Commercial multifamily lenders evaluate and approve loan applications on property performance (i.e., income, expenses, rent rolls, lease stability). They don’t limit how much you qualify for based on your W-2 income, debt-to-income (DTI) ratio, net worth, or cash reserves, like consumer Freddie Mac and Fannie Mae loans.

This makes them perfect for individual investors looking to purchase or refinance multifamily real estate, such as apartment buildings and mixed-use properties.

Despite the advantages of commercial multifamily financing, the lender you choose matters because it makes all the difference in how quickly (and how painlessly) you can close.

We hear stories from borrowers far too frequently about how they applied with a commercial bank or lender who advertised fast closing, only for the process to drag on for 90+ days and then get rejected right before they were supposed to close. In worst-case scenarios, they had to forfeit their earnest money deposit and lose undervalued real estate to other multifamily investors.

To avoid long closing times and last-minute rejections, evaluate the following factors in a lender:

- Check how fast they can issue term sheets, quotes, and pre-approval letters, as it’s an accurate reflection of their closing speed. Avoid lenders that take multiple business days to send term sheets because it shows they have slow internal processes that’ll likely affect closing. The fastest lenders issue same-day quotes, term sheets, and approval letters.

- Check whether they are a direct lender. Last-minute rejections mainly happen with brokers. They may think you can qualify, but if the real lender finds discrepancies in your application that the broker missed, you can get rejected several weeks in — even after receiving an early green light from the broker. Avoid last-minute rejections by going to a direct lender.

In the article below, we review seven commercial multifamily lenders on the market and compare them against the two factors above.

Use our automated loan pricer to see what rates you qualify for and generate instant quotes, term sheets, and pre-approval letters.

1. Constitution Lending

Fast, High-LTV Financing for Multifamily Properties

Before founding Constitution Lending, we were real estate investors who were burned by unreliable lenders and commercial banks countless times.

Commercial banks and lenders would claim they could close quickly, but then take months, costing us hundreds of thousands of dollars in earnest money deposits.

Additionally, they would frequently tell us we couldn't qualify the day before or on the day of closing, even after confirming early on that we met all requirements. This pattern of overpromising and underdelivering was frustratingly common.

So, we structured our multifamily investment solutions specifically to avoid these problems.

Here's what borrowers say about our reliability and speed:

Let’s discuss how Constitution Lending addresses the two pain points above: speed and reliability.

Speed: Our Automated Pricer and Documents Portal Allows Us to Close Multifamily Loans within 7 to 14 Days

The reason most commercial multifamily lenders are so slow is inefficient internal processes. After you submit an application, it often sits untouched for days before a loan officer reviews it.

Then, you must wait for a call, talk with a loan officer on the phone for an hour explaining the deal, and wait another few days for quotes and term sheets. These inefficiencies aren’t limited to the initial application process and often persist into underwriting and funding.

In our experience, the speed at which a lender provides term sheets, loan quotes, and pre-approval letters is a strong indicator of their overall closing speed.

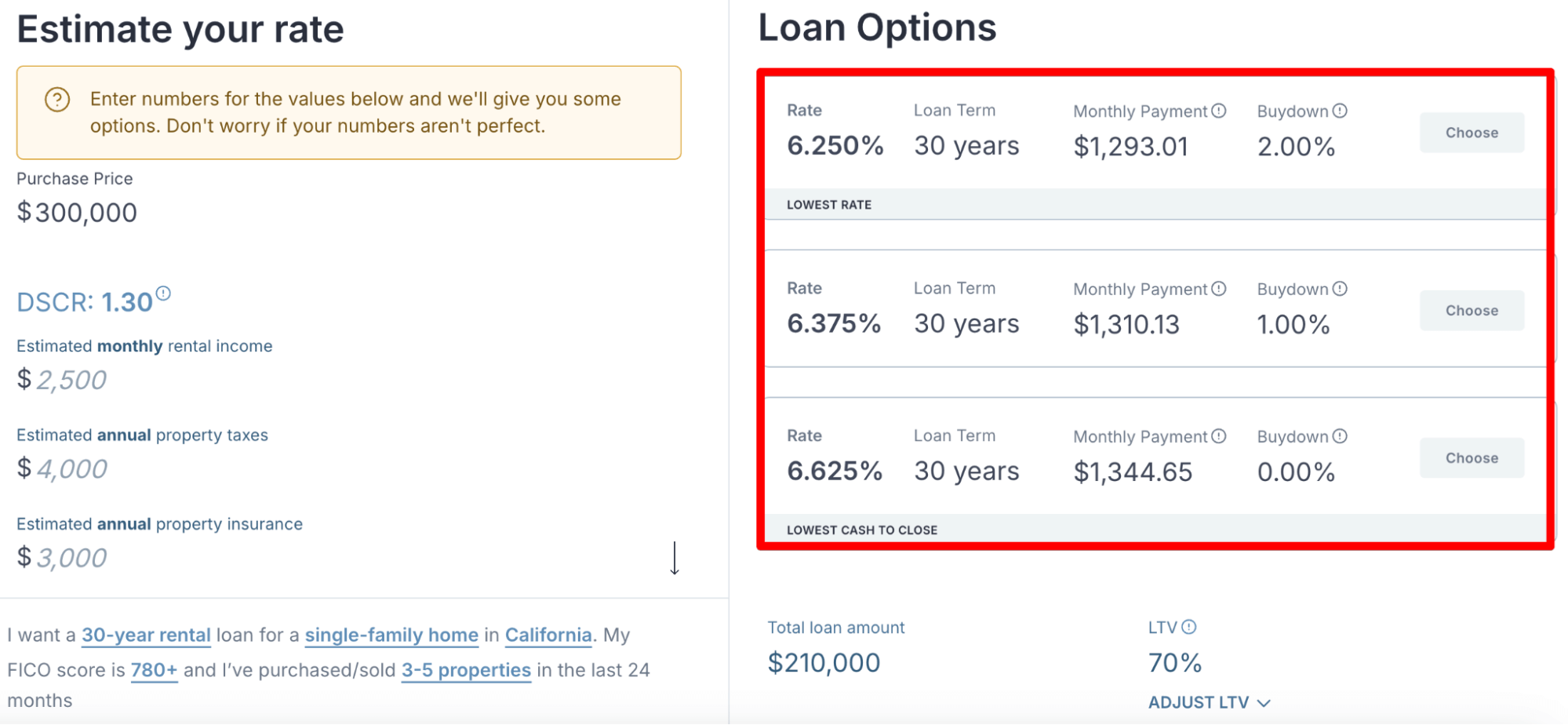

At Constitution Lending, we built a loan origination pricer to issue instant quotes, term sheets, and pre-approval letters, as well as a documents portal to accelerate processes further.

Here's how our process works:

- Enter basic information about the deal into our automated pricer, including the property’s location, type, purchase price, requested loan amount, borrower credit score, and commercial mortgage product (DSCR, fix-and-flip, bridge loan).

- Our pricer generates three instant quotes showing the interest rates, monthly payments, loan terms, and buydowns you qualify for.

- Experiment with various loan scenarios by tweaking loan amounts, property pricing, rental income projections, fixed rate or adjustable rate, and LTV ratios. This allows you to see how each factor impacts the three financing options.

- Select your preferred quote and enter your full name, email address, and phone number. We send you a term sheet, a pre-approval letter, and a copy of the quote immediately.

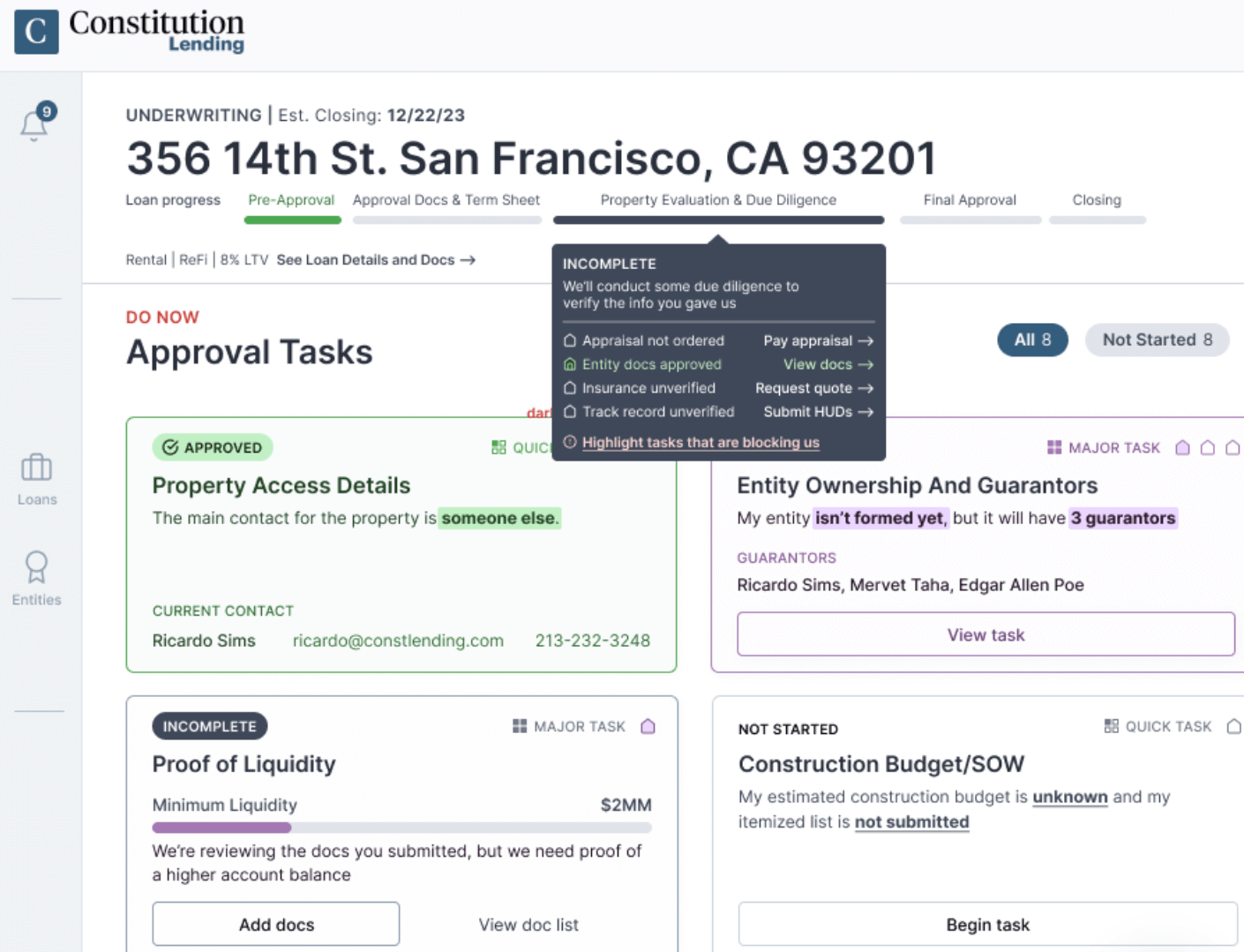

- We also send you a link to our documents portal, where you can review and submit all required documentation based on the multifamily financing you’re applying for.

- Receive definitive approval within one or two hours of submitting paperwork. We review your documents and give a clear yes-or-no answer. No last-minute rejections or surprises.

- We close in 7 to 14 days through the title company. When borrowers are under tight deadlines, and all documents are ready, we’ve funded loans in as little as four days.

Read more: Qualifying for a DSCR Multifamily Loan & How to Choose the Right Lender

Reliability: We Are a Direct Lender; We Can Guarantee a Smooth, Drama-Free Closing Early in the Application Process

Last-minute rejections usually occur when borrowers partner with brokers rather than direct lenders.

When you partner with a broker, they must send your application to an actual lender for underwriting before knowing whether you’re approved. They can’t guarantee approval upfront because they aren’t providing the funds and aren’t the decision-maker.

They may think you can qualify based on your documentation, but if the lender finds issues deep into underwriting — which is very common in large, multifamily deals — it can lead to last-minute rejections.

At Constitution Lending, you talk directly to the people funding your loan.

We’ve lent hundreds of millions of dollars of our own capital and know our requirements like the back of our hand. This familiarity allows us to determine whether you qualify immediately upon reviewing your documents and guarantee a smooth closing.

If we see discrepancies, we let you know early so you can resolve them before reapplying.

Important note: Another disadvantage of working through brokers is the additional fees and interest rate markups, making it harder to secure affordable housing loans. By applying with Constitution Lending, you secure the lowest possible interest rates that you qualify for because our loan offers don’t have expensive broker fees added on.

Types of Commercial Multifamily Loans We Offer

We provide three main categories of commercial multifamily loans:

- DSCR loans: These financing solutions are underwritten using the property’s total operating income rather than your personal earnings or debt ratios. You can learn more about the requirements to qualify for DSCR loans here.

- Fix-and-flip loans: These short-term loans are designed for the purchase and renovation of multifamily properties, typically with terms of 6 to 18 months. Approval is based on the spread between the property’s current value and its projected value after improvements.

- Bridge loans: These commercial mortgages provide interim capital for multifamily investors who need flexibility, whether that’s moving from one multifamily asset to another or securing funding quickly while arranging long-term loans.

Secure Fast, Reliable Multifamily Loans with Constitution Lending

Use our automated loan pricer to generate instant quotes, term sheets, and pre-approval letters, and secure affordable multifamily loans.

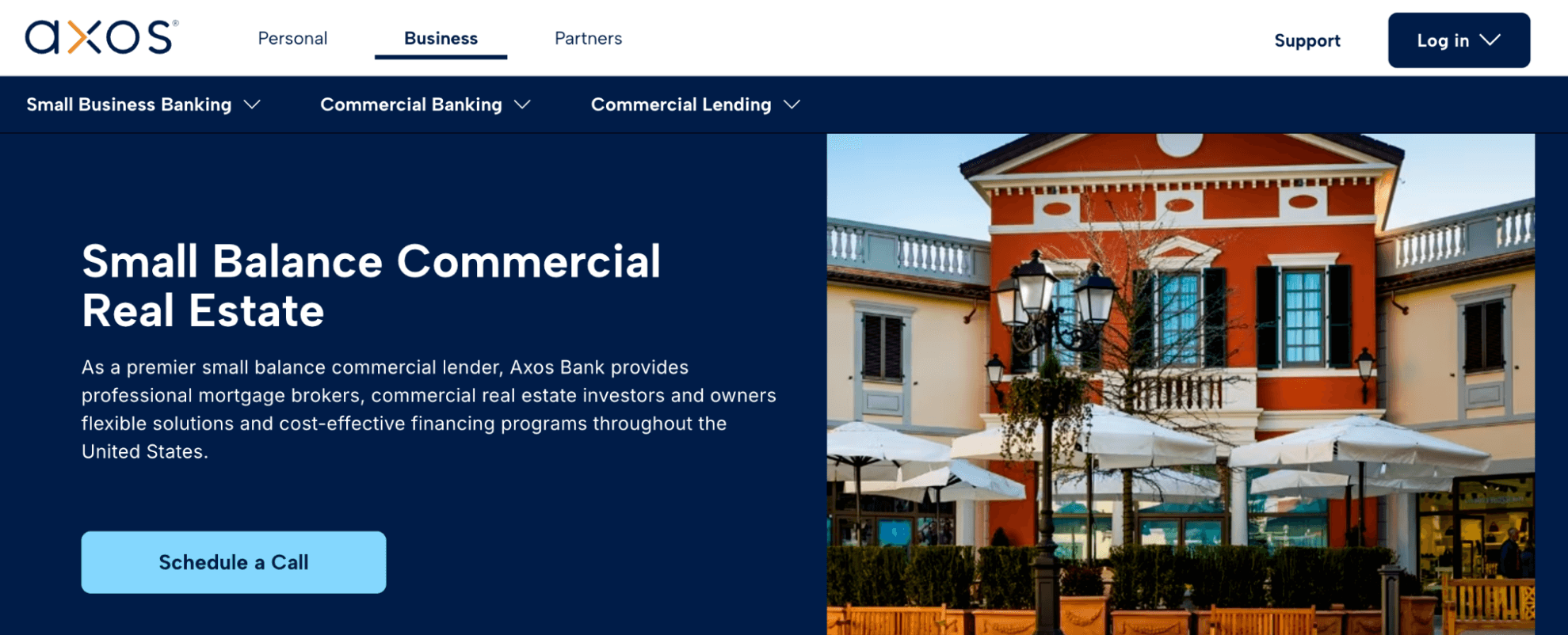

2. Axos Bank

Axos Bank provides borrowers with comprehensive financial solutions for multifamily properties, combining residential and commercial spaces into one financing package. These include Fannie Mae, Freddie Mac, FHA, and HUD multifamily loans.

Axos offers loan-to-value ratios up to 75% for multifamily properties, with loan amounts ranging from $1 million to $50 million. Their underwriting process focuses on the property's overall cash flow performance, evaluating both residential rental income and commercial lease revenue to determine DSCR.

Their multifamily lending program accepts various property types, including ground-floor retail with residential units above, office buildings with residential components, and even properties combining warehouse space with living quarters. Borrowers can qualify with credit scores as low as 680, and Axos provides both fixed-rate and adjustable-rate financing options with terms up to 30 years.

However, Axos Bank doesn't appear to offer an automated pricing system for instant quotes and term sheets. Borrowers typically need to contact a loan officer directly and wait several business days for preliminary quotes and underwriting decisions.

This traditional approach can extend the initial application timeline to 3-5 days before borrowers receive concrete loan terms, compared to lenders with automated systems that provide instant feedback.

3. LoanStream Commercial

LoanStream Commercial specializes in non-QM and alternative commercial financing. Borrowers can access flexible financial solutions for multifamily properties that may not qualify under traditional Fannie Mae and Freddie Mac guidelines. Their programs are particularly valuable for borrowers with complex income structures or properties in transitional markets.

The lender provides loan amounts from $250,000 and up with LTV ratios up to 80% for qualified multifamily properties. LoanStream's underwriting approach emphasizes property performance over borrower financials, so self-employed investors and small business owners can qualify.

LoanStream accepts properties with various commercial uses, including retail, office, light industrial, and multi-family residential combinations. They offer both short-term bridge financing (12-24 months) and long-term permanent financing (up to 25 years) for multifamily properties.

Credit score requirements are more flexible than traditional lenders, with a minimum score of 660 for qualified borrowers. The lender also provides cash-out refinancing up to 75% of the property value.

Despite these flexible terms, LoanStream relies on traditional loan officer consultation for quotes and pre-approvals. Borrowers must schedule calls with lending specialists and wait multiple days for term sheets and preliminary underwriting decisions. In our experience, these manual processes can delay initial approvals and closing.

4. Velocity Mortgage Capital

Velocity Mortgage Capital is another commercial lender that offers multifamily loan programs.

They provide financing from $1 million to $25 million with competitive interest rates starting around 7.5% for qualified borrowers. Velocity's multifamily programs accept loan-to-value ratios up to 75% for purchases and 70% for cash-out refinancing, with debt service coverage ratio requirements as low as 1.15.

Their underwriting process emphasizes property location, tenant quality, and lease terms rather than extensive borrower documentation. Velocity accepts various commercial real estate configurations, including retail/residential, office/residential, and light industrial/residential properties.

The minimum credit score required is 680, with higher scores qualifying for better rates and terms. Velocity also offers recourse and non-recourse financing solutions, giving borrowers flexibility based on their risk tolerance and loan size.

However, as with the other options mentioned above, Velocity Mortgage Capital uses traditional loan origination processes that require direct consultation with loan officers for quotes and approvals, which can hurt closing speed.

5. C2 Financial

C2 Financial provides borrowers with specialized commercial lending programs for multifamily properties. They offer loan amounts ranging from $750,000 to $20 million, with loan-to-value ratios up to 80% for well-located properties. C2's underwriting process evaluates both residential and commercial income streams, requiring a combined debt service coverage ratio of at least 1.20 to qualify.

Their multifamily programs accept various property types, including apartment buildings with ground-floor retail, office buildings with residential components, and properties combining light industrial uses with living spaces.

Credit requirements are competitive, with a minimum score of 680 for most programs. The lender offers both fixed and variable-rate options, and interest rates can range from 6.00% to 9.5% depending on property type, location, and borrower qualifications. C2 also provides construction-to-permanent financing for multifamily development projects.

It’s worth noting that C2 Financial operates through traditional relationship-based lending processes that require direct borrower-to-lender communication for quotes and approvals. Initial loan structuring typically requires phone consultations and detailed property analysis before preliminary terms are provided, often taking 4–7 business days for initial responses.

6. KeyBank

KeyBank is a well-established player among commercial multifamily lenders, known for its relationship-driven banking model and flexible loan structures. The bank offers financing for stabilized and transitional multifamily properties, with underwriting that emphasizes both property fundamentals and sponsor strength.

Online reviewers also value KeyBank’s consultative approach, particularly on larger or more nuanced deals where structuring matters. In addition to debt capital, the bank can integrate treasury services, rate hedging, and broader banking relationships, which appeals to experienced operators seeking a long-term institutional partner.

However, unlike some tech-enabled commercial multifamily lenders like Constitution Lending, KeyBank does not publicly offer an automated pricing engine or instant quote platform.

Pricing and structuring typically require direct engagement with a loan officer and internal credit review. This can slow down early-stage deal evaluation and extend closing timelines compared to lenders that provide automated term sheets or streamlined digital workflows. For borrowers prioritizing certainty and institutional execution over speed, this trade-off may be acceptable.

7. Arbor Realty Trust

Arbor Realty Trust has built a strong reputation as a specialty commercial multifamily lender, particularly for bridge loans, HUD/FHA financing, mezzanine debt, and structured capital solutions. The firm is often recognized for its ability to handle complex transactions, including value-add and transitional multifamily assets that require creative structuring.

Arbor’s deep experience in agency and government-backed programs makes it especially attractive to sponsors seeking tailored financing strategies beyond conventional bank debt. Execution reliability and product breadth are key strengths, particularly in competitive or time-sensitive acquisitions.

That said, Arbor’s process is largely relationship- and credit-driven rather than automated. The company does not publicly provide an instant automated pricer or digital self-serve quoting tools for commercial multifamily loans.

As a result, borrowers typically must go through a traditional underwriting and credit review process before receiving firm terms. While this allows for detailed structuring and risk assessment, it may lengthen the quoting phase and overall closing timeline compared to lenders that leverage automated pricing systems to accelerate preliminary approvals.

FAQs

What Are Multifamily Loans?

Multifamily loans are financing products designed specifically for properties containing multiple residential units, typically ranging from duplexes to large apartment complexes. These loans are underwritten based on the property's income-generating potential rather than the borrower's personal financial profile.

Unlike single-family residential mortgages, multifamily loans consider factors such as net operating income, debt service coverage ratios, and occupancy rates when determining loan eligibility and terms.

What Factors Should I Consider When Choosing a Commercial Multifamily Lender?

When selecting a multifamily lender, prioritize closing speed and reliability. Look for lenders who can provide instant quotes and term sheets rather than making you wait days for basic loan information. Additionally, verify that you're working with a direct lender who funds loans with their own capital, as brokers often cause last-minute rejections during the underwriting process.

Who Is the Best Commercial Real Estate Lender?

Constitution Lending stands out as a top commercial multifamily lender due to our ability to close loans within 7 to 14 days and provide instant quotes through our automated loan pricer. As a direct lender, we eliminate the risk of last-minute rejections that commonly occur with brokers.

We offer DSCR loans for 2-4 unit and 5-8 unit multifamily properties with loan amounts from $125,000 to $3,000,000, a minimum credit score of 660, and loan-to-value ratios up to 80% for purchases.

What Are Rental Appraisals?

Rental appraisals determine a property's market value based on its income-generating potential and comparable sales data. For multifamily properties, appraisers analyze rental income from all units, operating expenses, vacancy rates, and recent sales of similar properties in the area.

These appraisals are crucial for DSCR loans because they establish both the property's value for loan-to-value calculations and verify the rental income figures used in debt service coverage ratio calculations.