As the name suggests, peer-to-peer lending involves lending money to borrowers (e.g., small business owners, tech startups, real estate investors, consumers) in exchange for regular principal and interest payments. Typically, individual investors contribute capital to a shared pool, which borrowers then draw from to purchase real estate, cover operating expenses, or fund business growth.

P2P lending offers a few advantages over more traditional investment options:

- The potential for higher returns: P2P lending typically yields between 8% and 15%, depending on the borrower’s credit history, allowing investors to earn returns higher than those of bonds, REITs, and high-yield savings accounts.

- Low minimum investments: Most P2P lending platforms allow investors to start with a couple of hundred or a thousand dollars. Some platforms have minimum investments as low as $25.

- Better diversification: Because you can start investing with such small amounts, it’s easier to diversify across multiple loans.

Despite those benefits, the platform you choose to lend through matters because it determines the quality of deals you can access. The most common reason we see P2P investors lose money is that they invest through platforms filled with bad loans on the brink of default.

To help investors make better decisions and avoid unnecessary risk, we wrote this guide covering the factors you should consider before investing with a P2P lending platform.

We then review 5 P2P lending platforms and how they match up against those factors, starting with ourselves, Constitution Lending.

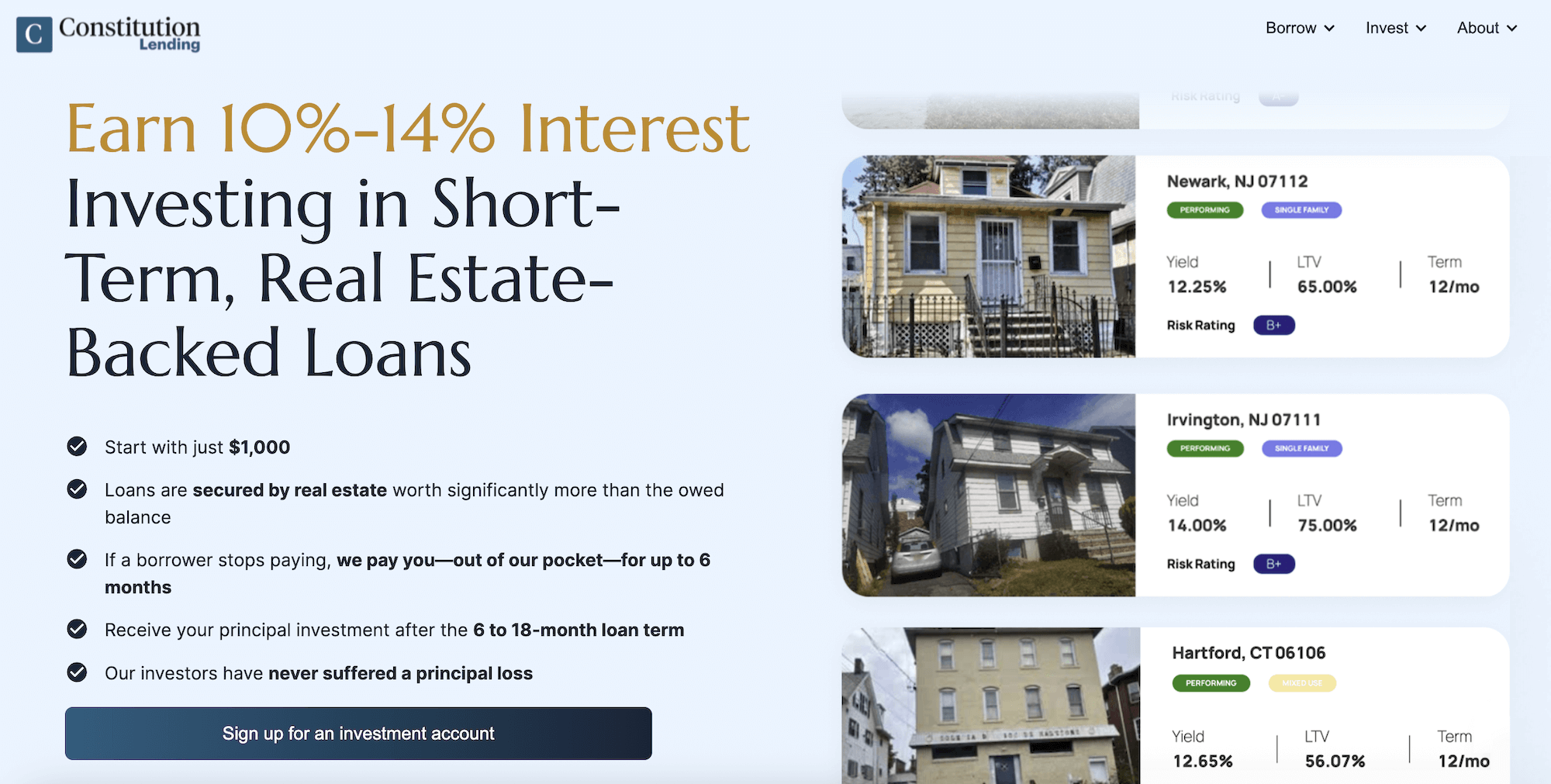

Who are we? Constitution Lending is a private real estate lender that allows investors to purchase shares of loans we originate, starting with $1,000. Interest rates on our loans range from 10% to 14%, and due to their quality, our investors have never lost principal. Sign up for a free account to browse our loan options.

Key Factors to Consider Before Investing in P2P Lending

Are the Loans Secured by Stable Collateral?

The two biggest risks in P2P lending are (1) borrower defaults and (2) market and economic downturns.

You can protect yourself against both default and market risk by investing in loans collateralized by a stable asset, such as real estate, that’s worth substantially more than the total owed amount. That way, if the borrower defaults, you are protected. The platform can initiate foreclosure, sell the underlying asset, and use the sale proceeds to repay debtors the outstanding amount (principal and interest).

In addition, because the underlying real estate is worth much more than the owed amount, it protects you from economic downturns; real estate prices can fall, and you can still recover the full owed amount. For example, if you invest in a $700,000 loan secured by a $1 million property, the property’s value can fall to $700,000, and you can still recover the owed amount from the sale proceeds.

That said, from what we see, most P2P lending platforms contain extremely risky loans with no collateral to protect against default. If a borrower defaults, the lender must take legal action and use third-party debt collectors to recover the debt. This takes years, and borrowers rarely end up paying the full amount, leaving debtors at a loss.

Essentially, collateral provides a much more reliable recovery mechanism than chasing individual borrowers.

What Is The Platform’s Default Rate?

While collateral protects against default risk, the best financial institutions maintain low default rates in the first place. So, we recommend assessing a P2P lending platform’s default rate before investing in its loans.

Quality lending platforms should maintain default rates significantly below the U.S. average of 4% through rigorous underwriting standards and established relationships with experienced borrowers.

Do They Invest Alongside You?

The reason most P2P lending platforms are filled with bad loans comes down to a fundamental flaw in their business model: their financial incentives don’t align with your goal of lending only to high-quality borrowers.

Most P2P lending platforms generate revenue through origination fees, servicing fees, and transaction commissions. They're incentivized to facilitate as many loans as possible, regardless of borrower quality. This leads to minimal vetting and underwriting, attracting the lowest-quality borrowers (i.e., those who can't secure traditional financing due to poor credit and repayment histories).

Instead, we recommend choosing a platform that originates all the featured loans with its own capital. This way, they have skin in the game and are financially motivated to present you only with high-quality loan options.

Platforms that simply collect fees without co-investing have no financial consequences if borrowers default. They can facilitate loans to risky borrowers and pass all risk to investors while collecting guaranteed commissions.

How Long is the Investment Term?

Consider the loan term, as it determines when you can access your original investment again.

We recommend choosing shorter-term loans of 6 to 12 months, since they let you get your principal back faster and reinvest or withdraw your capital more frequently, rather than waiting years.

1. Constitution Lending

Invest in Real Estate-Secured Loans Yielding 10% to 14% Annually

Constitution Lending operates differently from traditional peer-to-peer lending platforms. Rather than connecting individual lenders with unknown borrowers, we’re a private lender that originates real estate loans to experienced borrowers and enables investors to purchase fractional ownership in these loans starting at $1,000.

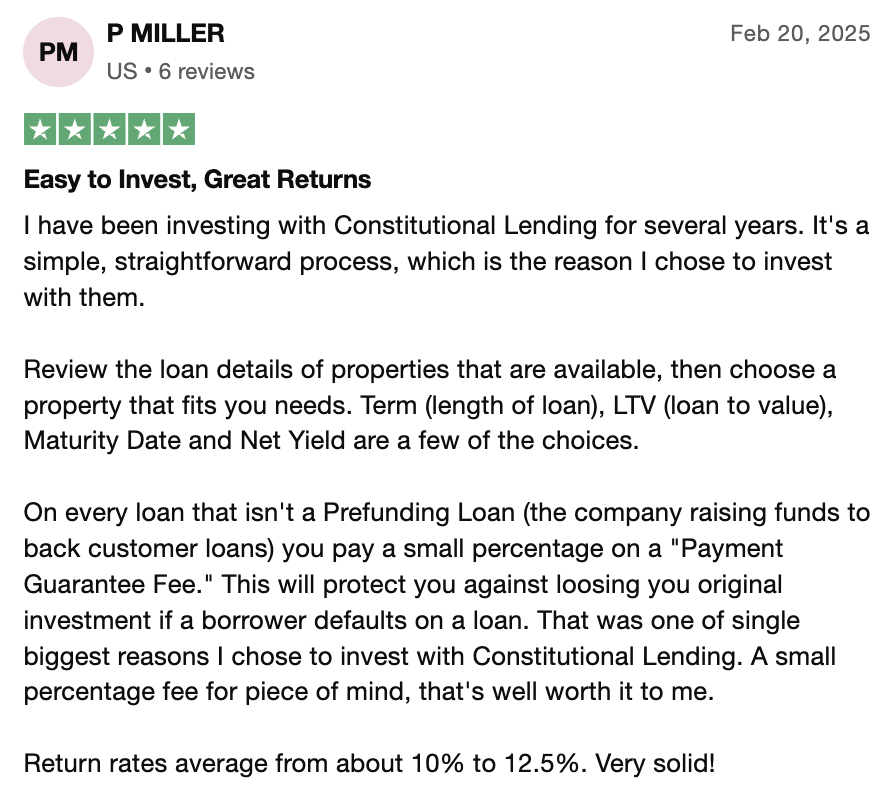

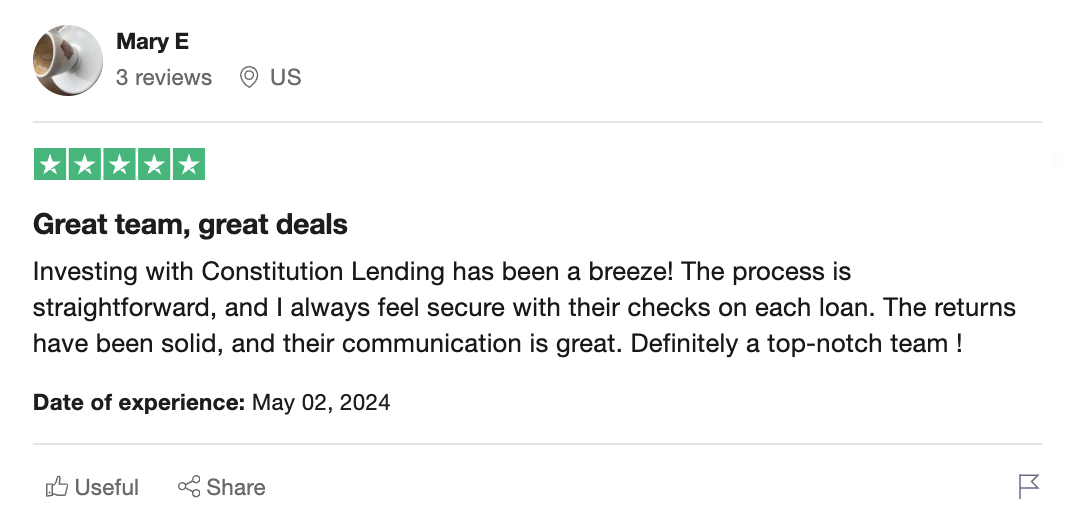

This is what borrowers say about our loan options’ performance:

Here's how Constitution Lending addresses the factors mentioned above:

Our Loans Are Secured by Real Estate Worth Much More Than the Loan Amount

Our loans are secured by the property being purchased. This mitigates default risk because, if a borrower stops paying, we can recover your principal and any accrued interest by liquidating the underlying property.

In addition, we protect our investors from market risk by lending a maximum of 75% of a property’s value. So, if you invest in a $750,000 loan, you’ll be secured by at least $1 million in real estate. This 25% borrower equity cushion means that property prices can fall by 25% and the selling price can still satisfy the entire owed amount.

Read more: 7 Best Alternative Investment Platforms & How to Choose

Our Borrower Default Rate Is Under 2%

Due to our strict underwriting standards and decade-long relationships with experienced real estate professionals, our default rate remains under 2% — half the national average of 4% for real estate loans.

We only lend to real estate investors with great credit, a proven track record of successful projects, and sufficient experience to execute their business plans. This careful selection process protects investors against default risk.

We Invest Alongside You

Unlike P2P lending platforms that simply facilitate transactions, we originate every loan with our own capital and maintain a 50%+ ownership stake throughout the entire loan term. Our financial success depends directly on loan performance, ensuring our interests align perfectly with yours.

Investors are confident that we're not simply collecting fees while shifting risk to them. If a loan performs poorly, we lose money too, which motivates rigorous underwriting standards and careful borrower selection.

Read more: Top 5 Yieldstreet Alternatives | Higher Returns & More Liquidity

Short-Term Investment Horizon

Our loans have terms of just 6 to 12 months, allowing investors to access their principal quickly rather than being locked into multi-year commitments like traditional P2P loans.

Payment Guarantee Feature

We're the only real estate investment platform offering payment guarantees on all loans. If borrowers stop making payments, we pay investors out of our own pocket for up to six months while resolving the situation through loan restructuring or foreclosure.

10% to 14% Interest Returns

Interest rates on our fix-and-flip, bridge, and construction loans range from 10% to 14%, providing significantly higher yields than most peer-to-peer lending platforms, savings accounts, or traditional investments.

How to Start Investing in Constitution Lending Real Estate Loans

You can begin investing in our real estate loans in under five minutes:

- Create your investment account by providing your name and email address.

- Review available loans on your dashboard, including loan-to-value ratios, interest rates, and borrower profiles.

- Conduct due diligence by examining loan metrics such as LTV, after-repair LTV, borrower credit score, and property details.

- Fund your investment starting at $1,000 by linking your bank account or IRA.

- Receive monthly interest payments on the first of each month, with full principal returned at loan maturity.

Open a free investment account to explore current loan opportunities and start earning 10% to 14% annual returns.

2. Prosper

Prosper is one of the oldest peer-to-peer lending platforms in the United States, connecting individual lenders with borrowers seeking personal loans for debt consolidation, home improvements, or other consumer purposes.

- Expected Returns: Prosper advertises historical returns ranging from 5.3% to 8.3% annually, depending on the risk level of loans selected. However, these returns don't account for defaults and charge-offs, which can significantly reduce actual investor returns.

- Investment Structure: Prosper facilitates unsecured personal loans, meaning there's no collateral backing the debt. If borrowers default, investors have limited recourse beyond debt collection efforts, which rarely recover the full loan amount.

- Default Risk: Prosper's loans carry significant default risk due to their unsecured nature and the platform's focus on consumer lending to individuals who may not qualify for traditional bank loans. The platform doesn't invest alongside P2P lenders, creating potential misalignment of interests.

- Liquidity: Prosper loans typically have three or five-year terms with no early exit options. Investors must commit capital for the full loan term, with no liquidity alternatives.

The platform's focus on unsecured consumer debt and lack of co-investment make it riskier than real estate-secured alternatives like Constitution Lending.

3. Kiva

Kiva operates as a nonprofit peer-to-peer lending platform that facilitates microloans to entrepreneurs and students in developing countries. The platform focuses on social impact rather than investor returns.

- Expected Returns: Kiva loans generate 0% interest returns for P2P lenders, as the platform operates on a charitable model. Lenders can expect to recover their principal if borrowers repay successfully, but earn no financial return on their investment.

- Investment Structure: Kiva facilitates small loans (typically $25 to $500) to borrowers in developing economies for business development, education, or other purposes. Loans are unsecured and processed through local field partners.

- Default Risk: While Kiva reports repayment rates above 95%, the platform provides no guarantees and offers limited recourse if borrowers default. Currency fluctuations and political instability in borrower countries add additional risk factors.

- Social Impact: Kiva's primary value proposition is social impact rather than financial returns. P2P lenders support entrepreneurship and education in underserved communities worldwide.

For investors seeking financial returns rather than charitable impact, Kiva's zero-interest model makes it unsuitable compared to yield-generating alternatives.

4. Zidisha

Zidisha is a peer-to-peer lending platform that connects lenders directly with entrepreneurs in developing countries, eliminating local intermediaries that other microfinance platforms use.

- Expected Returns: Zidisha allows borrowers to set their own interest rates, typically ranging from 0% to 25% annually. However, the platform's focus on very small loans and high default risk in developing markets often results in negative returns for lenders.

- Investment Structure: The platform facilitates small loans (usually under $500) to individual entrepreneurs for business development purposes. Loans are unsecured and processed directly between lenders and borrowers.

- Default Risk: Zidisha carries significant default risk due to limited borrower verification, lack of local oversight, and economic instability in target markets. The platform provides no guarantees or collection services for defaulted loans.

- Geographic Risk: Lending to borrowers in developing countries introduces additional risks, including currency devaluation, political instability, and limited legal recourse for debt collection.

Zidisha's high-risk profile and minimal investor protections make it unsuitable for investors seeking reliable returns with principal protection.

5. LenderMarket

LenderMarket is a European peer-to-peer lending platform that allows investors to purchase loans originated by various lending companies across multiple countries.

- Expected Returns: LenderMarket advertises potential returns of 8% to 18% annually, depending on loan types and risk levels selected. However, actual returns vary significantly based on originator performance and default rates.

- Investment Structure: The platform operates as a marketplace where multiple loan originators sell portions of their loan portfolios to investors. Loans include personal loans, business loans, and some real estate-backed debt.

- Default Risk: LenderMarket's default risk varies by originator, with some maintaining acceptable performance while others experience high default rates. The platform doesn't invest alongside investors, creating potential misalignment of interests between the marketplace and loan originators.

- Buyback Guarantee: Some loans on LenderMarket include buyback guarantees where originators promise to repurchase defaulted loans after a specified period. However, these guarantees depend on the financial stability of individual originators.

- Geographic Diversification: LenderMarket offers exposure to loans across multiple European countries, providing geographic diversification but also introducing regulatory and currency risks.

While LenderMarket offers higher potential returns than some alternatives, the reliance on third-party originators and lack of direct collateral control create additional risk layers compared to direct real estate lending.

Invest with Constitution Lending and Earn 10% to 14% Interest Returns

After evaluating these five platforms against our key criteria, Constitution Lending provides the strongest combination of high returns, principal protection, and aligned interests for investors seeking reliable passive income.

- Superior Returns: Our 10% to 14% annual returns exceed traditional p2p lending platforms while providing better security through real estate collateral.

- Aligned Interests: Our co-investment model ensures we share in both gains and losses, motivating careful loan origination and borrower selection. Our co-investment model ensures we share in both gains and losses, motivating careful loan origination and borrower selection.

- Principal Protection: Real estate backing with 75% or lower loan-to-value ratios provides substantial downside protection that unsecured loans cannot match.

- Payment Guarantees: Our unique payment guarantee feature provides additional security that no other platform offers.

- Professional Management: Our decade of lending experience and established borrower network deliver consistently low default rates and reliable performance.

Sign up for an investment account here and learn more about our investment opportunities.

Frequently Asked Questions

Is P2P Lending a Good Alternative Investment?

P2P lending can be a good investment when you choose platforms with strong borrower vetting, collateral backing, and aligned interests. However, many traditional p2p lending platforms carry significant default risk due to poor underwriting and unsecured loan structures. Real estate-secured lending offers better principal protection and more predictable returns.

How Much Should I Invest in P2P Lending?

We recommend starting with small amounts to test platform performance before committing larger sums. With Constitution Lending, you can begin with just $1,000 and gradually increase your allocation as you gain confidence in the returns and security. Diversification across multiple loans reduces concentration risk.

How to Make Money from Peer-to-Peer Lending?

Investors earn money through monthly interest payments from borrowers and principal recovery at loan maturity. Choose platforms with high-quality borrowers, real estate collateral, and payment guarantees to maximize returns while minimizing default risk. Reinvesting monthly payments compounds returns over time.

What Is the Best Platform for Peer-to-Peer Lending?

Constitution Lending offers the best combination of high returns (10% to 14%), principal protection through real estate collateral, and payment guarantees. Unlike traditional p2p lending platforms, we invest alongside you and maintain rigorous underwriting standards for experienced real estate borrowers.

How Does Peer-to-Peer Lending Work?

Peer-to-peer lending connects individual lenders with borrowers through online platforms. Lenders provide capital in exchange for interest payments, while platforms facilitate loan origination, underwriting, and servicing. The best platforms offer collateral backing and co-investment to protect lender interests.

When Is a Peer-to-Peer Loan a Good Idea?

P2P lending works best when platforms maintain high underwriting standards, offer collateral protection, and invest alongside lenders. Avoid platforms focused solely on fees without co-investment, as they lack incentives to maintain loan quality. Real estate-secured loans provide better protection than unsecured consumer debt.

What Are the Risks Associated with Peer-to-Peer Lending?

Primary risks include borrower defaults, platform failure, liquidity constraints, and lack of FDIC insurance protection. Unsecured loans carry a higher risk than collateralized debt. Choose platforms with payment guarantees, real estate backing, and proven track records to minimize these risks.