Apartment complexes have the potential to generate higher returns than single-family homes due to economies of scale (such as shared maintenance costs and bulk purchasing) and unique tax advantages.

However, apartment complexes are extremely difficult to finance because few lenders have the capital to fund them. Those who can, such as large banks and credit unions, have rigorous requirements, including a net worth greater than the loan amount, cash reserves equal to 12 months of expenses, and several years of commercial real estate investing experience.

To help you secure apartment complex loans, we’ve put together this guide outlining the key steps — based on our 10+ years of experience as both real estate investors and private lenders:

- Choose the right loan option based on your investment strategy:

- DSCR Loans

- Commercial fix-and-flip loans

- Traditional consumer mortgages

- Prepare your loan package.

- Approach the right lenders and submit your loan package.

- Evaluate a lender’s closing speed.

- Consider whether they are a direct lender or a broker.

- Await the lender’s underwriting, due diligence, and appraisal.

- Close the deal.

Who we are: Constitution Lending is a direct lender offering apartment complex financing options that are easier to qualify for than traditional bank loans. Use our automated pricer to map different loan scenarios and see what rates, terms, and amounts you qualify for.

Step 1: Choose the Right Loan Option Based on Your Investment Strategy

Real estate investors have three main options for financing an apartment complex, depending on their investment strategy:

- DSCR loans

- Commercial fix-and-flip loans

- Traditional debt financing

DSCR Loans: Best Suited for Stabilized Properties

DSCR (debt-service coverage ratio) loans are non-recourse financing options with 30-year amortization, evaluated based on an apartment complex’s ability to cover its debt obligations through rental income.

For instance, say a 20-unit apartment complex generates $40,000 per month in rent and has $30,000 in expenses. That building would have a DSCR of 1.33 ($40,000 ÷ $30,000 = 1.33). This number is what lenders evaluate when deciding whether to approve your application. Most lenders have a DSCR requirement of 1.0, but we’ve funded buildings with a DSCR as low as 0.75.

DSCR loans offer two main advantages for commercial real estate investors:

- DSCR loans are easier to qualify for: Unlike banks, DSCR lenders don’t care about your finances (e.g., income level, debt-to-income ratio, net worth, employment history, real estate experience). This makes them a good choice for real estate investors who cannot qualify for apartment loans from large banks.

- DSCR loans can close faster: Because DSCR lenders don’t underwrite your personal financial profile, you can close much faster. You don’t have to prepare and submit tax returns, pay stubs, net worth statements, business invoices, or any of the other financial statements banks require.

DSCR loan interest rates are between 6.25% to 8.50%, depending on the property’s cash flow potential. Fixed-rate and interest-only terms are available. This article explains in more detail the factors that influence your interest rates.

Read more: DSCR Loan Requirements: 5 Key Factors Lenders Consider

Commercial Fix-and-Flip Loans: Best for Value-Add Properties

DSCR loans are available only for ready-to-rent apartment complexes (i.e., Class A and B buildings), not Class C and D buildings that require upgrades and renovations.

For buildings in need of renovation, short-term fix-and-flip loans are typically the best option. That’s because, like DSCR loans, lenders don't care about your personal finances. Instead, they evaluate the property itself — specifically, its total cost (including purchase price and renovation costs) relative to its estimated after-repair value.

The larger the difference between the total costs and after-repair value, the better your chances of qualifying and the lower your required down payment. A bigger spread between costs and after-repair value indicates a safer, more profitable investment.

You can learn more about typical fix-and-flip loan requirements here.

Most fix-and-flip apartment loans have terms of 6 to 18 months, depending on the extent of the renovations, after which point the apartment properties must be sold and the loan balance paid off. Their interest rates are higher than longer-term DSCR loans, starting at 10.99%.

For investors looking to purchase an apartment complex, renovate it, and then collect rental income long-term, we can offer a fix-and-flip loan upfront and refinance it later with a DSCR loan when it matures. This way, you get your fix-and-flip and DSCR loan from the same source, reducing your administrative burden.

Traditional Multifamily Financing (Freddie Mac and Fannie Mae): Best for Investors Who Meet Their Stringent Criteria

While it is possible to secure financing for an apartment complex through traditional lenders like banks, the process is extremely difficult and time-consuming.

Most banks require borrowers to have a net worth that exceeds the total loan amount, cash reserves equal to 9 to 12 months of debt service payments, and years of commercial real estate investing experience.

The timeline for traditional bank financing is also long, typically taking 60 to 90 days to close apartment loans, compared to the 7 to 14 days that specialized lenders like Constitution Lending can achieve.

That said, bank loans, along with CMBS, HUD/FHA, and life insurance company programs, typically offer lower interest rates than DSCR loans. As a result, they remain strong options for high-net-worth, experienced investors who can accommodate a 60 to 90-day closing timeline.

Step 2: Prepare Your Loan Package

Before you spend time approaching lenders, we recommend pre-qualifying the commercial property first and confirming whether the deal actually meets the requirements mentioned above.

For DSCR loans, we advise requesting the rent roll documents from the seller, which detail the property's total rental income. Then, you can plug the rental income figure into our automated loan pricer, along with your desired loan amount, to get a DSCR estimate.

If the multifamily property meets the 0.75 to 1.0 DSCR required to qualify, begin gathering the necessary documents to apply. These may vary from lender to lender, but with Constitution Lending, we only require:

- Rent rolls showing total income, occupancy rates, and vacancy rates over the past 12 months

- Proof of insurance starting on the closing date

- Bank statements showing you have the required down payment

- Entity documents

- Pro forma showing projected net operating income after the value-add (mainly for fix-and-flip)

- Detailed business plan (mainly for fix-and-flip)

For investors looking to fix-and-flip an apartment complex, we recommend identifying the renovations that will have the biggest impact on the after-repair value and working with a contractor to create a rough construction budget.

Then order an appraisal of the commercial property that takes into account those renovations to determine the after-repair value. Plug these three numbers (purchase price, construction budget, and estimated after-repair value) into our automated pricer to see if you meet our requirements and what rates and loan terms are available.

Step 3: Approach the Right Lenders and Submit Your Loan Package

Once you’ve prepared your loan package, you need to find and approach lenders that can finance apartment complexes.

Choosing the right lender is critical to the success of your apartment complex purchase. It often determines whether you secure low interest rates and a fast close, or endure a slow process full of delays, complications, and the risk of losing your earnest money deposit.

Here’s how to tell if a lender is going to be slow, unreliable, and expensive.

- How fast do they issue quotes, term sheets, and pre-approval letters?

- Are they a direct lender or broker?

How Fast Can They Issue Quotes, Term Sheets, and Pre-approval Letters?

The biggest problem you’ll likely face when sourcing real estate financing is slow lenders.

Many lenders overpromise about closing speed to secure borrower clients. They’ll say they can close within a week, but then end up taking months. This can put your earnest money deposit at risk and allow faster-moving investors to snap up undervalued multifamily properties.

Our advice is not to take a lender’s word on their closing speed. A more reliable way to gauge closing speed is how quickly they provide quotes, term sheets, and approval letters. Lenders who are slow at this likely have outdated and inefficient internal processes, which will hurt closing times.

We recommend going with a lender that can issue instant quotes, term sheets, and approval letters, as they can close the fastest.

For example, at Constitution Lending, we’ve developed automated tools, such as our loan pricer and documents portal, to speed up the application, approval, and closing process — enabling our clients to compete with the speed of cash buyers. In fact, we regularly close apartment loans, including those for 5- to 20-unit apartment complexes, in 7 to 14 days.

Here’s how our process works:

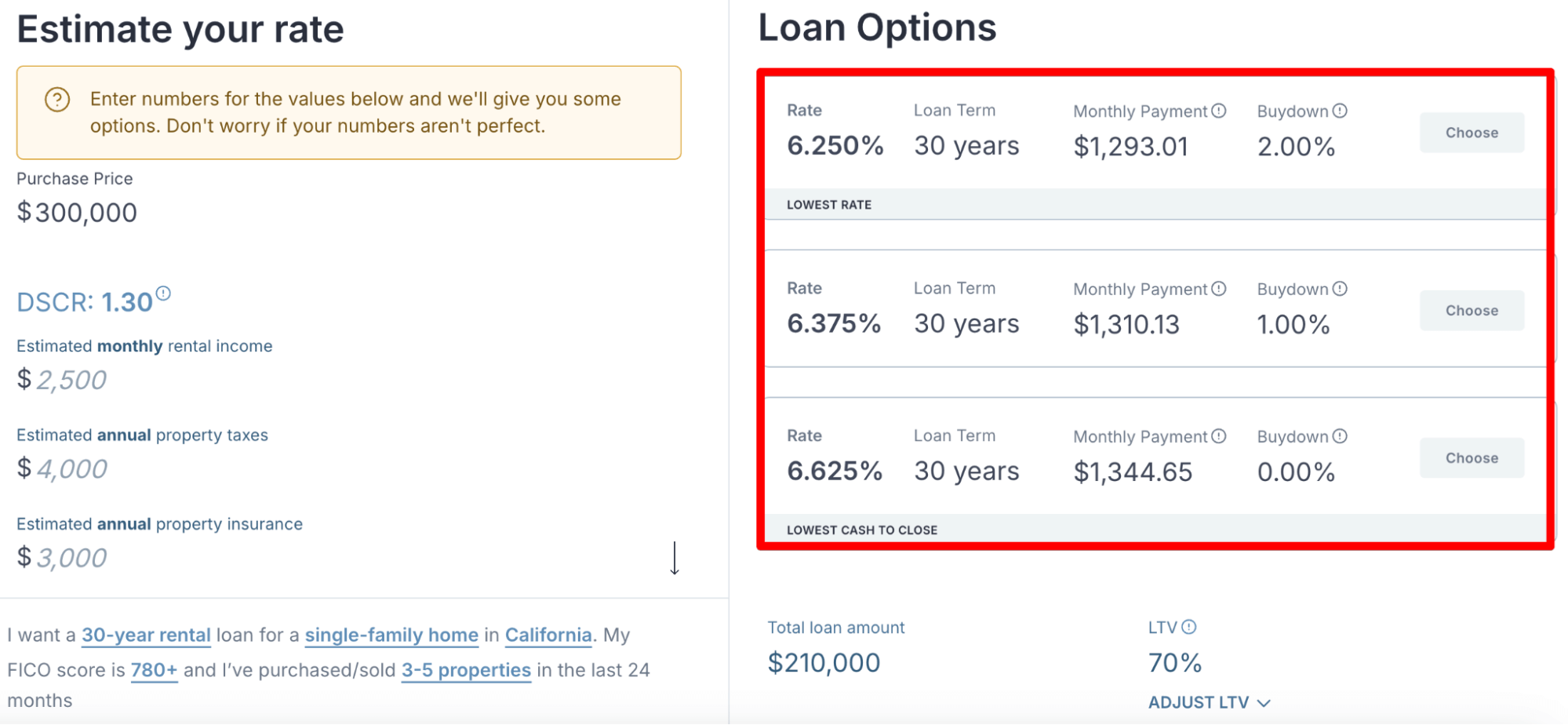

- Generate an instant quote, term sheet, and approval letter by answering a few questions in our loan pricer. This includes the property’s asking price, estimated rental income, your desired loan amount, and your credit score.

- The automated pricer calculates whether you qualify and, if you do, generates three quotes outlining your interest rates, terms, and buydown options.

- You can use the interface on the left to adjust rental income figures, loan amounts, expenses, and purchase prices to see how they affect your three quotes. For fix-and-flip apartment loans, these variables are as-is values, construction budgets, and after-repair values.

- Select the quote that fits you best and enter your full name and email address. You’ll be able to download a copy of the quote, a term sheet, and a pre-approval letter.

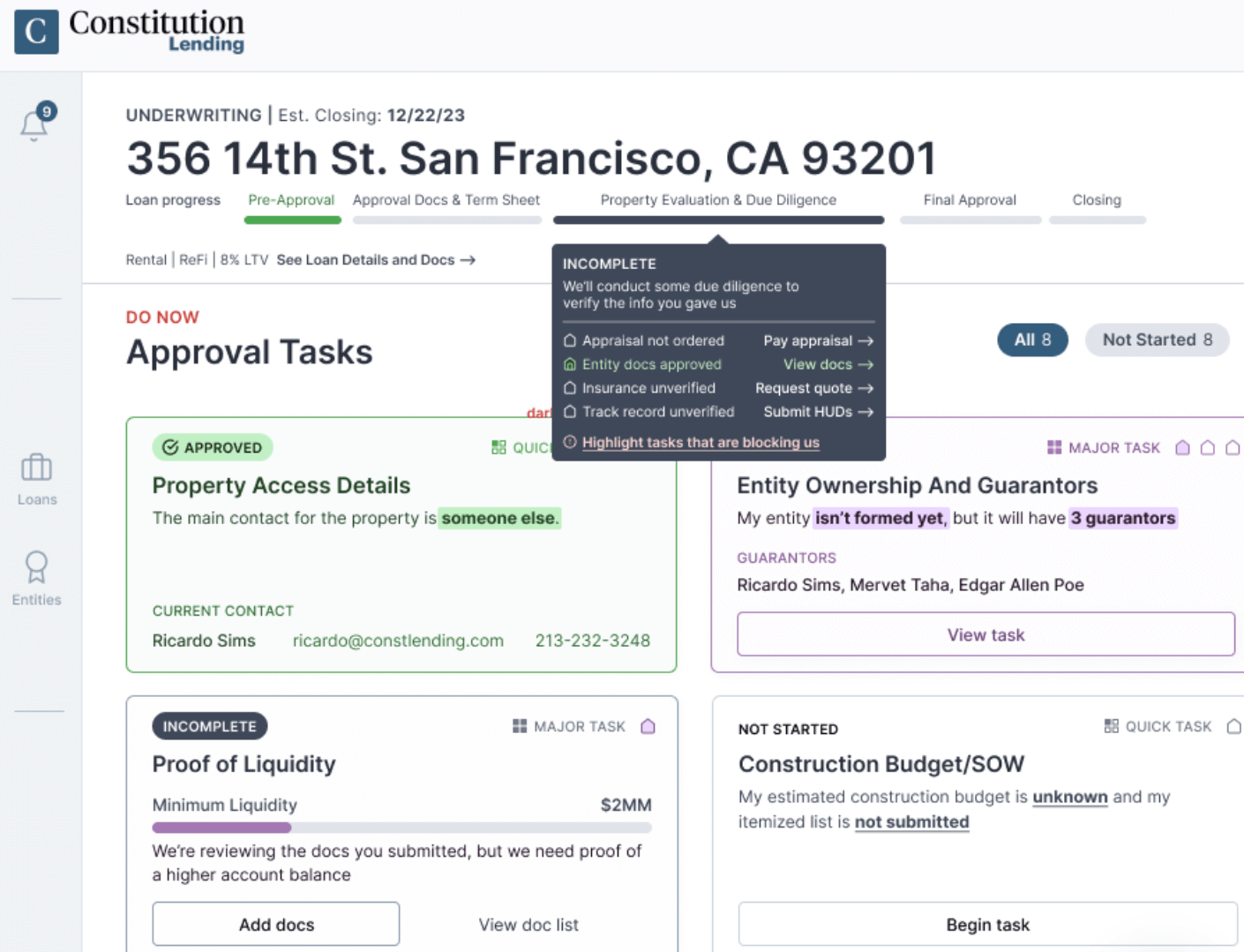

- At the same time, we’ll email you access to our documents portal, where you can view all the paperwork you need to submit depending on the type of loan. You can also chat directly with a loan officer on our team through the portal to clarify any information or answer any questions.

- As soon as you submit your documents, we review them, send you an email letting you know whether you qualify, and close within 7 to 14 days.

Are They a Direct Lender?

Unreliable, flaky lenders are another major challenge you’ll likely run into.

We regularly hear from our borrower clients about how they submitted their loan package to a lender, the lender said they met all the requirements and could qualify, but then rejected their loan application right before closing. We’ve even heard of borrowers getting rejected and losing their earnest money deposits on the closing date.

Last-minute rejections tend to happen when borrowers work with loan brokers rather than going directly to the source of the funds.

The problem with brokers is that they must still find a lender who can fund apartment complexes, submit your loan package to them, and wait for the lender to evaluate and underwrite your loan application before giving you a concrete yes or no.

A broker may believe you qualify, but nothing is certain until the deal goes through underwriting. If the lender finds issues with your application, the deal, or the property late into underwriting, you may get rejected after already being told you can qualify.

When you partner with a direct lender like Constitution Lending, you get a reliable and transparent answer immediately after you submit all your paperwork. No last-minute complications.

That’s possible because we’ve funded countless apartment complex loans and thus, know our requirements extremely well. We immediately know whether you qualify and don’t have to send your application to another lender for underwriting.

Note: Another drawback of brokers is that they charge additional fees, leading to higher APRs. Going to a direct lender lets you avoid broker fees and secure lower APRs.

Step 4: Await the Lender’s Underwriting, Due Diligence, and Appraisal

Once you’ve submitted your application, the lender will underwrite your application. This includes reviewing rent rolls and trailing 12 months financials, analyzing the deal’s cash flow and DSCR, and evaluating the property’s condition and market.

Lenders will also order an appraisal of the apartment building to determine its value and, for fix-and-flip projects, its estimated after-repair value. This helps accurately assess the property's value and protects you from hidden liabilities.

Step 5: Close the Deal

If the apartment complex passes all required assessments, the lender schedules the closing. At closing, the final loan documents are signed, funds are wired, prorations are settled, the seller signs the deed over, and ownership officially transfers to you.

Secure Fast and Affordable Apartment Complex Financing With Constitution Lending

Use our automated loan pricer to play around with various loan scenarios and see what rates and terms you qualify for.

Frequently Asked Questions

What Are the Requirements to Get a Loan for an Apartment Complex?

Apartment financing typically requires a minimum down payment of 25% to 30%, though Constitution Lending can accept as little as 20%. Borrowers also need a good credit score, usually 660 or higher.

Lenders evaluate the building’s DSCR, which should be at least 0.75, meaning rental income covers 75% of expenses.

Net worth requirements often equal the loan amount, and borrowers must show sufficient liquidity to cover several months of debt service. These requirements vary significantly between agency loans, HUD loans, and other commercial mortgage products.

What Are the Steps to Secure a Loan for Purchasing an Apartment Complex?

The multifamily loan process begins with pre-qualification, where lenders review the property's DSCR and your creditworthiness.

Next, you'll submit a formal application with detailed financial documentation, including rent rolls and operating statements. The lender orders an appraisal and completes environmental and property condition assessments.

The entire process typically takes 45 to 90 days, depending on the loan type and complexity. At Constitution Lending, however, we can close in as little as 7 to 14 days due to our automated tools and processes.

How Hard Is It to Get a Loan to Build an Apartment Complex?

Construction loans for multifamily housing are significantly more complex than acquisition financing. Lenders require detailed construction plans, contractor qualifications, and project budgets before approval.

Most construction-to-permanent loans require 25% to 30% down payments and involve higher risk for lenders. Borrowers need previous development experience, strong cash reserves, and pre-leasing commitments to demonstrate project viability.

How Much Money Is Needed to Buy an Apartment Complex?

Down payment requirements range from 20% to 30% of the purchase price, meaning a $2 million property requires $400,000 to $600,000 upfront. Additional costs include closing costs (2% to 3%), due diligence expenses, and working capital reserves.

How Much Do Apartment Buildings Cost To Build?

Construction costs vary significantly by location, with national averages ranging from $150 to $400 per square foot. A 50-unit apartment building typically costs $5 million to $15 million to construct, excluding land acquisition costs.

What Are the Advantages of Buying an Apartment Complex?

Apartment investing offers superior cash flow compared to single-family rental properties because it generates multiple income streams from individual units. This diversification reduces vacancy risk since one vacant unit doesn't eliminate all rental income.

Commercial real estate loans for multifamily properties often provide better financing terms, including longer amortization periods and competitive interest rates. Properties with over 20 units may qualify for non-recourse loans, limiting your personal liability.

How Long Will It Take to Close a Fannie Mae Loan?

Fannie Mae multifamily loans typically require 60 to 90 days to close, depending on property complexity and borrower readiness. The timeline includes application processing, underwriting, appraisal, and document preparation phases.