Slow and unreliable lenders are the most common reason we see brokers lose borrower clients.

Many commercial lenders claim they can close within a week or two, only for the process to drag out for months. It’s also common for lenders to reject applications at the last minute, even after giving the green light early on. This puts you in uncomfortable situations with your borrowers and damages their trust in you.

To avoid slow, low-quality commercial lenders, evaluate the following factors before you decide to partner with one:

- How fast can they close? We don’t recommend taking a lender at their word when it comes to closing speed. Instead, look at how quickly they can issue quotes, term sheets, and pre-approval letters, as that reflects the efficiency of their internal processes. If this takes multiple days, it’s unlikely you’ll close quickly. The fastest lenders can issue instant quotes, term sheets, and pre-approval letters.

- Are they the ones funding the loan? Confirm you’re working with the people funding the loan. Deals commonly fall through at the last minute due to miscommunication when brokers unknowingly work with other brokers rather than going directly to the source of the funds. We recommend partnering with a direct lender, as it gives you a direct line to the decision-maker.

In an effort to help brokers avoid bad lenders, we wrote this guide evaluating five commercial lenders against the points outlined above.

We start with ourselves, Constitution Lending, and how we use automated tools to help brokers provide their borrowers with reliable and flexible financing solutions in just 7 to 14 days.

Use our automated loan pricer to generate instant quotes, term sheets, and underwriter-reviewed pre-approval letters for your borrowers.

1. Constitution Lending: A Commercial Lender That Helps Brokers Close in 7 to 14 Days

Constitution Lending is a commercial real estate lender focused on helping brokers close loans fast and with certainty.

We founded Constitution Lending after being real estate investors for several years and realizing that fast and reliable commercial lenders are extremely rare. We had to endure lender after lender who overpromised but were slow and flaky.

We’ve had lenders promise they could close in under two weeks, only to take months. Some lenders even rejected our application on the day of closing without explanation after they’d already told us we qualified.

We know that long waiting times and last-minute rejections can be awkward for commercial loan brokers and cause borrowers to lose confidence in you, so we designed our loan process to avoid these situations.

Hear what borrowers and commercial loan brokers say about our closing speed and reliability:

Let’s dig deeper into our loan process below.

Factor #1: We Can Close within 7 to 14 Days Thanks to Our Automated Pricer and Documents Portal

When you apply with most lenders, you’ll need to wait several business days for a quote, term sheet, and pre-approval letter. That’s due to their slow and bureaucratic nature. It’s not uncommon for your application to sit untouched for days before a loan officer even looks at it.

These unnecessary delays often carry over into underwriting and closing, resulting in 30+ day closing times.

Constitution Lending speeds up the application process with our automated loan pricer and documents portal:

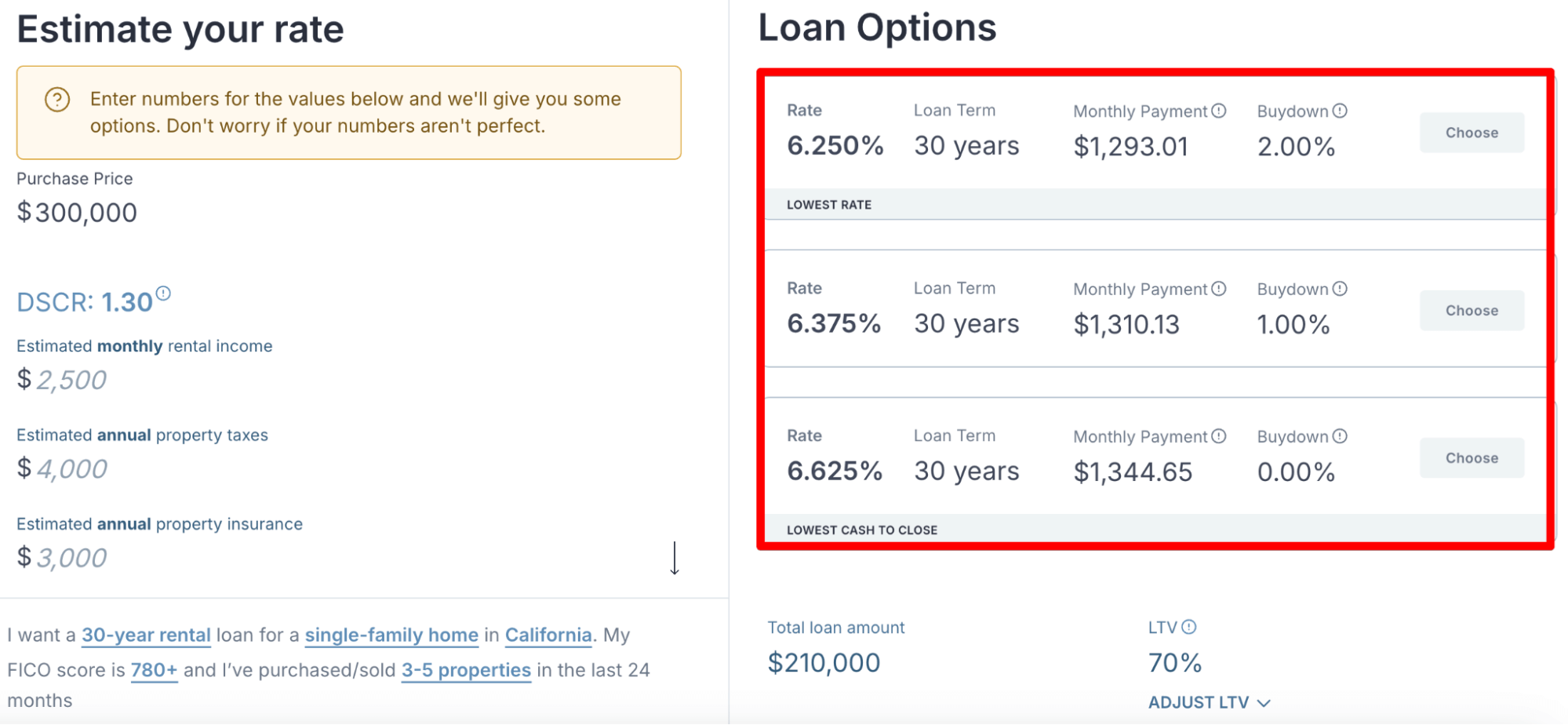

- You can generate instant quotes for your borrowers by entering the following details into our automated pricer: property location, type, purchase price, requested loan amount, borrower credit score and real estate experience, whether it’s a purchase or refinance, and type of loan product (e.g., DSCR, fix-and-flip, construction).

- You’ll receive three quotes detailing the interest rates, monthly payments, terms, and buydowns your borrower qualifies for.

- You can apply different loan amounts, rental incomes, and LTVs to see how each variable affects the three loan quotes.

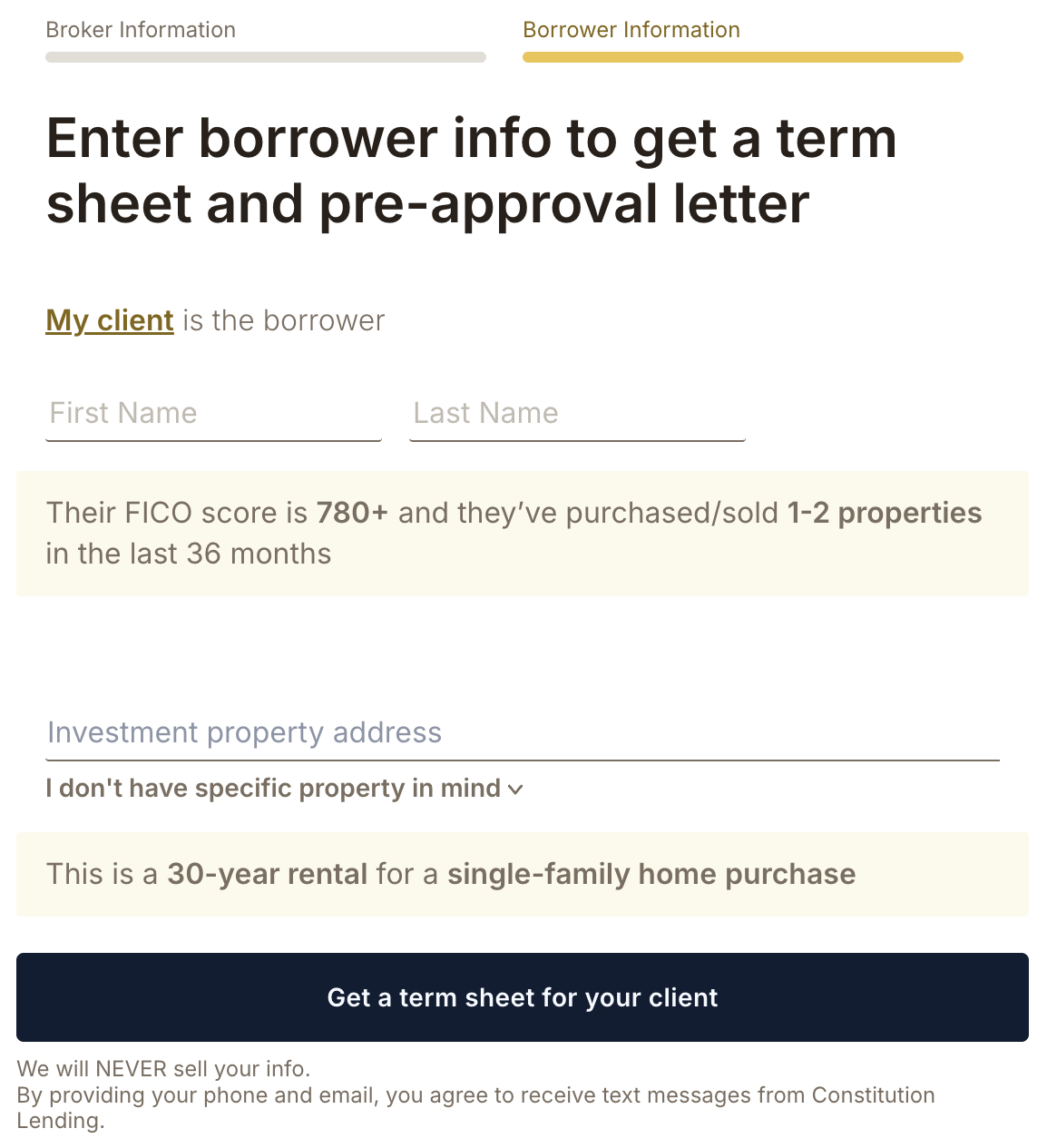

- Click on a quote that suits your borrower best, enter your full name, email address, and your borrower’s information, and you’ll be able to download a term sheet and pre-approval letter.

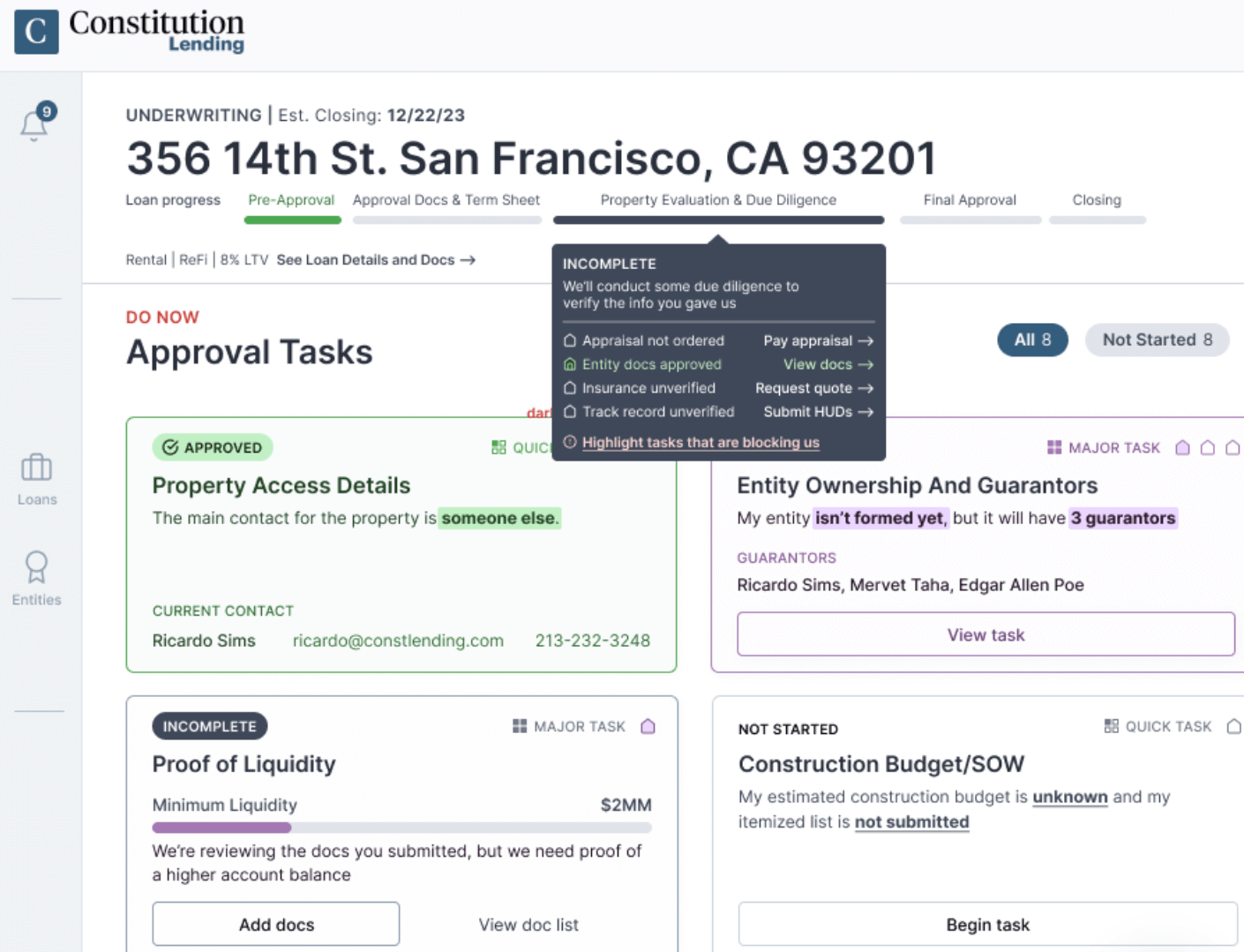

- At the same time, you’ll receive access to our documents portal, where you can see and submit all the required paperwork depending on the loan you’re applying for.

- As soon as you submit the documents, we review them. Within a few hours, we will let you know whether your borrower qualifies.

- We close the loan with the title company in 1 to 2 weeks. We can close faster than this if you're really under the gun; we’ve funded loans in just 4 days.

Factor #2: We are a Direct Lender, So We Can Guarantee a Smooth Closing Early in the Application Process

Another issue commercial mortgage brokers commonly face is their applications getting rejected right before closing. This hurts a borrower’s trust and confidence in you.

Last-minute rejections occur when brokers mistakenly partner with other brokers for financing rather than going to a direct lender. You wouldn’t think so, but this is far more common than most people realize. We’ve heard of deals with up to 3 mortgage brokers.

Here’s how partnering with another mortgage broker causes last-minute rejections: brokers must submit your application to an actual lender for underwriting before saying if you qualify. They can’t give you an upfront yes-or-no because they aren’t funding the loan and therefore aren’t the decision maker on your application.

The broker may think you qualify by reviewing your paperwork, but they can never be 100% sure until the lender completes underwriting. If the lender discovers problems late in underwriting, it opens the door to last-minute rejections.

When you partner with a direct lender like Constitution Lending, you’re talking to the source of the funds and the decision maker on your loan.

The advantage of this is that we can review your paperwork and immediately say whether you qualify and guarantee a smooth closing. We know our loan criteria and what it takes to qualify since we’ve originated hundreds of loans. We don’t have to submit your application to another lender and wait for them to underwrite before giving you a yes or no.

Read more: 5 Best Hard Money Lenders in Connecticut (Reviews)

Types of Commercial Loan Programs We Offer

We offer four main types of commercial real estate loans:

- 30-year DSCR loans: These loans are evaluated based on a commercial property’s cash flow and not the borrower’s income, debt-to-income ratio, or employment history. This makes them a good option for commercial real estate investors with non-W-2 income, high debt-to-income ratios, or other conditions that prevent them from qualifying for conventional bank or credit union loans. You can learn more about DSCR loans here.

- Fix-and-flip loans: These are short-term commercial lending options (6 to 12 months) used to purchase and rehab an investment property. They are approved on the property’s as-is value versus its after-repair value, and not the borrower's financials. We also offer fix-and-flip loans that can be converted into long-term DSCR loans.

- Construction loans: These are short-term loans used by construction companies and real estate developers to construct rental properties from the ground up. They are approved based on the cost to construct a property relative to its after-construction market value.

- Bridge loans: As the name suggests, these are commercial real estate financing options designed to help real estate investors bridge the gap between selling an investment property and buying a new one.

Secure Fast and Reliable Commercial Real Estate Lending Solutions for Your Borrowers with Constitution Lending

Enter a few details about your borrowers into our automated pricer and generate instant quotes, term sheets, and pre-approval letters.

2. Avana Capital

Avana Capital is a commercial real estate lender that provides financing solutions for various property types, including single-family homes, multifamily homes, mixed-use properties, self-storage facilities, and mobile home parks.

They focus on serving business owners and real estate investors who need flexible financing options beyond traditional bank products.

Avana Capital offers multiple loan products, including bridge loans, permanent financing, and lines of credit with competitive interest rates. Avana Capital works with properties ranging from small business locations to larger commercial developments, providing creative solutions for complex deals that traditional lenders might reject.

However, Avana Capital operates with a traditional application process that requires brokers to submit contact forms and wait for loan officers to respond. Unlike Constitution Lending’s automated systems, you'll need to speak directly with their team to receive quotes and term sheets, which can add days to your initial qualification process. Their underwriting timeline typically extends beyond two weeks, making it challenging to compete with cash buyers or meet tight closing deadlines.

For CRE deals requiring longer processing times, Avana Capital can be a viable option. They offer various amortization schedules and work with borrowers who have unique financing needs. However, brokers working with time-sensitive borrowers may find their processes slower than Constitution Lending’s automated pricing tools and document submission systems.

3. Finance Lobby

Finance Lobby positions itself as a commercial lending platform connecting brokers with multiple funding sources for diverse needs, including healthcare facilities, retail spaces, industrial properties, and residential real estate.

The platform offers access to various loan products, including interest-only options, traditional amortization schedules, and lines of credit. Finance Lobby claims to work with deals ranging from small business acquisitions to larger commercial real estate transactions, providing brokers access to multiple lenders through their network.

Their brokerage model means they don't fund loans directly, instead connecting your borrower applications to their network of originators and lenders. This creates potential complications during underwriting, as Finance Lobby cannot guarantee loan approval until their partner lenders complete their own review process. Last-minute rejections become more likely when multiple parties are involved in the decision-making process.

The application process requires brokers to submit detailed borrower information through their platform, then wait for their team to match deals with appropriate lenders. This can extend qualification timelines significantly compared to working directly with lenders who can provide immediate answers about eligibility.

While Finance Lobby may offer access to specialized products like SBA loans, their broker model introduces uncertainty that can be problematic.

4. Velocity Mortgage Capital

Velocity Mortgage Capital is a direct lender specializing in commercial real estate financing across various property types, including office buildings, retail centers, and industrial facilities.

They offer competitive interest rates and flexible loan terms, including interest-only payment options and various amortization schedules. Velocity focuses on deals ranging from smaller commercial properties to larger multi-million dollar transactions, providing financing for purchases, refinancing, and cash-out scenarios.

While Velocity operates as a direct lender, their application process follows traditional lending practices, requiring brokers to complete detailed application forms and wait for a loan officer to contact them. They don't offer automated pricing tools or generate instant quotes, meaning initial qualification can take several days as loan officers review applications and prepare term sheets manually.

Their underwriting process typically requires 3–4 weeks, which may not meet the needs of brokers working with borrowers facing competitive bidding situations.

5. Pacific Premier Bank

Pacific Premier Bank (now part of Columbia Bank) is an FDIC-insured financial institution offering commercial real estate lending services to loan brokers.

They offer competitive rates on commercial real estate loans with traditional amortization schedules and established lending criteria. Pacific Premier works with borrowers seeking financing for owner-occupied commercial properties, investment real estate, and business expansion projects. Their loan products include both fixed-rate and adjustable-rate options with terms typically ranging from 5 to 25 years.

However, Pacific Premier operates with traditional banking processes that can significantly delay qualification and closing timelines. As a regulated bank, they maintain strict documentation requirements and lengthy underwriting procedures that often take 45–60 days to complete.

In addition, they don’t offer automated pricing tools or instant qualification systems, requiring brokers to work through relationship managers and loan officers for all quote requests and application updates. This traditional approach can create challenges for brokers working with borrowers who need quick answers about qualification.

Secure Low-interest Commercial Real Estate Loans for Your Borrowers with Constitution Lending

Use our automated loan pricer to model multiple loan scenarios and deliver instant quotes, term sheets, and pre-approval letters for your borrowers.