re buying, that means you’ll need a down payment of 20%–25%. Naturally, the larger your down payment, the better your interest rates and prepayment penalties.

If you’re refinancing, DSCR lenders typically finance 65%–75% of the property’s market value.

DSCR of 0.75 or More

DSCR is another key factor lenders consider.

You can calculate DSCR by dividing the property’s cash flow by its total debt obligations, including loan repayments, insurance, HOA fees, and taxes.

For example, if a multifamily investment property generates $2,000 in net operating income (NOI), and its expenses are $1,600, its DSCR is 1.25. (2,000 ÷ 1,600 = 1.25.)

Typically, lenders prefer funding deals with a DSCR above 1.0, because that means the owner can pay for all expenses without using their own personal income, and still have funds remaining to weather vacancies and repairs.

That said, Constitution Lending has a minimum DSCR requirement of just 0.75; we’ve lowered it in response to rising loan rates, making it easier for real estate investors to qualify.

Credit Score of 660 or More

Even though DSCR loans are underwritten based on the property’s financials, borrower credit scores still matter, as lenders want to gauge a borrower’s financial responsibility.

Think of it this way: DSCR shows the quality of the deal, and credit score shows the quality of the borrower.

So, DSCR lenders will run a credit check when you apply to assess your credit score and see if you’ve been making debt payments on time.

Most lenders want to see a credit score above 680 to 700. However, at Constitution Lending, we’ve funded deals with real estate investors who have credit scores as low as 660.

How to Choose the Right DSCR Lender & What Sets Constitution Lending Apart From Other Lenders

The lender you choose plays a critical role in how quickly and stress-free the loan process will be.

High-quality DSCR lenders can close quickly and with minimal fuss. In contrast, bad lenders usually take months to close, have endless paperwork demands, and will sometimes reject your application on the day of closing.

Here are two ways you can test the quality of a DSCR lender:

- Consider how quickly they can issue pre-approval letters and term sheets, as this is a good indicator of how quickly they can close.

- Verify whether they’re funding the loan themselves or if they’re just a broker connecting you to a lender. Brokers are a common cause behind last-minute rejections.

How Quickly Can They Issue Pre-Approval Letters and Term Sheets?

Closing speed matters — it can make the difference between snagging an undervalued, income-generating property and losing it to a fast-cash buyer.

A good way to gauge a lender’s closing speed is by how fast they issue term sheets. If it takes more than 24 hours, that’s a red flag that their internal processes are slow and they’re unlikely to close quickly.

With Constitution Lending, we consistently close DSCR loans within 7 to 14 days — and in as few as 4 days when borrowers face a tight deadline. This speed is possible thanks to our automated DSCR pricer and documents portal.

You can generate multiple quotes by just entering a few details about your deal into our pricer. Once you’ve chosen a quote, you can download a term sheet and loan approval letter immediately. No need to explain the deal to a loan officer for an hour and wait multiple days for a quote.

At the same time, we send you access to a documents portal where you can submit all the required paperwork: purchase contract, proof of insurance, bank statements, etc. Once you submit everything, we start underwriting and close within 7 to 14 days.

Are They Funding the Loan Themselves or Are They a Broker?

Steer clear of loan brokers, as they’re a common culprit in last-minute complications.

Brokers are problematic because they aren’t the ones funding your loan and don’t have a say in whether you are approved. Instead, they send your documents to the actual hard money lender, where they will underwrite them over multiple weeks before deciding whether you qualify.

The issue arises when brokers say early on in the application process that you can qualify, but then, when the lender finds a problem during underwriting and near the closing date, you’re left without funding and could lose your earnest money deposit.

Constitutional Lending is a direct lender; in other words, we are the ones funding your loan. We know our loan requirements inside and out and can guarantee a smooth closing process; you don’t have to brace yourself for last-minute drama.

Here’s what borrowers say about our DSCR loan options:

Secure Competitive DSCR Loans with Constitution Lending

Get an instant DSCR loan quote and view available terms, interest rates, and buydown options.

Frequently Asked Questions

What are the benefits of using a DSCR loan for an LLC?

The main benefit of using a DSCR (debt service coverage ratio) loan for an LLC is that qualification is based on the property’s cash flow, not your personal income.

Unlike a conventional mortgage loan, lenders don’t require tax returns or debt-to-income (DTI) ratios. They simply evaluate whether the property’s rental income can cover its expenses. This makes DSCR loans much easier for borrowers to qualify for, particularly those who are self-employed, have complex finances and write-offs, or high DTI ratios.

Is it hard to qualify for a DSCR loan?

No, qualifying for a DSCR loan is often easier than a conventional loan because you don’t need to provide personal income verification, tax returns, or debt-to-income documents. Instead, lenders focus on the property’s DSCR — its income compared to expenses. For example, if a property earns $1,200 in rent and has $1,000 in expenses, the DSCR is 1.2, which most lenders consider sufficient.

Can an LLC get a loan for real estate?

Yes, an LLC can secure a real estate loan, but not a regular consumer mortgage. Instead, borrowers apply for a non-QM loan like a DSCR (debt service coverage ratio) loan, which is designed for LLCs purchasing long-term rental properties.

What credit score is needed for a DSCR loan for an LLC?

Most lenders require a minimum credit score of 700–720 for DSCR loans. At Constitution Lending, you only need a 660 credit score, though higher scores can help you secure better loan terms and lower interest rates.

Can I refinance my property with a DSCR loan?

Yes, you can refinance an investment property with a DSCR loan, even without a current tenant. At Constitution Lending, we offer low-interest DSCR refinancing, lending up to 70% of the property’s value. This is a great option for investors who want to use their equity to purchase another property.

Do all DSCR Lenders have the same qualification rules?

No, not all DSCR lenders have the same qualification rules. At Constitution Lending, we offer some of the easiest-to-qualify-for DSCR loan products with only three requirements: a 20%–25% down payment, a credit score of 660, and a minimum DSCR ratio of 0.75.