Hard money wholesale lenders provide capital to brokers at discounted rates, who then originate loans to individual borrowers. This makes wholesale lending an excellent way for brokers to close more deals and earn points without lending their own capital.

That said, the wholesale lender you work with matters because it impacts how quickly and smoothly your deals close. One of the main reasons we see brokers losing borrowers is because of slow and unreliable wholesale lenders.

Many lower-quality wholesale lenders promise one- to two-week closings, but after you relay that timeline to your borrowers, it becomes clear they overpromised and need 30+ days.

Even worse, lenders sometimes reject applications right before closing and after initially saying your borrower qualifies, leaving you scrambling to find alternative financing and creating awkward conversations with borrowers.

To avoid slow and unreliable hard money wholesale lenders, we recommend evaluating these factors before partnering with one:

- How fast can they issue quotes, term sheets, and pre-approval letters? If this takes multiple days, it signals inefficient internal processes that will likely delay closing. The fastest wholesale lenders can provide instant quotes, term sheets, and pre-approval letters, demonstrating they have the systems to move applications forward quickly.

- Are they a direct lender? Many wholesale "lenders" are actually brokers who must find funding elsewhere. As we explain in more detail below, partnering with another broker often leads to miscommunication, surprises, and last-minute rejections. Choosing a direct lender gives you clear communication with the financier and decision-maker on the loan.

In this article, we compare 10 hard money wholesale lenders using these two criteria, helping you differentiate between high-quality and problematic lenders.

We start by reviewing our wholesale financing program and how we help brokers consistently close in 7 to 14 days, without the drama of last-minute surprises or rejections.

Use our automated loan pricer to generate instant quotes, term sheets, and underwriter-reviewed pre-approval letters for your borrowers.

1. Constitution Lending: Fast, Reliable Hard Money Wholesale Financing

Constitution Lending is a direct hard money wholesale lender designed to help mortgage brokers close deals fast and with complete certainty.

We founded Constitution Lending after spending years as real estate investors and experiencing for ourselves how slow and unreliable most hard money lenders are.

Many hard money lenders promised they could close within two weeks, only to take months. Some rejected our applications on the day of closing without explanation, even after confirming we qualified weeks earlier.

We know these delays and last-minute rejections can make you look unprofessional and put you in a tough spot with borrowers. So, we designed our private lending process to eliminate them.

Here's what clients say about our closing speed and reliability:

Let’s take a closer look at how Constitution Lending meets the two criteria above.

Our Automated Pricer and Documents Portal Enable 7 to 14 Day Closings

Most wholesale lenders require mortgage brokers to wait several business days just to get a basic quote, term sheet, and pre-approval letter. This delay often reflects deeper inefficiencies that carry over into underwriting and closing, resulting in 30+ day funding timelines.

Constitution Lending accelerates the entire loan process with our automated pricer and documents portal:

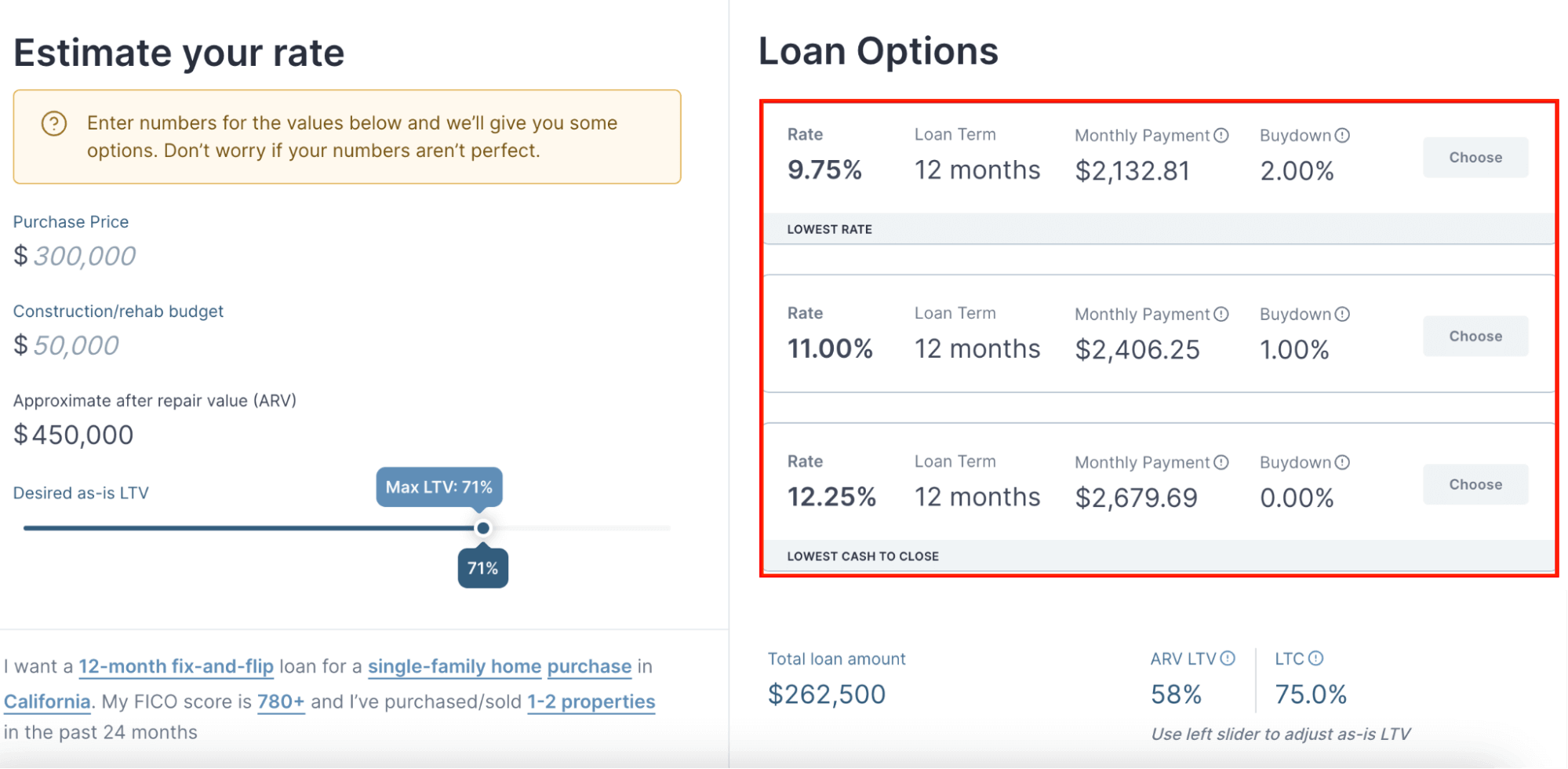

- Enter a few details into our automated pricer: the value of the property, its location, requested loan amount, borrower credit score and years of experience, and loan type (fix-and-flip loan, rental loan, construction loan, or bridge loan).

- Receive three quotes that show interest rates, monthly payments, loan terms, and the available buydowns your borrower qualifies for.

- Test different scenarios by adjusting loan amounts, construction budgets, after-repair values, and LTVs to see how each variable affects the three quotes.

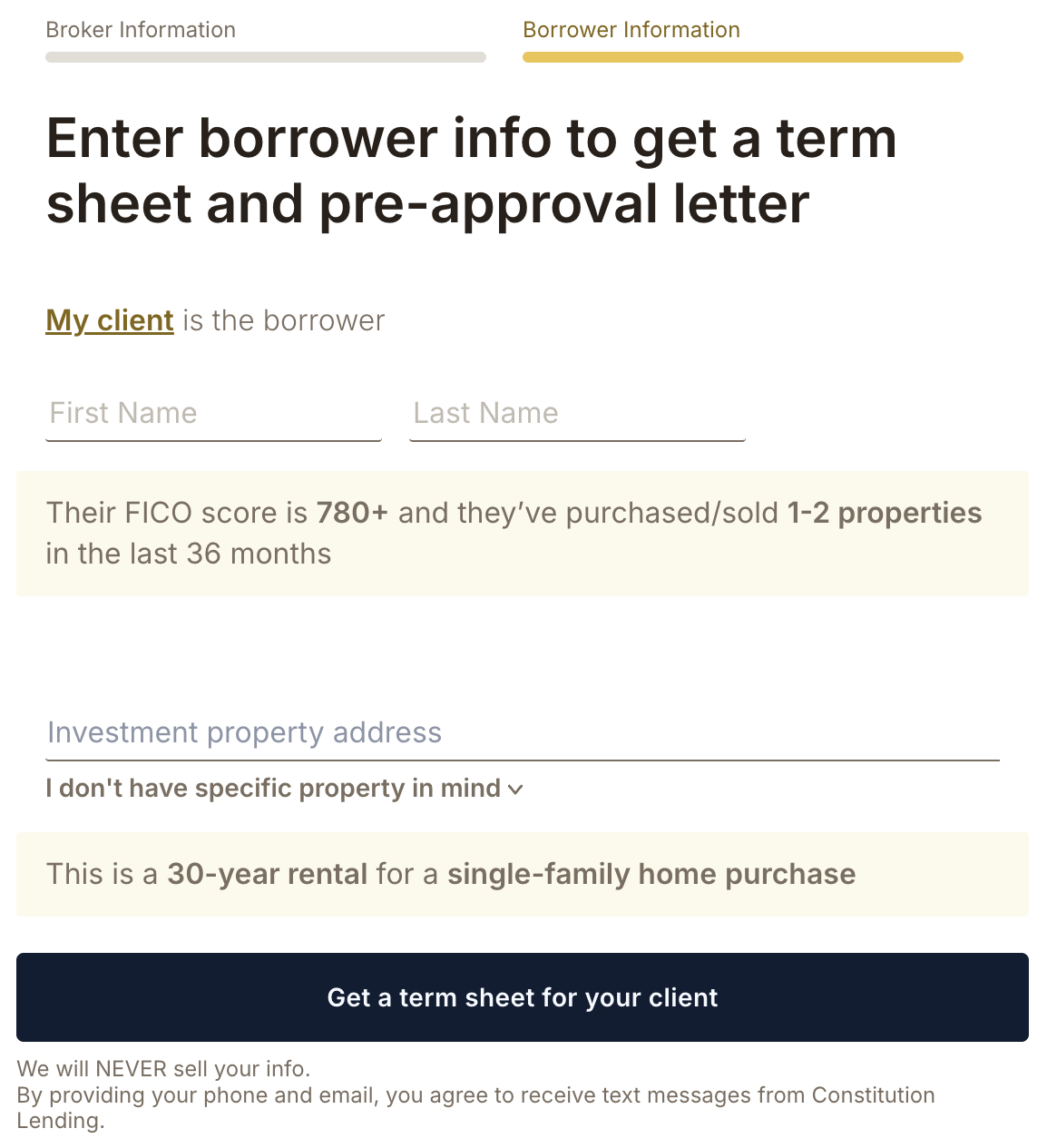

- Download immediate documentation by clicking on your preferred quote and entering your contact information. You'll instantly receive a term sheet, pre-approval letter, and a copy of the quote to share with your borrower.

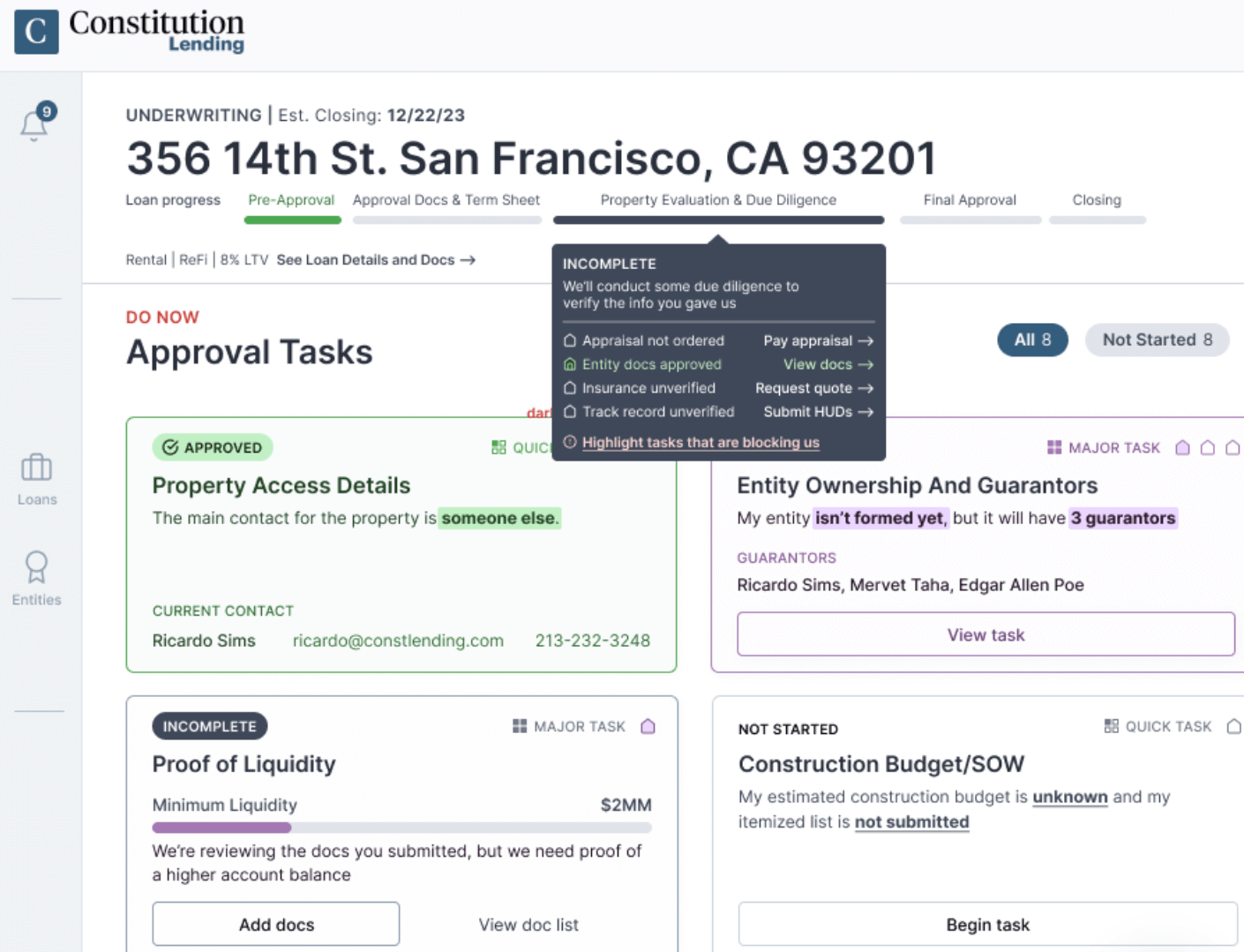

- Access our documents portal at the same time, where you can view and submit all required paperwork based on the type of loan you’re applying for.

- Get definitive approval within hours of submitting documents. A loan officer on our team reviews everything immediately and provides a concrete yes-or-no answer. No last-minute surprises.

- We close within 7 to 14 days with the title company. When brokers are under extreme time pressure and have all documents ready, we've funded loans in just 4 days.

We Are Direct Wholesale Lenders with In-house Capital

The leading cause of last-minute rejections in wholesale lending is brokers unknowingly partnering with other brokers rather than direct private lenders. This is more common than most people realize, as we've seen deals involving up to three different brokers.

Here's how working through other brokers causes problems: brokers must submit your borrower’s loan application to the actual funding source for underwriting. As a result, they can't provide definitive approval early on because they don't control the money or make the final decisions.

Even if they think your borrower qualifies, they won't know for certain until the real lender completes underwriting.

If issues surface late in underwriting, they can lead to last-minute rejections and complications, despite the broker saying early on that your borrower could qualify.

When you partner with Constitution Lending, you're working directly with the decision-makers on your loan. We’ve originated hundreds of millions in loans with in-house funds, understand our hard money lending criteria inside and out, and therefore, can guarantee closing immediately after you submit documents. We don't need to consult with third parties or wait for external approval.

Read more: 5 Best Hard Money Lenders for First-Time Investors

Types of Hard Money Financing Options We Offer

We provide four main categories of wholesale financing:

- 30-year DSCR loans: Evaluated based on investment property cash flow, not borrower income or debt-to-income ratios. They are perfect for real estate investors who want to purchase or refinance a rental property with non-W2 income, high DTI ratios, or other factors that traditional banks avoid. This article explains the pros and cons of DSCR loans in more detail.

- Fix-and-flip loans: Short-term financing (6–12 months) for fix-and-flip projects. They are approved based on a real estate investment’s as-is value versus after-repair value, not borrower financials. We also offer loan programs that convert fix-and-flip loans to long-term DSCR loans.

- Ground-up construction loans: Short-term funding for building rental properties from scratch. New construction loans are approved based on construction costs relative to the value of the completed property.

- Bridge loans: Temporary financing to help investors transition between selling one property and purchasing another.

Secure reliable wholesale hard money loans by using our automated loan pricer to generate instant quotes and documentation for your borrowers.

2. Deephaven Mortgage

Deephaven Mortgage operates as a wholesale hard money lender serving brokers nationwide with a focus on non-QM and investment property financing. Their wholesale division provides DSCR loans, bank statement programs, and asset-based lending options for real estate investors who may not qualify with traditional lenders.

The company offers competitive loan programs with flexible underwriting guidelines, accepting borrowers with credit scores as low as 680 for most programs. They provide loan amounts ranging from $100,000 to $5 million across various property types, including single-family residential (SFR) properties and small multifamily properties.

However, Deephaven lacks the automated pricing tools that enable instant quotes and same-day documentation. Brokers typically need to work through account executives to obtain pricing and preliminary approvals, which can extend the initial application timeline compared to lenders with automated systems. This manual process means you'll need to spend time on the phone explaining deal details and waiting for responses, rather than getting immediate answers for your borrowers.

Their underwriting process generally takes 2-3 weeks once complete documentation is submitted, assuming no complications arise during review. For brokers working with borrowers who need faster closings to compete with cash offers, this timeline may not meet their investment strategy requirements.

3. Angel Oak Mortgage Solutions

Angel Oak Mortgage Solutions provides wholesale non-QM lending programs, including DSCR loans, bank statement loans, and asset-based financing. They serve brokers across most U.S. states with a variety of investment property loan products designed for investors with non-traditional income documentation.

Their DSCR program accepts properties with debt service coverage ratios as low as 0.75 and offers loan amounts up to $3 million. They provide both fixed-rate and adjustable-rate options with terms up to 30 years, giving borrowers flexibility in their refinancing and investment goals.

Angel Oak requires a minimum credit score of 680 for most programs and offers maximum LTVs of 80% for purchases and 75% for refinances. They accept various property types, including single-family homes, condos, and 2-4 unit multifamily properties. The higher credit score requirement compared to some lenders may limit your pool of potential borrowers, particularly first-time investors with shorter credit history.

The approval process involves working with dedicated account managers who handle pricing requests and preliminary underwriting. While they aim for competitive turnaround times, the manual nature of their initial quote process can add several days compared to automated systems. For brokers who need to provide upfront pricing to borrowers quickly, this delay could impact your ability to secure deals in competitive markets.

4. Lima One Capital

Lima One Capital operates a wholesale division that provides hard money lending products to mortgage brokers and correspondents. They offer DSCR loans, fix-and-flip financing, and bridge loans for investment properties, making them a versatile option for brokers serving different types of real estate investors.

Their wholesale program includes loan amounts from $75,000 to $3 million with flexible terms ranging from short-term fix-and-flip loans to 30-year rental property financing. They accept borrowers with credit scores starting at 680 and provide LTVs up to 80% for purchases, though the higher credit requirement may exclude some potential borrowers compared to lenders with more flexible standards.

Lima One has established relationships with brokers nationwide and provides dedicated wholesale account management. However, their quote generation process requires broker interaction with account representatives rather than offering automated pricing tools. This means you'll need to wait for manual responses instead of getting instant quotes for your borrowers, which can slow down your ability to move quickly on deals.

Processing times typically range from 2–4 weeks, depending on loan complexity and documentation completeness. They focus primarily on experienced real estate investors rather than first-time buyers, which may limit your referral opportunities with newer investors entering the market.

5. New Silver Lending

New Silver Lending offers wholesale hard money programs through their broker channel, focusing on real estate investment financing, including DSCR loans and fix-and-flip products. Their platform is designed to serve mortgage brokers working with investment property borrowers who need non-traditional lending solutions.

They provide loan amounts ranging from $150,000 to $3 million with interest rates starting around 7.5% for qualified borrowers. Their programs accept minimum credit scores of 660 and offer competitive LTV ratios up to 80% for purchases. The lower credit score requirement makes them more accessible than some competitors, though they may charge higher interest rates for borrowers with lower credit history.

New Silver's wholesale process involves working through regional account managers who handle pricing and preliminary approvals. This manual approach means brokers can't generate instant quotes for borrowers, potentially causing delays when speed is critical for competitive deals.

They aim for closing timeframes of 15–21 days once all documentation is submitted and underwriting begins. Their product suite covers single-family homes, condos, and 2–4 unit properties across most U.S. markets. They require borrowers to have some real estate investment experience for most loan programs, which may exclude first-time investors from your potential client base.

6. Kiavi

Kiavi operates a wholesale lending channel that provides investment property financing to mortgage brokers nationwide. Their primary focus is on rental property DSCR loans and portfolio refinancing products, making them a specialized option for brokers working with buy-and-hold investors.

The company offers 30-year fixed-rate and adjustable-rate DSCR loans with competitive pricing for qualified borrowers. They accept credit scores as low as 680 and provide loan amounts up to $3 million for single-family and small multifamily properties. However, their higher credit score requirements compared to some lenders may limit your ability to work with borrowers who have a shorter credit history or past financial challenges.

Kiavi's wholesale process requires brokers to work through dedicated account representatives for pricing and approvals. They don't currently offer automated pricing tools, which can extend the initial quote timeline compared to lenders with self-service options. This manual approach means you'll need to wait for responses rather than providing immediate answers to borrowers' questions about loan terms and qualification.

Their underwriting timeline typically ranges from 2-3 weeks for standard deals, with potential for faster processing on straightforward applications with complete documentation. For brokers working with borrowers who need to close quickly to secure properties, this timeline may not be competitive with faster alternatives.

7. RCN Capital

RCN Capital provides wholesale hard money lending through their broker network, offering DSCR loans and short-term rental financing products. They serve brokers across most U.S. states with flexible investment property programs designed for various types of real estate investment strategies.

Their wholesale division offers loan amounts from $55,000 to $2 million with competitive interest rates for qualified borrowers. They require a minimum credit score of 660 and accept properties with DSCR ratios as low as 1.05. However, their higher DSCR requirements compared to some lenders mean properties need stronger cash flow to qualify, potentially limiting deals where borrowers are willing to supplement monthly payments with other income.

RCN Capital's process involves working with wholesale account managers for pricing and preliminary approvals. The manual nature of their quote system can add time to the initial application phase compared to automated alternatives. This delay can be problematic when working with borrowers who need quick responses to make competitive offers.

Standard processing times range from 15–30 days, depending on loan complexity and market conditions. They focus primarily on experienced investors and require properties to be rent-ready at closing, which may exclude fix-and-flip investors or those purchasing properties that need renovation before generating rental income.

8. Griffin Funding

Griffin Funding operates wholesale programs serving mortgage brokers with non-QM and investment property financing. They offer DSCR loans, bank statement programs, and commercial lending products, providing brokers with a range of options for different borrower profiles.

Their wholesale division provides loan amounts ranging from $100,000 to $20 million with flexible underwriting guidelines. They accept borrowers with credit scores as low as 620 and accept various property types, including single-family homes and small commercial properties. The lower credit score requirement makes them accessible for borrowers with a challenged credit history, though this may come with higher interest rates.

Griffin Funding works through regional wholesale representatives who handle broker relationships and pricing requests. Their quote process requires broker interaction with account managers rather than offering self-service pricing tools. This manual approach results in longer wait times for initial pricing and term sheets compared to lenders with automated systems.

Processing timelines typically range from 2–4 weeks once complete applications are submitted, with potential variations based on loan complexity and documentation requirements. While they serve a broad range of borrowers, the extended timeline may not meet the needs of borrowers competing in fast-moving markets.

9. Visio Lending

Visio Lending provides wholesale investment property financing through their broker channel, specializing in DSCR loans and short-term rental financing products. They focus on serving brokers whose clients invest in vacation rental properties and other high-income-generating real estate.

They offer loan amounts starting at $150,000 with competitive rates for qualified borrowers. Their programs require a minimum credit score of 680 and focus on rent-ready properties in desirable markets. This higher credit requirement and property focus may limit your ability to work with first-time investors or those purchasing properties in emerging markets.

Visio's wholesale process involves working with dedicated account representatives who handle pricing and preliminary underwriting. The manual quote system can extend initial response times compared to automated pricing platforms. For brokers who need to provide quick responses to borrowers evaluating multiple properties, this delay could impact your competitive position.

Standard closing timeframes range from 15–25 days for complete applications, with potential for acceleration on straightforward deals with experienced borrowers. Their focus on experienced investors may limit referral opportunities with newer market entrants.

10. Stratton Equities

Stratton Equities operates wholesale programs providing hard money and non-QM financing to mortgage brokers nationwide. Their product suite includes DSCR loans, bank statement programs, and commercial lending options, offering brokers flexibility in serving diverse borrower needs.

They offer loan amounts from $100,000 to $5 million with flexible credit requirements and competitive LTV ratios. Their programs accept various property types, including single-family homes, multifamily properties, and mixed-use buildings. This broad property acceptance gives brokers more options when working with investors pursuing different investment strategies.

Stratton Equities works through regional wholesale managers who handle broker relationships and pricing requests. Their manual quote process requires broker interaction rather than offering automated pricing tools. This approach means additional time spent coordinating with account managers rather than providing immediate responses to borrower inquiries.

Processing times typically range from 2–3 weeks for standard applications, with potential variations based on loan complexity and documentation completeness. While they offer competitive loan origination terms, the manual processes may slow down deal flow compared to more automated alternatives.

Secure Reliable Hard Money Loans for Your Borrowers with Constitution Lending

Enter a few basic borrower details into our automated loan pricer to generate instant loan quotes, term sheets, and approval letters.