Mixed-use properties combine residential and commercial units, often with commercial spaces on the ground floor and residences above.

While mixed-use real estate can be a compelling investment option, it's incredibly difficult to finance with a regular consumer mortgage. That’s because most banks assess borrowers based on their personal income and debt-to-income ratios, rather than evaluating the property’s actual cash flow potential.

The few banks that offer mixed-use financing products have stringent requirements and strict underwriting standards (e.g., high net worth, years of real estate investing experience, strong cash reserves), making it difficult for most real estate investors to qualify.

As a result, more real estate investors are turning to specialized commercial mortgages.

In this article, we discuss the three main types of commercial mixed-use financing options, the requirements you have to meet to qualify, what interest rates you can expect, and how to evaluate and choose a lender. Feel free to jump directly to the section most relevant to you.

- DSCR loans

- Commercial fix and flip loans

- Commercial bridge loans

- Factors to consider before partnering with a commercial lender

Throughout, we'll explain how we at Constitution Lending designed our processes to help real estate investors close quickly, without complications or last-minute drama.

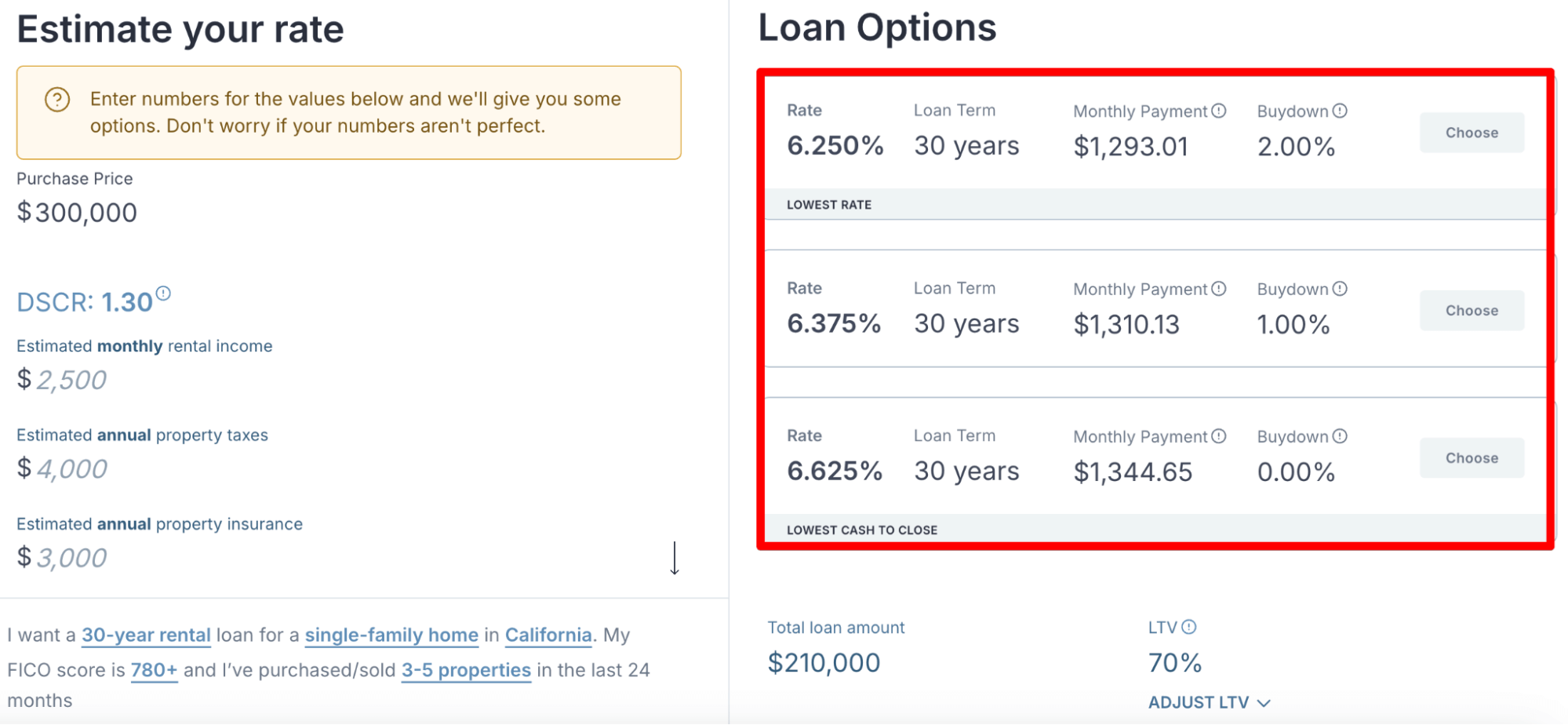

Use our automated loan pricer to generate instant quotes and see what interest rates, terms, and buydowns you qualify for.

DSCR (debt service coverage ratio) loans are 30-year financing products evaluated based on a commercial property's cash flow (i.e., expected rental income minus expected expenses).

For example, if a mixed-use property can generate $120,000 annually from all commercial and residential units combined, and its total expenses (mortgage payments, taxes, insurance, and operating costs) equal $100,000, the DSCR is 1.2 (120,000 ÷ 100,000 = 1.2). This ratio is what lenders consider when deciding whether to approve an application.

The higher a commercial property’s DSCR, the better, because it provides a stronger cash flow buffer against vacancies, unexpected repairs, or market downturns.

DSCR lenders don't evaluate a borrower’s personal financial profile (e.g., salary, employment history, net worth, tax returns) like banks, which offer the following advantages:

- Borrowers aren’t limited by their personal income or debt-to-income ratio because the lender doesn’t consider those factors. This makes it possible to qualify for much larger amounts than consumer bank loans.

- Borrowers with complex finances can qualify as long as the property they want to purchase meets the DSCR threshold. It doesn't matter if you earn non-W-2 income, have high debt-to-income ratios, or own an extensive real estate portfolio. This makes DSCR loans perfect for leveraged real estate investors who can't qualify for conventional bank financing.

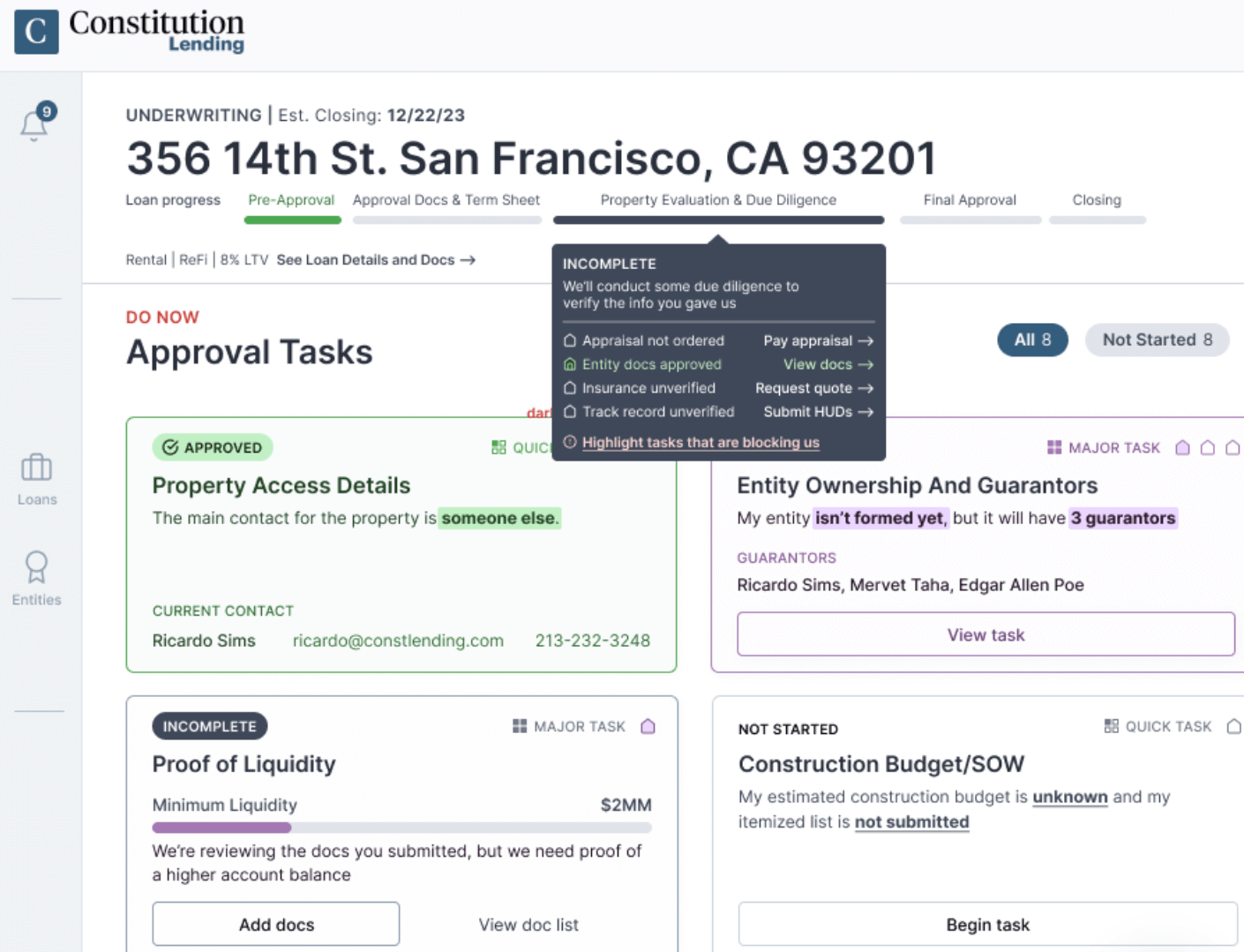

- Borrowers don't need to submit tax returns, pay stubs, or other personal financial documents that banks typically require. You only need entity documents, proof of insurance, and bank statements. This lightweight paperwork requirement enables much faster closing times. For example, Constitution Lending can close DSCR loans in 7 to 14 days.

Interest rates on mixed-use DSCR loans typically range from 6.25% to 8.50%, depending on factors such as DSCR, credit score, loan-to-value (LTV) ratio, and the specific property type and location. If you’d like to learn which factors influence your interest rates, we have an entire article on the topic you can read here.

Requirements to Qualify for Mixed-use DSCR Loans

Mixed-use DSCR loans have relatively straightforward qualification criteria:

- A minimum DSCR of 0.75 to 1.00 (meaning the property's income covers at least 75% of its expenses)

- A minimum credit score of 660

- A maximum LTV ratio of 80% for purchases and 75% for refinancing

- 2–4 unit and 5–20 unit mixed-use properties can qualify

How to Apply for a DSCR Loan

You can apply for a DSCR loan with Constitution Lending in under 5 minutes:

- Use our automated loan pricer to generate instant quotes by entering your property details, estimated rental income, and credit score.

- Select your preferred loan option and enter your contact information.

- Download a copy of the quote as well as a term sheet and pre-approval letter.

- Submit required documents through our digital documents portal.

- We appraise the mixed-use property and close with the title company in 7 to 14 days. In urgent situations when borrowers needed to close even faster than this, we’ve closed in just 4 days.

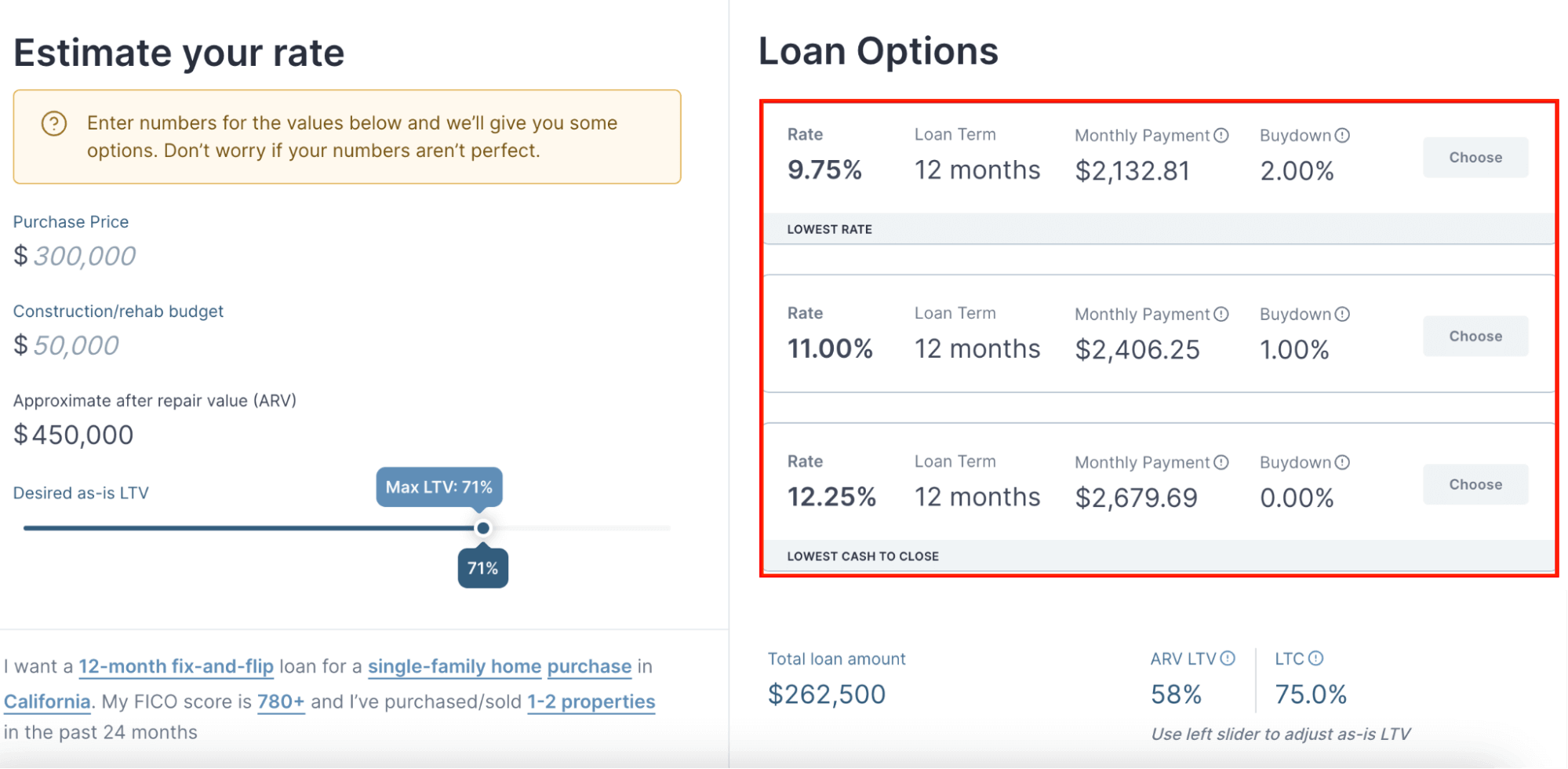

If you're looking to purchase a distressed mixed-use property, renovate it, and sell it for a profit, commercial fix-and-flip loans provide the right financing structure for this strategy.

Like DSCR loans, fix-and-flip loans aren't evaluated based on a borrower’s personal financial profile. Borrowers can qualify even with a leveraged real estate portfolio, complex finances, or non-W2 income that would disqualify them from traditional bank financing.

Instead, commercial lenders evaluate applications based on the total project cost (purchase price plus renovation expenses) relative to the property's estimated after-repair value (ARV). The larger the potential profit margin between these numbers, the higher your chances of qualifying.

These commercial real estate loans typically offer:

- Up to 85% of the purchase price plus 100% of verified renovation costs

- Amortization periods ranging from 12 to 18 months, providing sufficient time to complete renovations and find buyers

- Conversion options allowing you to convert your fix-and-flip loan into a long-term DSCR loan if you decide to hold the property as a rental instead of selling

Requirements to Qualify for Fix-and-Flip Loans

Commercial fix-and-flip loan products typically have four main requirements:

- A down payment of 15% to 40% of the purchase price

- Cash reserves equivalent to 3 months of monthly payments to cover carrying costs during renovation

- An after-repair LTV of 70%

- A minimum credit score of 660

You can learn more about the criteria you have to meet to secure fix-and-flip loans here.

How to Apply for a Fix-and-Flip Loan

The application process for fix-and-flip loans is similar to DSCR loans but focuses on renovation and construction details:

- Use our fix-and-flip loan pricer to generate quotes based on purchase price, renovation budget, and after-repair value.

- Adjust variables such as as-is LTV, after-repair LTV, and construction budgets to see how they affect your terms.

- Submit your preferred quote along with your contact information.

- Provide a detailed scope of work and construction budget from a licensed contractor.

- We complete the appraisal process for both the current and the after-repair value.

- We close the commercial real estate loan within 7 to 14 days and begin paying for renovation costs as work progresses.

Bridge loans are short-term, mixed-use property financing options (typically 3 months to 2 years). They help real estate investors bridge the gap between when they need capital and when they can secure permanent financing or complete a sale.

Real estate investors commonly use bridge loans when they want to purchase a new mixed-use property but are waiting for another property in their portfolio to sell.

Bridge loans were historically limited to single-family residential properties, but specialized lenders like Constitution Lending have expanded their offerings to include mixed-use properties with 2–4 and 5–20 units.

Bridge loans offer several advantages for mixed-use property investments:

- They have much faster approval and funding than permanent financing. Investors can act quickly on opportunities without waiting for other assets to sell.

- They are extremely flexible and can be used for acquisitions, refinancing, or cash-out scenarios.

- Most bridge loans offer interest-only monthly payment options to minimize carrying costs.

Requirements to Qualify for Bridge Loans

- Up to 75% LTV of the property's current value

- The commercial use property itself serves as collateral, and additional properties may be required for larger loans

- A minimum credit score of 660

- A clear plan for repaying the loan (e.g., sale, refinance, or cash-out from other assets)

How to Apply for a Bridge Loan

The application process for bridge loans is very similar to other commercial real estate loans and focuses on the value of the property relative to the loan amount:

- Use our loan pricer to see available terms based on property value and loan amount.

- Download a copy of the quote, term sheet, and pre-approval letter.

- Through our documents portal, provide current property documentation and proof of other assets if needed.

- Complete appraisal for current market value.

- Close within 7 to 14 days.

Read more: A Guide on How to Get a Loan for an Apartment Complex

Selecting the right lender can mean the difference between securing favorable rates quickly and reliably versus dealing with expensive mixed-use property financing that's slow and unreliable. Here are the two most important factors to consider when evaluating a lender:

Are They a Direct Lender or a Loan Broker?

A major problem in commercial real estate lending is last-minute rejections. We frequently hear from borrowers who applied with other lenders, received initial approval, but then faced unexpected rejection when closing approached. Some borrowers have been rejected on the actual day of closing despite being told early in the process that they qualified.

Last-minute rejections usually happen when borrowers work with loan brokers.

When you apply with a broker, you're working through a middleman who doesn't provide the actual funding and therefore can't definitively determine if you qualify. Brokers must submit an application to their lending partners and wait for them to complete underwriting before providing you with a final answer.

The broker may tell you early on that you qualify based on their preliminary review. But if the lender finds issues the broker missed, you could face a rejection, even after being told you qualify.

At Constitution Lending, we are a direct lender who uses our own capital to fund loans. We set our own underwriting rules and can tell you if you qualify as soon as we review your documents. There are no last-minute surprises because we do not depend on another lender's decision.

How Quickly Can They Close?

We also recommend evaluating a lender's closing speed because it helps you compete with fast cash buyers in competitive markets.

Most lenders advertise fast closing times but fail to deliver. We regularly speak with borrowers who were promised 7 to 14-day closings by other lenders but experienced delays of 30+ days, causing them to lose deals to cash buyers.

Rather than taking a lender's word about their speed, examine how quickly they provide term sheets, pre-approval letters, and loan quotes. This demonstrates their internal efficiency, which directly affects closing speed.

The fastest lenders have automated systems that generate same-day quotes, term sheets, and pre-approval letters. If a lender takes multiple business days to provide basic documents, it suggests internal inefficiencies that will affect your closing timeline.

At Constitution Lending, we use automated tools such as our loan pricer and documents portal to accelerate the entire application, approval, and closing process.

Instead of waiting several days for quotes, you can generate them immediately by answering a few questions in our pricer.

Our organized documents portal lets you submit everything in one submission, rather than waiting for a loan officer to specify the required documents. It also shows exactly where your application stands and what steps remain.

Once you submit all documents, we review them, give you a clear answer regarding your eligibility within hours, and close within 7 to 14 days.

Here's what borrowers say about our speed and reliability:

Secure Fast and Affordable Real Estate Investment Loans with Constitution Lending

If you're ready to finance a mixed-use property investment, use our automated loan pricer to see what loan terms and rates you qualify for. You can generate quotes for DSCR loans, fix-and-flip loans, or bridge loans within seconds and receive a term sheet immediately.

Frequently Asked Questions

Is mixed-use considered commercial?

Yes, mixed-use properties are typically classified as commercial real estate because they contain commercial units. This classification affects financing options, with most residential loan programs being unavailable for these properties.

Does Fannie Mae allow mixed-use properties?

Fannie Mae has very limited programs for mixed-use properties and strict requirements that make qualification difficult. Most investors use commercial lenders specializing in mixed-use financing instead.

How much do you need to put down on a mixed-use property?

Down payment requirements vary by loan type. DSCR loans typically require 20-25%, fix-and-flip loans require 10-25%, and bridge loans require 25-30% down payments.

What is the interest rate for mixed-use property loans?

Interest rates typically range from 6.75% to 12%, depending on the loan type, property characteristics, borrower qualifications, and market conditions. DSCR loans generally offer the lowest rates, while short-term loans like fix-and-flip and bridge loans carry higher rates.

What should I look for in a lender?

Focus on two key factors: whether they're a direct lender (not a broker) and how quickly they can provide quotes and close loans. Direct lenders reduce the risk of last-minute rejections, while fast lenders help you compete with cash buyers.

What are the typical terms for a commercial loan on a mixed-use property?

DSCR loans offer 30-year terms with fixed rates, fix-and-flip loans provide 12-month terms, and bridge loans range from 3 months to 2 years. Loan amounts typically range from $150,000 to $3,000,000, depending on the lender and property type.