In this guide, we explore seven passive real estate investment vehicles, comparing them based on their safety, expected returns, lock-up periods, and minimum starting investment.

1. Real Estate Debt

Real estate debt investing involves lending money to real estate borrowers (or investing fractionally with a lender who does) in exchange for monthly interest payments and the eventual repayment of the loan amount (i.e., principal) at the end of the term.

This differs from traditional real estate investing because you don’t own the property itself; you own the debt secured by the property, which offers numerous advantages:

- Protection from market downturns: Debt investors are best protected during downturns because they get paid first and in full from any sale proceeds. For example, if you invest in a $700,000 loan secured by a $1 million property and the property’s value falls to $700,000, you recover your full investment through a sale. Real estate investors have to lose their entire equity before you lose a cent.

- Strong returns and reliable cash flow: Interest rates on short-term real estate loans (fix-and-flip, ground-up construction, and bridge loans) range from 10% to 14%, with borrowers making interest payments monthly.

- Short investment horizons: Most fix-and-flip, bridge, and construction loans have terms between 6 and 12 months, so you receive your original investment relatively quickly. You don’t have to commit for several years like with rental properties.

- Low minimums and no day-to-day involvement: When you invest with a private lender like Constitution Lending, you don’t need $200,000+ to originate entire loans, nor do you require hands-on management. You can invest in the loans we originate, starting with as little as $1,000, and receive borrower interest payments on an entirely passive basis.

Let’s cover these factors in more detail below.

Significant Capital Protection Against Market Downturns and Market Fluctuations

As we discussed above, real estate debt provides superior capital protection compared to direct property ownership because debt holders are paid first and in full from any sale. Real estate investors only receive proceeds after all debts are satisfied.

This capital protection is even stronger when you invest through a high-quality private lender like Constitution Lending. That’s because we lend a maximum of 75% of a property’s value, and the borrower has to provide the remaining 25% in the form of a down payment. This gives our investors a healthy 25% borrower equity cushion; the property’s value can fall by 25%, and debt investors can still recover their full principal investment.

Because of this protection, our investors haven’t lost principal to date.

Read more: How to Invest in Debt Secured by Real Estate

Strong Returns and Reliable Cash Flow

At Constitution Lending, our short-term real estate loans have interest rates of 10% to 14%. Borrowers make monthly interest payments, providing consistent cash flow throughout the loan term.

We also offer a payment guarantee feature on all loans. If a borrower stops making payments, we pay investors from our own funds for up to 6 months while addressing the situation via loan restructuring or, if necessary, foreclosure and liquidation. This way, you get reliable passive income every month, even if the borrower doesn’t pay.

That said, we lend exclusively to experienced, high-quality borrowers with a track record in real estate fix-and-flips or construction, strong credit profiles, and a flawless repayment history. As a result, defaults are extremely rare: less than 2% of our borrowers defaulted, compared with a 4% U.S. average.

Short Investment Horizons

Real estate debt offers excellent liquidity compared to other real estate investments. Our real estate loans have terms of 6 to 12 months, after which borrowers sell or refinance their properties and repay the owed balance in full. We don’t lock up your capital for years.

Low Minimums and No Day-to-Day Involvement Needed

Traditional real estate lending requires hundreds of thousands of dollars to fund entire loans, deep expertise and experience, and hands-on management.

However, with Constitution Lending, you can invest in the loans we’ve already originated, which offers multiple benefits:

- Lower capital requirements: You don't need $200,000 to $500,000 to fund an entire loan. Retail investors can participate in high-quality real estate debt with $1,000.

- No sourcing, underwriting, or servicing required: We handle all loan origination, underwriting, and servicing. Investors receive a true source of passive income in the form of borrower interest payments.

- Built-in diversification: Small minimums allow investors to spread capital across multiple loans and diversify their investment portfolio, reducing the risk of a single borrower default.

How to Start Investing with Constitution Lending

You can begin investing in our real estate debt platform in under five minutes:

- Create your investment account by providing your name and email address.

- Review available loans on your dashboard, including LTV ratios, interest rates, borrower profiles, and property type (e.g., duplexes, single-family homes, commercial properties, etc.).

- Conduct due diligence by examining loan metrics such as property values, borrower credit scores, and repayment structures.

- Fund your investment starting at $1,000 by linking your bank account or IRA.

- Receive monthly interest payments in your wallet, which you can withdraw or automatically reinvest

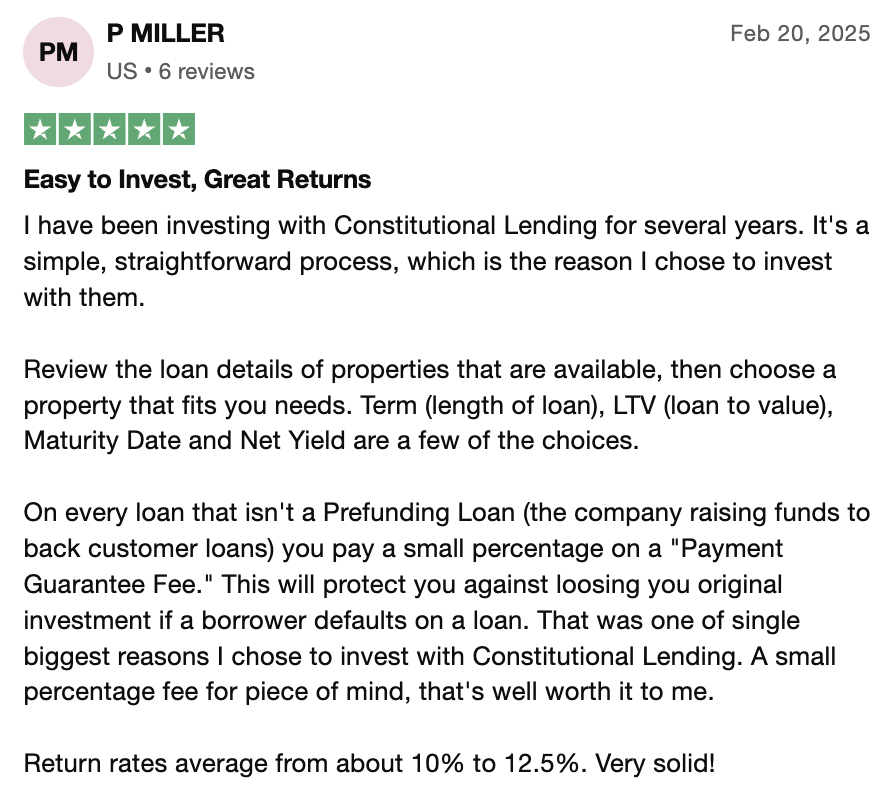

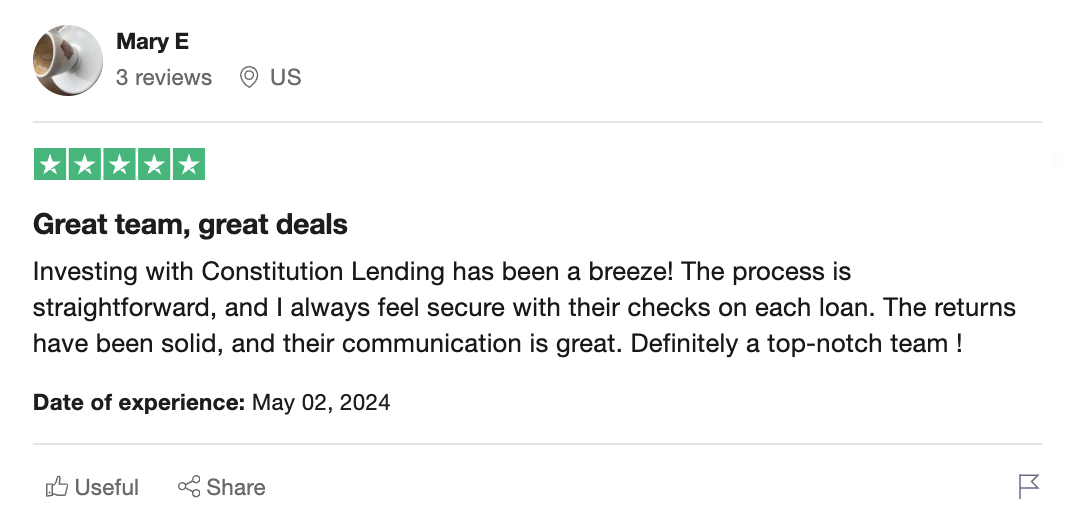

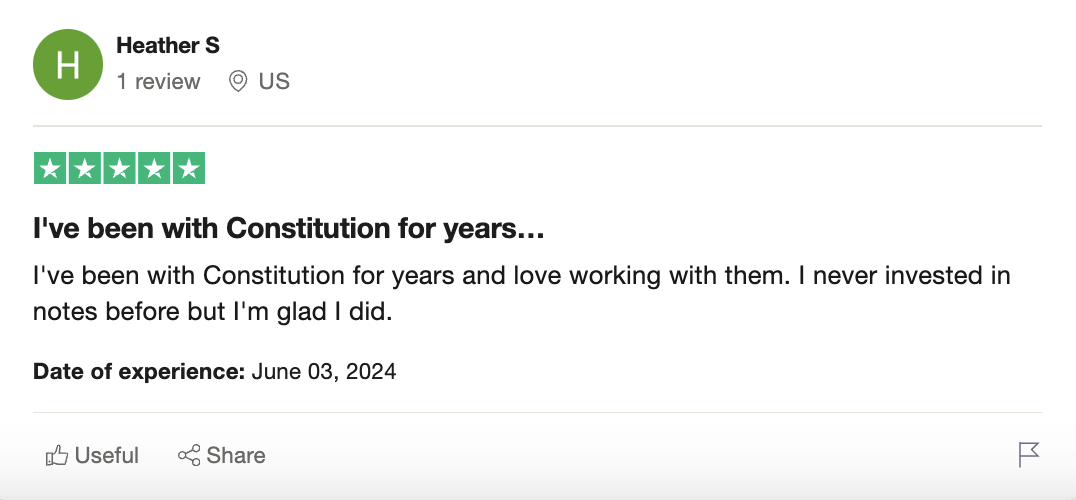

Here’s what investors say about our real estate debt investment options.

Open a free investment account to explore current loan opportunities and start earning 10% to 14% interest payments.

2. Real Estate Funds

Real estate funds pool investor capital to purchase multiple properties or loans, providing diversification and professional management. Real estate funds may include mutual funds, REITs, and private equity funds.

Fund managers look for undervalued or commercial properties in emerging, high-growth areas, purchase them, and earn returns through monthly rent payments and long-term property appreciation.

At Constitution Lending, we offer a specialized non-performing loan fund that purchases distressed real estate debt at significant discounts and earns returns by recovering the full amount owed.

We can do this through multiple avenues (depending on the borrower’s cooperation and market values), including foreclosing on the property, buying the property ourselves for under-market value, restructuring the loan to get the borrower paying again, and selling the loan at a profit.

Our non-performing loan fund addresses passive income, hands-off criteria as follows:

- Strong returns: The fund generated a 57.60% return for investors in 2024 by purchasing non-performing loans at discounts and recovering full loan balances through borrower negotiations, loan modifications, or foreclosure proceedings.

- Capital protection: We only purchase loans with LTVs of 60% or less, providing substantial equity cushions. Most loans have significant borrower equity protecting against market volatility.

- Investment horizon: The fund has an 18-month lock-up period, after which investors receive quarterly distributions. While longer than our performing loan options, this timeframe remains reasonable for alternative investments.

- Low minimums: Investors can start with as little as $20,000, significantly less than the $1 million to $2 million typically required to purchase non-performing loans directly from banks.

If you’d like to learn more about our non-performing loan fund, this article walks through our investment strategy.

3. REITs (Real Estate Investment Trusts)

REITs allow investors to purchase shares in companies that own and operate income-producing real estate. Publicly traded REITs offer easy access to real estate markets through stock exchanges and don't require investors to be accredited, making them perfect for beginners.

- Strong returns: REITs have historically generated average annual returns of 8% to 12%. However, performance varies significantly by property type and market conditions.

- Capital protection: REITs provide limited downside protection as share prices fluctuate with market sentiment and real estate values. During market downturns, REIT values can decline substantially.

- Investment horizons: Publicly traded REITs offer excellent liquidity, as shares can be bought and sold during market hours. However, this liquidity comes with increased volatility.

- Low minimums: Most REITs can be purchased with minimal capital in the form of an ETF, often less than $100 per share.

While public and private REITs offer accessibility and diversification, they lack the capital protection and higher yields available through real estate debt investing.

4. Long-Term Rental Properties

Long-term rental properties involve purchasing residential or commercial real estate and leasing it to tenants for extended periods, typically one year or longer.

- Returns: Rental properties typically generate 3% to 8% annual cash flow, plus potential appreciation over time. Total returns may reach 8% to 12% annually in favorable markets.

- Capital protection: Direct property ownership exposes investors to market volatility, unlike debt investors, who enjoy protection. Property values can decline, affecting both cash flow and equity.

- Investment horizons: Real estate ownership is inherently illiquid. Selling commercial properties requires marketing, negotiations, and closing processes that can take months to complete.

- Capital and effort requirements: Rental properties require substantial down payments (typically 20% to 25%) and ongoing management responsibilities, including tenant screening, maintenance, rent collection, and handling vacancies.

5. House Hacking

House hacking means purchasing a multi-unit property, living in one unit, and renting out the others to offset mortgage payments. This strategy combines homeownership with rental income generation.

- Returns: House hacking can significantly reduce living expenses while building equity. Effective returns vary widely based on local rental markets and property management efficiency.

- Capital protection: As with direct ownership, house hackers are exposed to property value fluctuations, unlike debt investors, who are protected.

- Investment horizons: House hacking typically requires multi-year commitments, as frequent moves undermine the strategy's benefits.

- Requirements: This strategy requires significant personal involvement in property management and limits housing flexibility since you must live on-site.

6. Short-Term Rentals

Short-term rentals involve purchasing properties (e.g., vacation rentals, Airbnb listings, serviced apartments) and renting them to travelers through platforms like Airbnb and VRBO. This strategy can generate higher income than long-term rentals in tourist destinations.

- Returns: Successful short-term rentals can generate 10% to 20% annual returns in prime locations, though income varies significantly with seasonality and local regulations.

- Capital protection: Like other direct ownership strategies, short-term rental investors are exposed to property value fluctuations and market downturns.

- Investment horizons: Properties remain illiquid assets that can take months to sell during market transitions.

- Requirements: Short-term rentals require intensive management, including marketing, guest communications, cleaning coordination, and regulatory compliance. Many cities have implemented restrictions limiting short-term rental operations.

7. Real Estate Partnerships

Real estate partnerships mean pooling resources with other accredited investors to purchase larger properties or portfolios. Partners typically contribute capital, expertise, or management services in exchange for a share of profits.

- Returns: Partnership returns vary widely based on property types, market conditions, and profit-sharing arrangements. Successful partnerships may deliver annual returns of 8% to 15%.

- Capital protection: Protection levels depend on partnership structure and whether partners invest in debt or equity positions within the venture.

- Investment horizons: Most real estate partnerships require multi-year commitments with limited liquidity options during the partnership term.

- Requirements: Partnerships demand extensive due diligence on both investment properties and partner qualifications. Ongoing involvement in partnership decisions and potential conflicts can create management burdens.

FAQs

How Much Money Do I Need to Invest to Make $3,000 a Month?

To earn $3,000 monthly in passive income, you need approximately $257,000 to $360,000 invested, depending on your annual return rate.

- 10% annual return: $360,000 invested

- 12% annual return: $300,000 invested

- 14% annual return: $257,143 invested

Constitution Lending makes this goal more achievable through high-yield real estate debt. With our 10% to 14% returns and $1,000 minimum investment, you can build toward a $3,000 monthly income through fractional loan investments.

How Does Passive Real Estate Investing Compare with Investing in REITs?

Real estate debt investing typically offers higher returns and more control than REITs, while maintaining similar levels of passiveness.

Real Estate Debt vs. REITs Comparison

Constitution Lending's real estate debt investments offer REIT-level passiveness with significantly higher returns. You choose which loans to fund while we handle all borrower relationships and loan servicing.

What is the Main Difference Between Passive Income and a Side Hustle?

Passive income requires minimal ongoing effort after the initial investment, while side hustles demand continuous time and active work to generate money.

Key differences:

- Time commitment: Passive income works without your presence; side hustles require active participation

- Scalability: Passive investments can grow without additional time; side hustles trade time for money

- Initial setup: Passive income needs upfront capital; side hustles often require ongoing effort

Constitution Lending's real estate loans provide true passive income. After investing, you receive monthly payments automatically without any additional work, unlike side hustles that require constant effort.

Is it Actually Possible to Have Passive Income Through Investment Properties?

Traditional rental properties require significant active management despite being marketed as "passive." True passiveness comes from real estate debt investments, where you earn returns without property ownership responsibilities.

Rental property reality check:

- Tenant screening and management

- Maintenance and repair coordination

- Vacancy periods and marketing

- Property taxes and insurance management

Real estate debt eliminates these issues by positioning you as the lender, not the property owner. Constitution Lending handles all loan origination, servicing, and borrower management, delivering truly passive returns of 10% to 14%.

What Is a Real Estate Investment Trust (REIT)?

A REIT is a company that owns, operates, or finances income-producing real estate. Investors buy REIT shares and earn dividends from the underlying property income, similar to owning stock in a real estate portfolio.

REIT limitations:

- Lower returns (typically 3% to 8%)

- No investment control or transparency

- Market volatility affects share prices

- Management fees reduce returns

Constitution Lending offers an alternative to REITs through direct real estate debt investments. You earn 10% to 14% returns with full transparency into each loan's details, borrower profile, and underlying property.

What are the Best Real Estate Investment Strategies for Generating Passive Income?

The most effective passive real estate strategies balance high returns with minimal management requirements:

1. Real Estate Debt Investing

- Returns: 10% to 14% annually

- Minimum: $1,000 with Constitution Lending

- Management: Completely passive

- Risk Tolerance: Low (first lien position, payment guarantees)

2. Real Estate Crowdfunding Platforms

- Returns: 6% to 12% annually

- Minimum: $1,000 to $10,000

- Management: Passive

- Risk Tolerance: Moderate (equity investments)

3. Publicly Traded REITs

- Returns: 3% to 8% annually

- Minimum: $1 (stock price)

- Management: Completely passive

- Risk: Market volatility

Constitution Lending stands out by offering the highest returns (10% to 14%) with true passiveness and strong principal protection. Our payment guarantee ensures you receive income even if borrowers default, while our first lien position protects your investment.

What is the 3-3-3 Rule in Real Estate?

The 3-3-3 rule suggests waiting at least 3 years before selling a property, ensuring you can cover 3 months of expenses, and maintaining 3% of the property value for annual maintenance costs.

Invest in High-quality Real Estate Loans with Constitution Lending

For accredited investors seeking true passive real estate income, debt investing offers the optimal combination of high returns, capital protection, liquidity, and minimal management requirements.

While other real estate investments may provide diversification benefits or higher potential returns in specific circumstances, few match the consistent income and principal protection available through high-quality real estate debt.

Constitution Lending's platform allows investors to access institutional-quality real estate loans with just $1,000, receiving monthly interest payments and full principal repayment within 6 to 18 months. Our payment guarantee feature and low LTV lending standards provide additional security rarely available in other passive real estate investments.

Start building your passive income portfolio today by opening a free investment account and exploring our current loan opportunities.