Mixed-use properties can be extremely profitable for real estate investors because they leverage economies of scale to reduce costs and generate stronger cash flow than single-unit properties.

That said, mixed-use properties are challenging to finance. Most banks and credit unions avoid them because they’re difficult to underwrite, appraise, and properly zone. Smaller alternative lenders, like DSCR lenders, also cannot finance them because they don’t have enough capital for larger loan sizes.

To fill this market gap, Constitution Lending began offering larger DSCR loan programs for real estate investors looking to purchase mixed-use properties.

This article covers everything you need to know about our mixed-use DSCR loans, including how they work, their benefits, requirements, how to apply, and interest rates to expect.

At the end, we discuss how Constitution Lending can close faster and offer lower interest rates than most lenders.

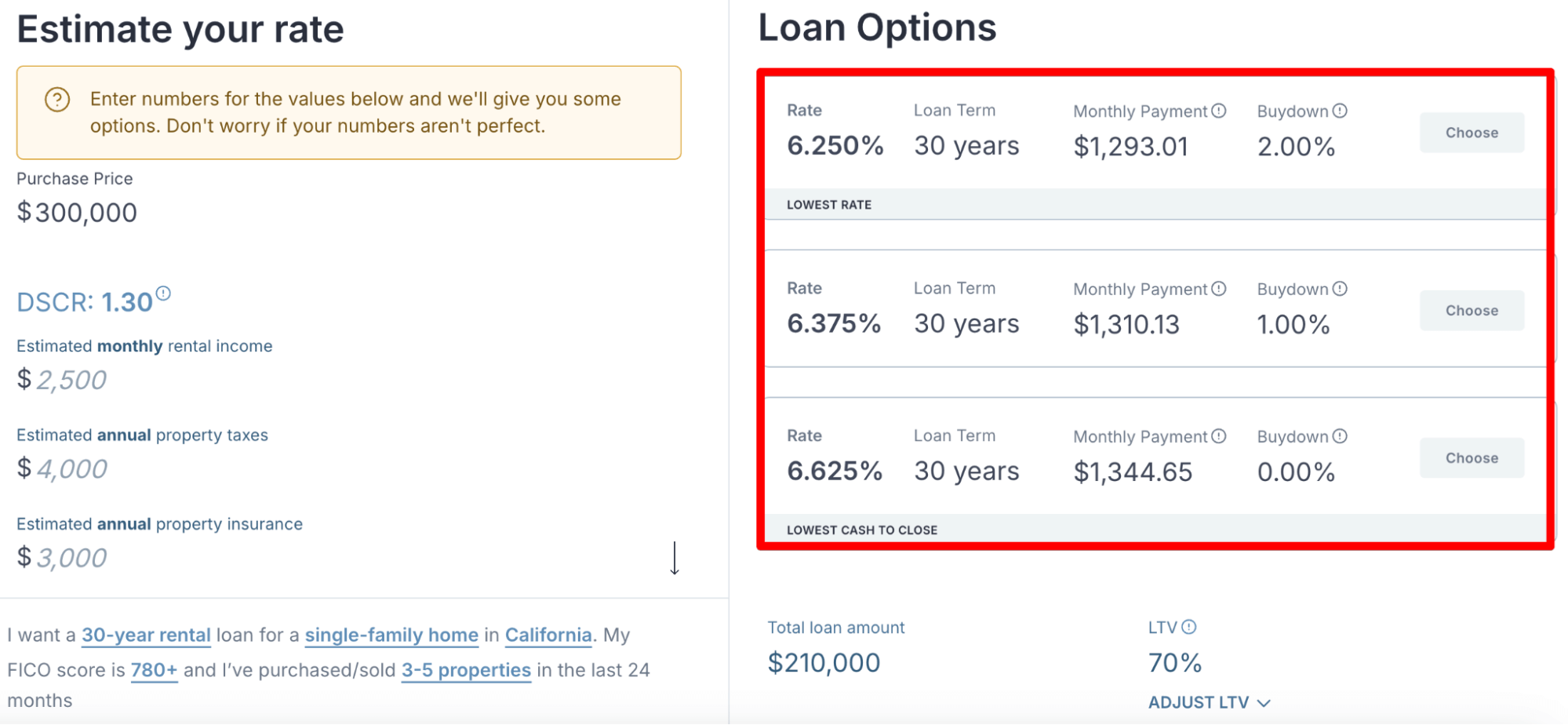

You can use our automated DSCR loan pricer to generate instant quotes and see what terms you qualify for on your mixed-use property investment.

How Do DSCR Loans Work and What Are Their Advantages?

As the name suggests, DSCR (debt-service coverage ratio) loans are financing options assessed based on a property's DSCR, that is, its net operating income divided by its expenses. DSCR loans don’t consider personal financial documentation like traditional mortgage loans.

For example, if a mixed-use property earns $50,000 per month in rental income from all residential and commercial units, and its total expenses (including loan payments, insurance, taxes, and maintenance) equal $40,000, its DSCR would be 1.25 ($50,000 ÷ $40,000). This ratio is what lenders focus on.

DSCR loans offer several advantages for mixed-use real estate investors:

- No personal income verification: DSCR lenders don't consider your personal income, DTI ratio, employment history, or tax returns. They focus solely on the property's ability to generate cash flow. This makes it possible for real estate investors with complex finances (e.g., self-employed, no W-2 income, high DTI, large tax deductions) to qualify.

- Faster closing: You don't have to submit all the personal income paperwork banks require, speeding up the application and approval process. DSCR loans typically close within 30 days, while traditional mortgage loans take 45 to 90 days. Constitution Lending can close within 7 to 14 days, even faster than most DSCR lenders, due to our automated processes (more on this below).

- Unlimited portfolio growth: There's no limit on the number of DSCR loans you can have simultaneously, unlike Fannie Mae and Freddie Mac guidelines that restrict conventional mortgages. As long as each property meets the minimum DSCR requirement and you have an adequate down payment, you can continue expanding your portfolio.

- First-time investors are welcome: Many DSCR lenders, including Constitution Lending, don't require previous real estate investment experience, making mixed-use properties accessible to new investors.

Read more: DSCR Loan Pros and Cons: A Detailed Guide for Investors

DSCR Loan Requirements for Mixed-Use Properties

To secure a DSCR loan for a mixed-use property, you must meet three main requirements:

- Minimum DSCR: 0.75

- Down payment: 20% to 25% of the property’s value

- Credit score: 660+

Minimum DSCR of 0.75

The ideal DSCR for any investment property is 1.0 or higher, because it demonstrates that the property’s income covers all its debt obligations.

However, Constitution Lending accepts mixed-use properties with a DSCR as low as 0.75, meaning the rental income only needs to cover 75% of the property's total expenses. This low DSCR requirement allows real estate investors to acquire properties with strong long-term potential that may not immediately achieve full cash flow coverage.

70% to 80% Loan-to-Value (LTV)

DSCR lenders offer LTV ratios between 70% and 80% for mixed-use properties. This means if you're purchasing a building for $10 million, for example, lenders will provide between $7 million and $8 million, requiring you to contribute the remaining amount as a down payment.

For cash-out refinancing of existing mixed-use properties, lenders generally offer LTVs of 65% to 75%, with the remaining 25% to 35% equity serving as collateral.

The exact LTV you qualify for depends on several factors, including DSCR, your FICO score, the stability of existing leases, and the property's condition and location. For instance, mixed-use properties in prime locations with established commercial tenants often qualify for higher LTV ratios.

660+ Credit Score

While DSCR lenders primarily evaluate properties based on cash flow, borrower creditworthiness remains important. Lenders need assurance that borrowers have demonstrated financial responsibility in the past by paying loans on time.

As a result, most DSCR lenders ask for a minimum credit score of 720 or higher.

However, Constitution Lending offers more flexibility with mixed-use properties, accepting borrowers with FICO scores as low as 660. Our goal with this lower threshold is to make mixed-use investing accessible to more real estate investors, even those with suboptimal credit.

Read more: DSCR Loan Requirements: 5 Key Factors Lenders Consider

How to Apply for a Mixed-Use DSCR Loan

- Pre-qualify yourself: Before you approach a lender, run some quick numbers to see if the property meets the minimum DSCR. You can do this by asking the seller for the building’s rent rolls, totaling the rental income, and plugging that number into our DSCR loan pricer with the loan amount you’ll need.

- Gather and submit documents: If the property meets the DSCR minimum, prepare and submit the following documents to the lender: 3 months of bank statements showing you have a 20% to 30% down payment, proof of insurance starting on the closing date, purchase contract, entity or LLC documents, rent rolls, and a copy of your ID or driver’s license.

- Wait for lender underwriting and appraisal: The lender will underwrite the building’s DSCR, conduct an appraisal to confirm its value, and close the loan, at which point the seller signs the deed over.

DSCR Loan Interest Rates for Mixed-Use Properties

Interest rates on DSCR loans currently range between 6.25% and 8.50%. This applies to 30-year fixed-rate, hybrid 5/6 ARMs, and interest-only loan programs.

This article explains the factors that influence the interest rates you qualify for in more detail.

How to Choose a Lender for Your Mixed-Use DSCR Loan

The biggest mistake investors make when financing mixed-use properties is choosing the wrong DSCR lender.

Many DSCR lenders are slow and unreliable, saying they can close within a couple of weeks, but then taking months. Bad lenders are the most common reason why we see borrowers lose their earnest money deposits and watch undervalued properties get snapped up by faster buyers.

Here’s our advice on identifying and avoiding slow, low-quality DSCR lenders:

- Look at how quickly they can issue quotes, term sheets, and approval letters.

- Verify whether they are a direct lender or broker.

How Quickly Can They Issue Quotes, Term Sheets, and Approval Letters?

Almost every lender will advertise that they can close quickly, but it’s rare for them to live up to their promises. We've heard from borrowers that lenders promised to close in one or two weeks, only to see deals drag out for 60+ days, costing them their earnest money deposits.

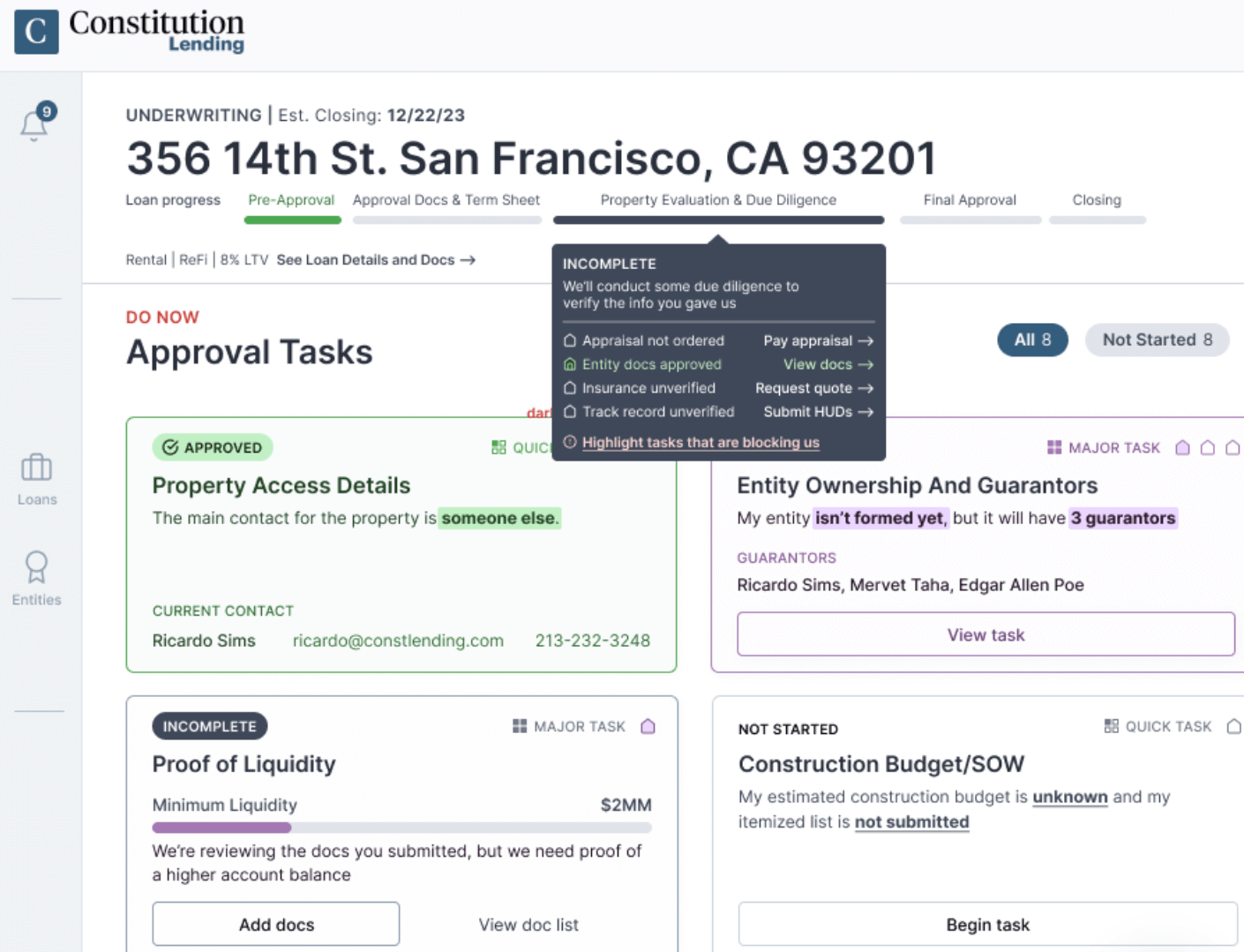

We don’t suggest taking a lender's word on their closing speed. Instead, evaluate how quickly they can issue loan quotes, term sheets, and approval letters. If a lender takes multiple business days to provide these, you can expect slow closing times because it signals that their internal workflows aren’t designed for speed.

At Constitution Lending, we can close faster than most lenders thanks to our automated loan pricer and streamlined documents portal.

Enter basic property information into our loan pricer, and we provide quotes, term sheets, and pre-approval letters immediately. You can also test different scenarios by adjusting loan amounts and rental income projections, to see what difference they make to your quotes. No need to wait days for loan officers to call and spend hours on phone calls explaining the deal.

You’ll then receive email access to our documents portal, where you can view all the documents we require and submit them immediately.

This efficiency allows us to close most loans within 7 to 14 days, and we've closed urgent deals in as little as 4 days when all documentation is ready.

Partner with a Direct Lender

Last-minute rejections are a big problem in mixed-use property financing. It’s common for investors to get approved early in the process only to be rejected right before closing.

Last-minute complications typically happen when you partner with brokers rather than direct lenders. Brokers aren't the decision-makers because they aren't lending you their own money. They are simply connecting you to a lender.

This means a broker may review your mixed-use property application and believe you qualify, but they must submit your application to the actual lender for final underwriting. If the lender discovers issues late in the process — which is common with complex, mixed-use properties with mixed tenant types and zoning compliance — it can result in last-minute rejections.

Constitution Lending is a direct lender, which means we fund your mixed-use property loan with our own capital. We can evaluate your loan application, identify any potential issues upfront, and guarantee a smooth closing process once we approve your loan. We don’t have to wait for third-party approval.

Being a direct lender also means lower costs for borrowers, as there are no broker fees built into your loan terms. You're working directly with the decision-makers throughout the entire process.

Secure Affordable Mixed-Use DSCR Loans With Constitution Lending

Mixed-use properties offer real estate investors the opportunity to diversify income streams and achieve higher returns than traditional residential investments. DSCR loans make these properties accessible by focusing on cash flow rather than personal financial documentation, enabling faster closings and more flexible qualification criteria.

Use our automated DSCR loan pricer to generate instant quotes for your mixed-use property investment and receive a term sheet within 24 hours. Our direct lending approach ensures you get definitive answers about your eligibility without the risk of last-minute surprises.

Frequently Asked Questions

What Is the Minimum DSCR Ratio to Qualify for Constitution Lending’s Mixed-Use Loans?

Constitution Lending requires a minimum DSCR of 0.75. This means the building's total income needs to offset at least 75% of its total expenses.

The DSCR calculation for mixed-use properties includes rental income from both residential units and commercial spaces, divided by all property expenses, including mortgage payments, taxes, insurance, and maintenance costs.

What Is the Maximum Amount of Units for a Mixed-Use Property to Qualify?

Our mixed-use DSCR loans are available for properties with up to 20 total units.

The residential portion can include single-family or multi-family units, while the commercial space might house retail, office, or service businesses.

What Is the Minimum Credit Score I Need to Qualify for a Mixed-Use DSCR Loan?

With Constitution Lending, borrowers need a minimum credit score of 660 for mixed-use DSCR loans.

On the other hand, most DSCR lenders will require at least a 720 credit score.

What Is the Maximum Cash-Out Proceeds for a Mixed-Use DSCR Loan?

A cash-out refinance on mixed-use properties is limited to 75% of the property's appraised value. To qualify, borrowers must demonstrate stable income from both residential and commercial components over the previous 12-24 months.

What Are the Interest Rates for DSCR Loans?

Interest rates for mixed-use DSCR loans range from 6.25% to 8.50%.

Rates vary based on credit score, DSCR ratio, loan-to-value ratio, and the specific mix of residential versus commercial space. Properties with established commercial tenants on long-term leases may qualify for lower rates.

What Is the Minimum Down Payment for a Mixed-Use DSCR Loan?

Mixed-use DSCR loans require a minimum 20% down payment.

This down payment requirement reflects the increased risk and complexity of mixed-use properties, as it provides a larger cushion against potential vacancy, market downturns, or major repairs.

How Mixed-Use DSCR Loans Differ from Traditional Commercial Loans

Mixed-use DSCR loans offer several advantages over traditional commercial financing for mixed-use properties.

Traditional commercial loans typically require extensive financial documentation, business plans, and personal guarantees. They also often have shorter terms (5-10 years) with balloon payments, creating refinancing risk.

Mixed-use DSCR loans focus primarily on property cash flow rather than borrower financials, similar to residential DSCR loans. This makes them accessible to investors who may not qualify for traditional commercial financing due to debt-to-income ratios or self-employment status.

The 30-year fixed-rate structure provides stability that commercial loans rarely offer, eliminating the need to refinance every few years.