Dear Partners,

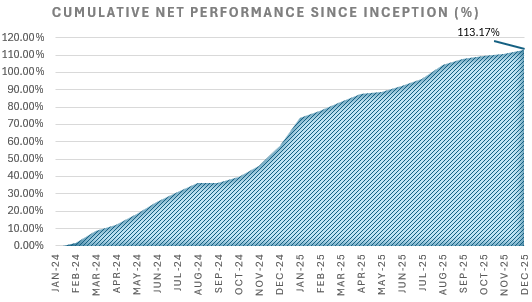

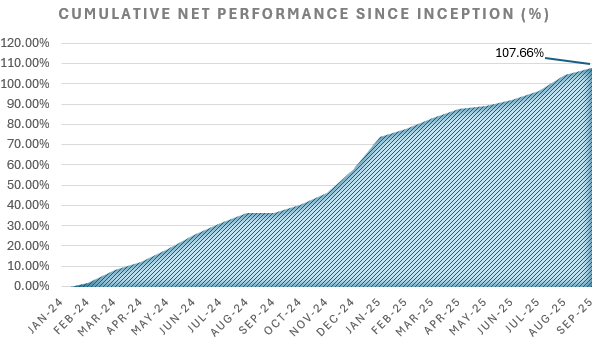

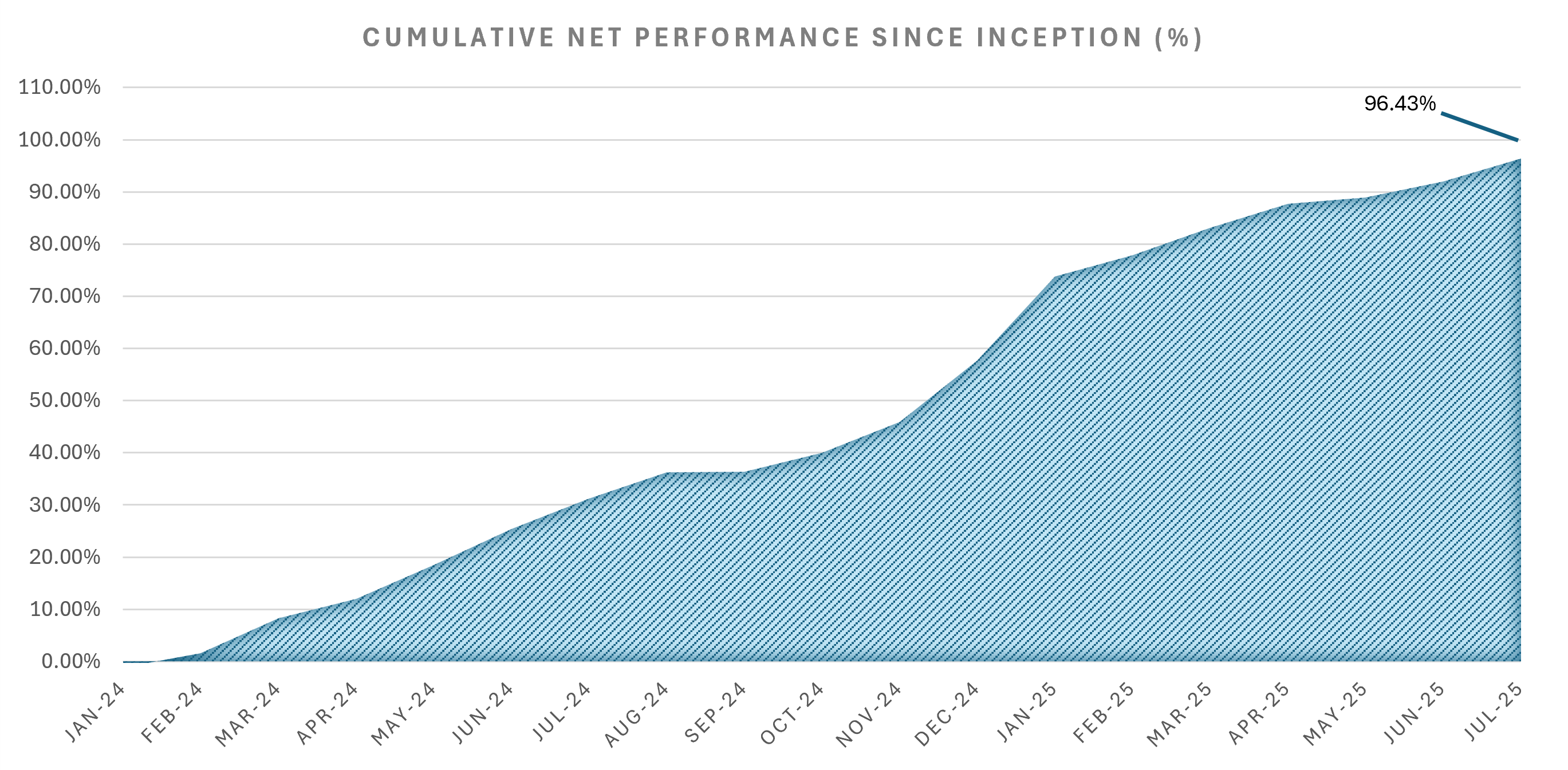

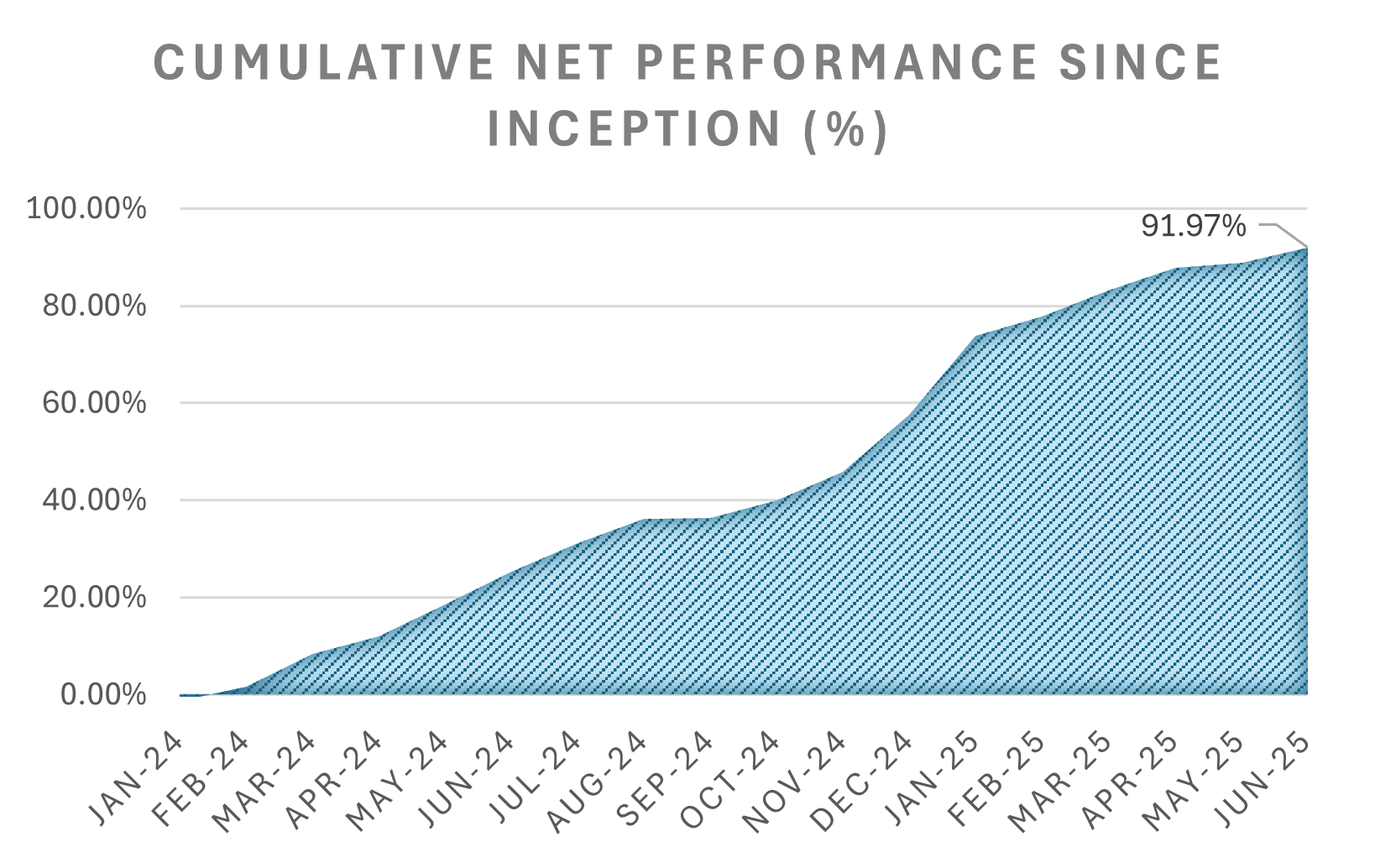

We’re excited to share details on what has been a standout inaugural year for the fund. We generated a 56.96% net return to our limited partners for calendar year 2024, including a strong 7.71% gain in December.

Market conditions have created buying opportunities in nonperforming real estate debt that few players are able to capitalize on. For the few players equipped to source, underwrite, and manage these assets, we expect the next few years to be a boon.

With lenders increasingly motivated to sell their distressed loans, we believe 2025 will present even more compelling deals. In this update, we’ll cover performance, portfolio insights, and our most investor asked questions of the year.

As a final note, the fund minimum investment is increasing from $20,000 to $100,000 starting April 1. Re-investment minimum for current investors, will remain at $10,000.

Performance

- The fund generated a net return of 56.96% for 2024 and 7.71% in Dec24

Net P/L Performance by Month Breakdown

Jan 2024

-1.21%

Feb 2024

2.85%

Mar 2024

6.59%

Apr 2024

3.38%

May 2024

5.84%

Jun 2024

5.78%

Jul 2024

4.68%

Aug 2024

3.83%

Sep 2024

0.06%

Oct 2024

2.69%

Nov 2024

4.11%

Dec 2024

7.71%

YTD

56.96%

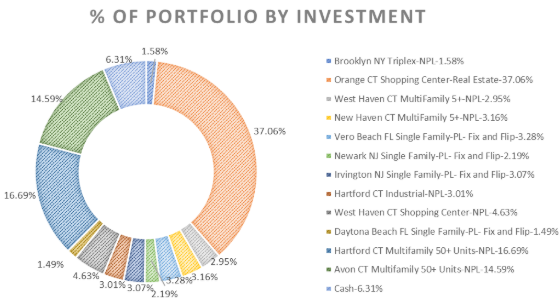

Portfolio Insights and Highlights

- The fund made 15 investments in 2024

- 4 of the investments paid off fully in 2024

- 1 of them became real estate owned by the fund, a shopping center in New Haven County, Connecticut.

- This retail deal generated $138,000+ of net income for the fund in the 2nd half of 2024. Not bad for an initial cash outlay of about 1.4mm.

- In December, a few days before year end, the fund acquired a non-performing loan on 160+ units in Hartford, Connecticut at a sizable discount to current payoff. Unpaid principal balance of about $9mm. We are very happy with this investment and are excited to see it play out in 2025.

- This deal is a good encapsulation of our edge: it was widely marketed and some expected to sell near 100% of UPB. Instead we won it for 76% and closed in 2 weeks.

Market Thoughts

- The environment for acquiring nonperforming loans remains highly favorable.

- We continue to see a growing pipeline of distressed debt hitting the market as lenders adjust to the reality of higher-for-longer interest rates.

- Many sellers who previously held out for better pricing are now recognizing the need to transact at today’s lower values rather than waiting for rate relief that may not come soon.

- This shift is creating even more opportunities to acquire loans at attractive prices, and we expect this trend to accelerate into 2025.

- Mind you, the most interesting thing relative to many other cycles where the assets themselves are in some sort of distress, the assets today (except office) are mostly fine. High occupancy, low future supply, etc..

- The problems with most distress today was driven by sponsors overpaying and overlevering in the hopes that double digit rent grow would continue and rates would stay near zero. Unfortunately for them (fortunately for us) this has not been the case.

Most asked investor questions

Fund Strategy & Performance

- How do you generate such high returns in nonperforming loans?

The fund acquires loans that have default rates of 15-24%. So as a simple example, if you buy a loan that is $100,000 that’s collateralized by a property worth $500,000 and it takes you 1 year to push the property into a sale, you would earn $18k-$24k, an 18-24% return. That’s assuming you did not pay a discount for the loan or didn’t use any leverage. We often have both.

- What is the typical timeline for resolving a nonperforming loan?

Most loans resolve within 9 months of us acquiring it. If we also have to add value to the real estate in some way, such as leasing it up or stabilizing the asset, that will typically be another 9 months but the timelines are quite varied, depending on the asset.

- How do you manage risk when purchasing nonperforming loans?

Risk management begins with disciplined underwriting—purchasing only at prices that provide sufficient collateral coverage. In addition, being an active and aggressive participant on the legal side allows us to be faster at resolution than any other lender in Connecticut. Our local legal expertise enables us to move efficiently to outcomes while managing costs effectively.

- Does this strategy scale?

Yes, we have built a systematic way to source these opportunities. Today we have more capital and a larger pipeline than we’ve seen previously

Distributions & Liquidity

- How often does the fund make distributions, and can I reinvest them?

The fund has made discretionary distributions and will transition to a quarterly schedule in 2025. Distributions remain subject to fund performance and liquidity conditions. Investors have the option to reinvest distributions to compound returns or receive cash.

- Will distributions remain discretionary, or do you plan to set a fixed schedule?

Starting in Q1 2025, we will make quarterly distributions, but they will remain subject to fund performance and available liquidity. This approach ensures that distributions align with realized returns.

Market & Deal Flow

- How has deal flow changed with higher interest rates?

Higher interest rates have placed increased pressure on borrowers and lenders, leading to a rise in distressed assets. Lenders are becoming more motivated to offload nonperforming loans as refinancing options remain limited. This environment presents attractive acquisition opportunities for the fund.

- Are you seeing better pricing on nonperforming loans now compared to last year?

Yes, we are observing more realistic pricing from sellers. While many lenders still hold out for higher recoveries, some are surrendering to sustained elevated interest rates. This shift has resulted in improved acquisition opportunities for the fund.

- What property types is the fund going for?

The fund is focusing on well-located properties where distress is driven more by financing issues than fundamental asset weakness.

Fund Operations & Growth

- How does the fund source deals, and what gives you an edge in finding opportunities?

We leverage a combination of direct lender relationships, AI, proprietary data, and market intelligence to source off-market and lightly marketed deals. Unlike funds relying solely on brokered transactions, we prioritize sourcing strategies directly to opportunities before they reach broader distribution.

- What improvements have been made this year to enhance fund operations and deal execution?

This year, we significantly enhanced our technological capabilities to accelerate deal identification and underwriting. Thanks to the amazing new capabilities of AI and our great developers, we are able to read and scrape information on every single foreclosure and/or lawsuit in the state of Connecticut. Giving us unprecedented visibility into distress in an entire state. These improvements have contributed to more efficient capital deployment and stronger overall performance.

As we close out an exceptional year, we want to thank you for your continued trust and partnership. With strong momentum entering 2025, we remain focused on capitalizing on market opportunities and delivering strong risk-adjusted returns. The current environment continues to favor disciplined buyers, and we’re well-positioned to take advantage of it. We look forward to another successful year ahead and will keep you updated on new acquisitions and fund developments. Wishing you a prosperous and rewarding year ahead.

Learn more about investing in the Constitution Real Estate Credit Fund

Yours truly,

Ricardo, Kyle, and Joe

200 Pemberwick Road

Greenwich CT 06831

Invest@ConstLending.com

203-423-3534