A real estate investment loan is any financing used to purchase a non-owner-occupied property that generates income.

There are various types of loans real estate borrowers can use to purchase investment properties, with each option being a viable choice depending on your investment strategy.

In this article, we review the main types of investment property loans, covering who it is for, their pros and cons, eligibility requirements, and the application process.

At the end, we explore the key factors that real estate borrowers should consider when selecting a lender, ensuring they close quickly and have access to the lowest possible interest rates.

Constitution Lending is a private lender that offers low-interest DSCR and hard money loans. You don’t need to submit tax returns, pay stubs, or any of the other information banks require. Use our automated pricer to explore loan scenarios and check what you qualify for.

1. DSCR Loans: Best for Long-Term Buy & Hold Strategies

DSCR (debt-service coverage ratio) loans are financing products approved based on the ratio of an investment property's cash flow to its expenses.

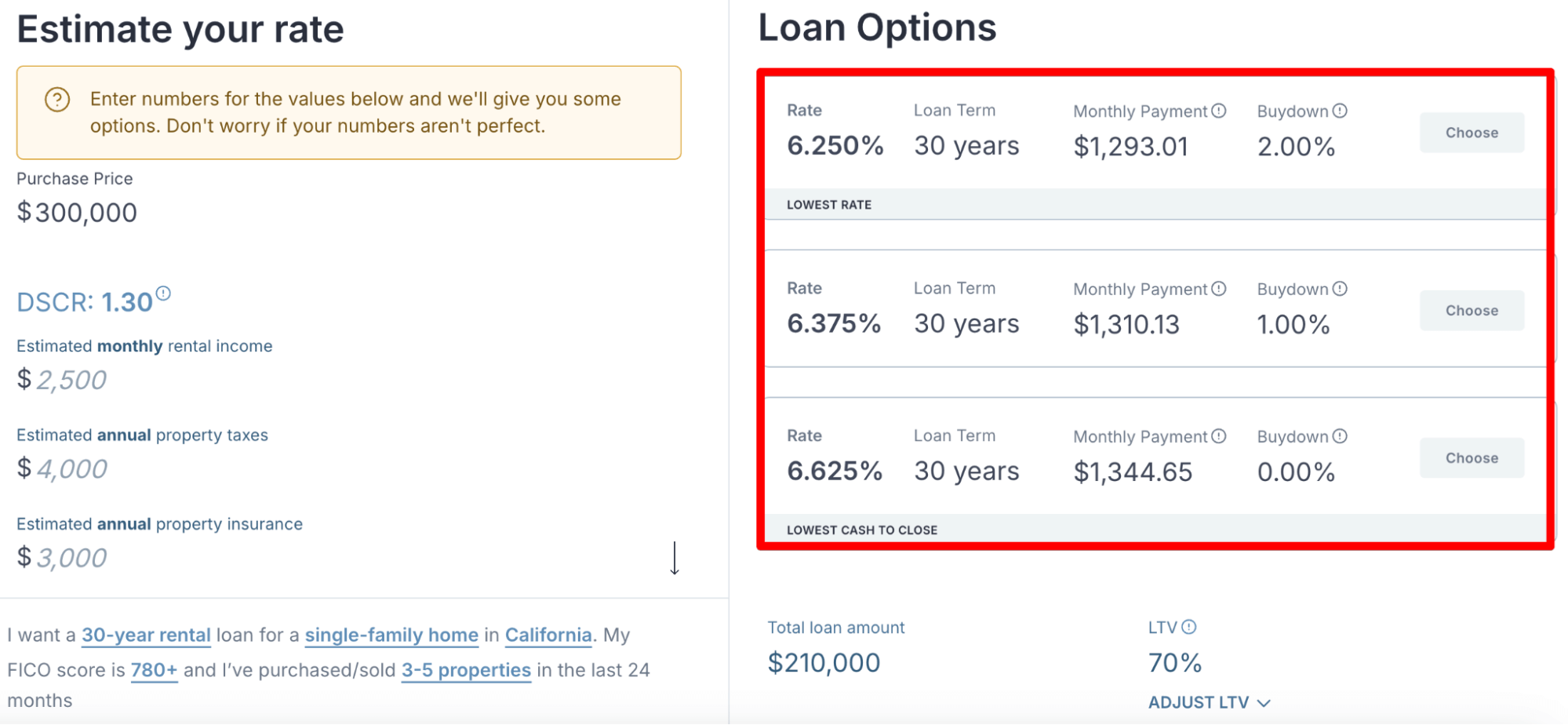

For example, say a single-family home can rent for $1,300 per month, and the mortgage payment plus other expenses is $1,000. That property’s DSCR is 1.3, and this ratio is what lenders focus on when underwriting. Naturally, the higher the DSCR, the better your chances of approval and the lower your interest rate. Most DSCR lenders look for a DSCR of 1.0, but we can fund deals with a DSCR as low as 0.75.

DSCR lenders don’t underwrite a borrower’s income, debt-to-income ratio, or employment history. So, you don’t have to submit personal income verification, pay stubs, tax returns, or other financial documents that conventional mortgage loans require.

As a result, DSCR loans tend to be best for investors with a few financed investment properties who want to scale their portfolio, but can no longer qualify for conventional mortgages because of a high debt-to-income ratio.

DSCR loans are also common among self-employed borrowers. That’s because banks make it difficult for self-employed borrowers to qualify for conventional financing; they must submit years of balance sheets, business tax returns, and profit and loss statements, among other documents, to show their business is profitable. DSCR loans require none of that.

Read more: 5 Best LLC Mortgage Lenders: Guide for Borrowers

How to Qualify for a DSCR Loan at Constitution Lending

We can’t speak for all DSCR lenders, but for our DSCR loan program, borrowers only need to meet three requirements:

- Have a DSCR of 0.75 or higher

- Have a down payment of 20% or more

- Have a minimum credit score of 660

How to Apply for a DSCR Loan at Constitution Lending

- Use our automated pricer to generate an instant quote. Our pricer requests basic information, including the property’s location, type, your credit score, and the desired loan amount. It gives you three quotes that look like this:

- Feel free to play around with the rental income, loan amount, property value, and LTV to see how they impact your quotes.

- Once you’ve selected a quote, you can download a term sheet and a pre-approved letter immediately.

- You’ll receive a link to your documents portal, where you can view and submit the required paperwork (e.g., bank statements, entity documents, proof of insurance). Once you’ve submitted everything, we close in 7 to 14 days.

Read more: DSCR Loan Pros and Cons: A Detailed Guide for Investors

2. Hard Money Loans: Best for Fix-and-Flip Investment Strategies

Hard money loans are short-term financing options commonly used by borrowers to fix and flip investment properties. They address two of the biggest challenges real estate flippers face: the need for fast funding and flexible requirements.

- Fast funding: When applying for a bank loan, borrowers often wait three months or more to close. This is due to all the paperwork involved and the bureaucratic nature of large banks. With hard money lenders, you can close in 7 to 14 days. At Constitution Lending, we’ve even helped flippers purchase fixer-uppers in under four days, enabling them to compete with cash buyers.

- Flexible requirements: Banks typically have strict requirements. It's unlikely that you’ll qualify if you don’t have near-perfect credit, strong income, low debt, and sufficient assets or reserves. However, hard money lenders like Constitution Lending have flexible loan requirements and can make exceptions to help you qualify.

The drawback of hard money loans is that the interest rate is higher than that of conventional bank loans, typically ranging from 10% to 14%. However, this doesn’t really matter to most flippers because the loan term is so short, usually between 6 and 18 months. Many would prefer to pay more interest and close quickly rather than waiting for a lower rate and potentially losing out on the deal entirely.

Read more: 5 Best Fix and Flip Lenders & Reviews

How to Qualify for a Hard Money Loan with Constitution Lending

Our hard money loan options have four main requirements:

- We offer a maximum LTV of 60% to 85%, meaning borrowers need to put 15% to 40% down, depending on how well they meet the rest of these requirements.

- Cash reserves equivalent to around three months of payments. This is necessary because we don’t fund the full construction at once. Instead, we fund the purchase of the property, and borrowers need to pay for repairs initially. They then invoice us, and we reimburse them within a few days.

- An after-repair LTV of 70% or less, so once the rehab is complete, the loan amount shouldn’t exceed 70% of the property’s value.

- A credit score of at least 660.

How to Apply for a Hard Money Loan with Constitution Lending

The process of qualifying for a Constitution Lending hard money loan is similar to a DSCR loan:

- Use our pricer to pull a quote. However, unlike a DSCR loan, our pricer will ask for estimated after-repair value and other fix-and-flip-specific metrics.

- You’ll find three quotes on the right-hand side of your screen detailing your interest rate, buydowns, and monthly payment.

- Choose a quote, download a pre-approval letter and term sheet, and submit all required documents through our portal.

- We close in 7 to 14 days.

3. Conventional Mortgages: Best for First-time Real Estate Investors

Conventional mortgages like FHA loans or VA loans can be a suitable option for first-time homebuyers. That’s because with your first mortgage, you can often qualify for lower interest rates and down payment requirements thanks to a low debt-to-income ratio, which makes you a safer bet in the eyes of lenders.

However, conventional loans quickly become impractical, typically after about four financed properties or once you reach a 50% DTI ratio, since your DTI becomes too high for standard underwriting.

In that case, DSCR mortgage loans become a better option for scaling your portfolio because DSCR mortgage lenders completely disregard DTI ratios and focus on the property’s financials.

Additionally, it’s worth noting that conventional bank loans typically take a considerable amount of time to close, making it challenging to capitalize on undervalued properties. Banks can take three months or more to underwrite and close, which isn’t an option when competing with fast cash buyers.

For these reasons, once investors have used conventional loans to secure a few investment properties, they often utilize DSCR loans to scale their investment portfolio further.

How to Qualify for a Conventional Mortgage Loan

The requirements for conventional mortgages will vary depending on the bank; however, they generally include:

- A good credit score; most banks require a credit score of 700 or more

- A DTI ratio below 50%

- A 3% down payment for your first property and 20% for second homes

- Two years of stable income and pay stubs to prove it

- Two years of personal tax returns

- If you’re a business owner, you’ll need to provide financial documents showing the health of your business

How to Apply for a Conventional Mortgage Loan

For most banks, you’ll need to visit a branch or schedule an appointment with a loan officer to explain the details of the deal (e.g., the purchase price, your down payment, estimated rental income, the type of property, whether it’s a single-family home, multifamily home, or condo).

From there, the loan officer will follow up with you about the necessary paperwork. This usually includes two years of tax returns, 6 months of bank statements, pay stubs, and proof of assets or reserves. If you’re self-employed, you’ll need to submit balance sheets, business tax returns, profit and loss statements, and a list of business assets.

The bank will underwrite your application and close the deal. This typically takes around two to three months. Such lengthy closing times can make it hard to compete with fast-closing cash buyers when trying to purchase an undervalued property quickly.

4. Home Equity Loans: Best for Tapping Into Existing Equity

If you have equity in your primary residence or an investment property, you can borrow against that equity and use it as a down payment to purchase another property. The property you borrowed against acts as collateral. This is known as a home equity loan or home equity line of credit (HELOC).

Home equity loans are a good option for investors who have one or numerous properties with equity and would like to scale their portfolio. They are typically disbursed as a lump sum at closing and can be used to acquire long-term rental properties or renovate and resell distressed homes.

5. Portfolio Refinance or Blanket Loans: Consolidate Multiple Loans Into One With a Lower Mortgage Rate

Another popular option for real estate investors is the portfolio loan. This type of investment property financing is designed for homeowners with multiple properties who want to simplify payments and reduce the interest they’re paying. With a portfolio loan, investors can roll their existing property loans into one, often at a lower rate, and then make a single repayment on the new consolidated loan.

This makes portfolio refinance or blanket loans a good choice for real estate investors with a portfolio of properties looking to lock in lower interest rates.

How to Choose a Real Estate Investment Lender & What Sets Constitution Lending Apart

Regardless of the type of loan and investment strategy you choose, the lender you partner with plays a crucial role in how quickly and reliably you can close. From our experience as both real estate investors and private lenders, we’ve found that most lenders tend to fall short in a few key areas:

- They take a long time to close: Most lenders claim they can close quickly, but we’ve seen they typically take 30+ days. This slow closing speed can cause you to lose deals, especially undervalued properties, to fast cash buyers. So, consider a lender’s closing speed; a good way to predict this is by testing how quickly they issue term sheets. If this takes a long time, they’ll likely take a long time to close.

- They reject your loan at the last minute: Many lenders will send you a pre-approval letter and say you can easily qualify. However, when closing approaches, they say your application has been rejected. Sometimes, they’ll reject your application on the day of closing. This happens mainly when you partner with a broker (we explain how this happens later). To avoid this, partner with a direct lender.

We faced these issues during our time as real estate investors, which is the main reason we founded Constitution Lending. Here’s how we address the issues above:

- Our automated pricer and documents portal allow us to close faster than most lenders

- We are a direct lender, so we can guarantee closing early in the application process

Our Automated Pricer and Documents Portal Speed Up Closing

Instead of using slow and outdated systems such as phone or email, we have an automated pricer that enables borrowers to price out multiple loan scenarios and generate quotes instantly, speeding up the application process.

From there, our online documents portal lets borrowers know exactly which documents they need to submit; there’s no being passed on to other loan officers and learning about new document requirements at the last minute. You can submit all documents through our portal at once.

Read more: How to Use DSCR Loans to Purchase Investment Properties

We are a Direct Lender, Not a Loan Broker

As we alluded to above, one of the biggest challenges borrowers face (in addition to slow lenders) is flaky, unreliable ones. It’s common for lenders to tell you when you first submit your application that you qualify, only to come back with a rejection letter.

This issue has become especially widespread with the growth of loan brokers. Loan brokers act as intermediaries connecting you with lenders; they aren’t lending you their own money. This means they aren’t the ones who decide whether your loan goes through or not; that’s the lender’s decision.

What commonly happens is that the broker might think you qualify, but ultimately, they must wait for the lender to underwrite before giving you a concrete decision. If the lender identifies issues late in underwriting (which can take weeks), your application may still be rejected even if the broker initially said you qualified.

At Constitution Lending, we provide the funds directly and make all lending decisions in-house. That means we can give you a clear answer on your qualification as soon as your documents are submitted.

Secure Fast Real Estate Investment Loans with Constitution Lending

Use our automated loan pricer to plot multiple loan scenarios and see what terms you qualify for.