Dear Partners,

We are pleased to share the latest performance update for the Constitution Real Estate Credit Fund. This report highlights the fund’s performance, current market trends, and key portfolio insights.

Performance

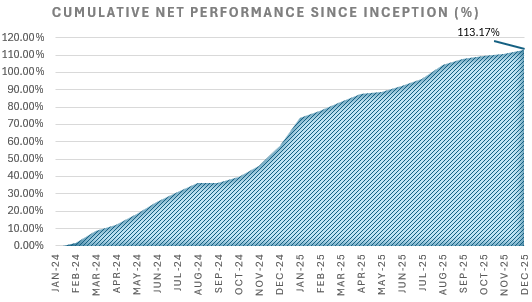

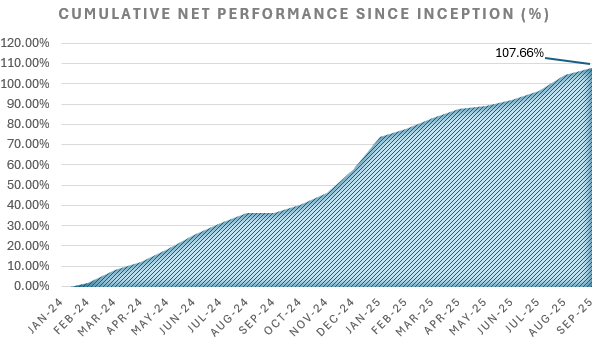

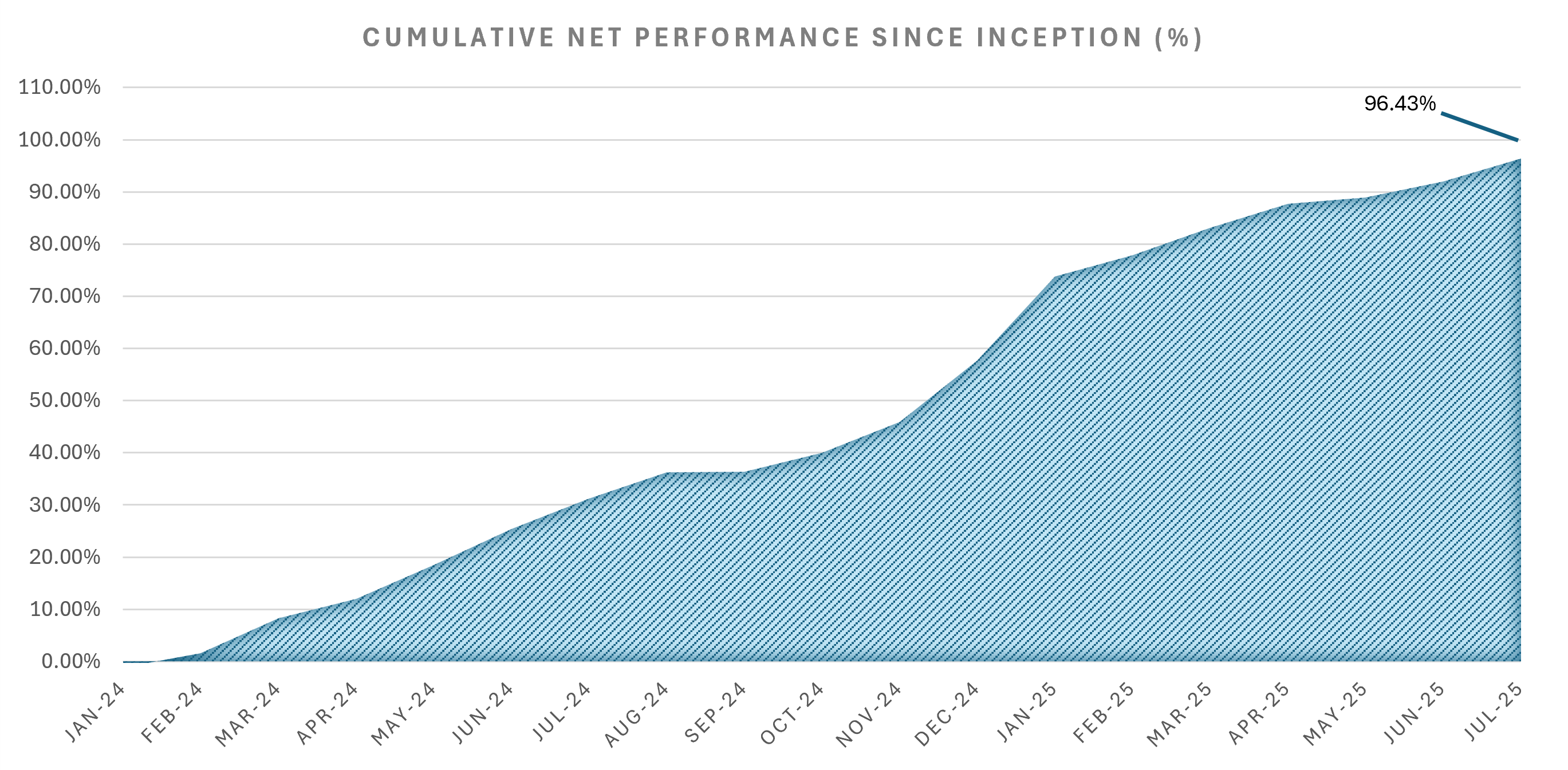

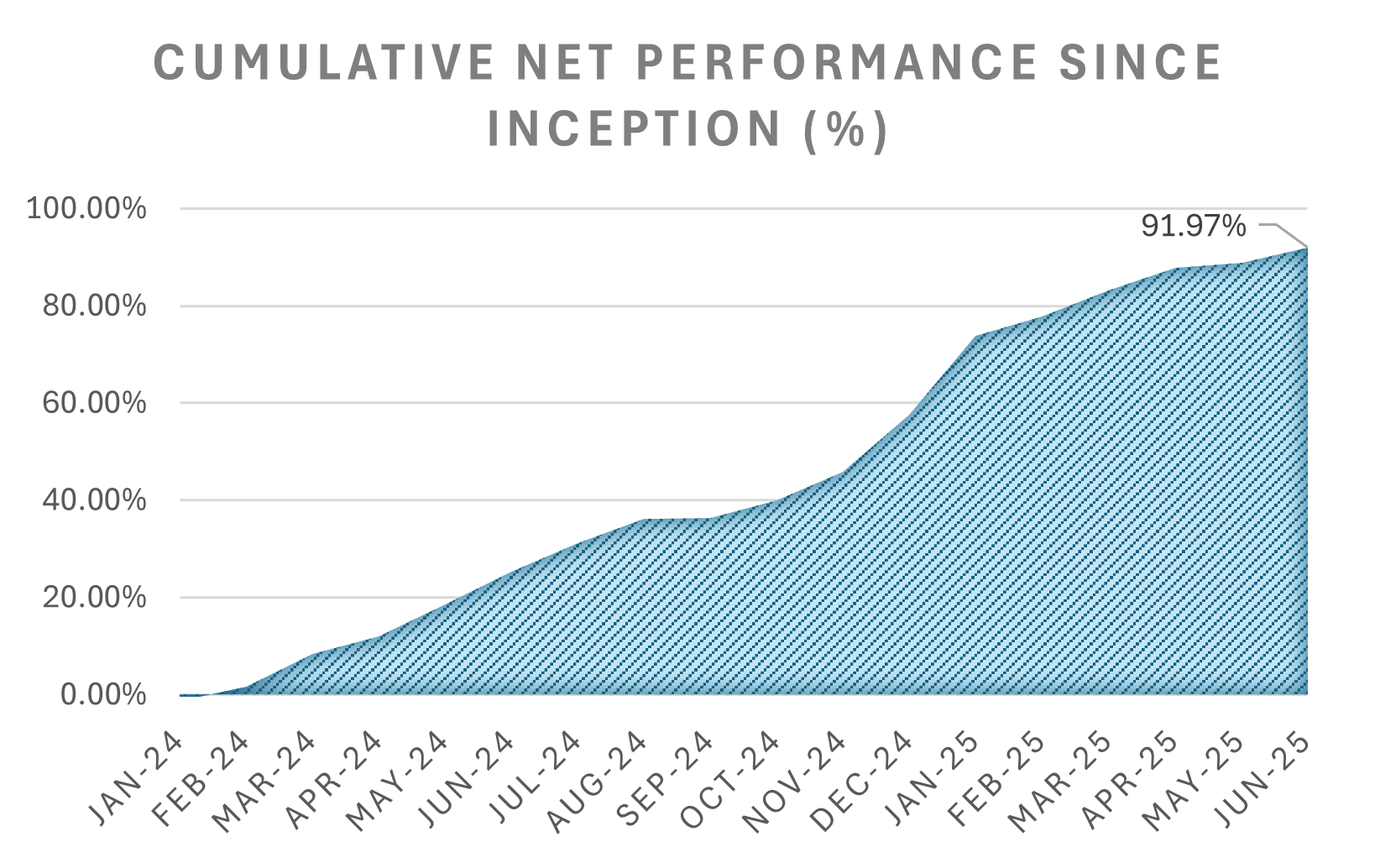

- The fund had a net return of 36.31% through September 30 2024

Net P/L Performance by Month Breakdown

Jan 2024

-1.21%

Feb 2024

2.85%

Mar 2024

6.59%

Apr 2024

3.38%

May 2024

5.84%

Jun 2024

5.78%

Jul 2024

4.68%

Aug 2024

3.83%

Sep 2024

0.07%

YTD

36.31%

Market Thoughts

Things we have been expecting and looking forward to for the last 12 months are starting to materialize. Non-bank lenders and banks are starting to sell some of the non-performing loans (still close to par of course, but progress) that 12 months ago weren’t even for sale at 100 cents. It is still the case that deals trading sub 90% of UPB have unique issue(s) that makes it harder to sell at a good price on the secondary market (either the collateral, the borrower, or both). There is now a regular flow of brokered NPL and sub-performing loan pools coming to market monthly. We view this as healthy and don’t expect it to slow down any time soon.

The regulatory scrutiny from banks feeds through to the whole system. Even with the explosion in private credit, banks still matter a lot. Some fraction of every dollar in private credit is ultimately coming from someone with a regulator who is concerned about commercial real estate. This has and will continue to create opportunities for picking up great credit at a great basis.

We’re often asked why we often pay par for NPLs. We are frequently going direct to the original lender and rarely face competition. Obviously, if a deal works at par it works at a discount. One can always angle for better pricing in theory. In practice, we are bidding against the gag reflex of some credit committee. Humans are risk seeking when it comes to loss avoidance and you can see this clearly in the intransigence of soon-to-be impaired creditors, they’d rather let their situation get worse by doing nothing than taking a loss on a loan when they should. We prefer spending our finite underwriting capacity on deals with a high likelihood of transacting.

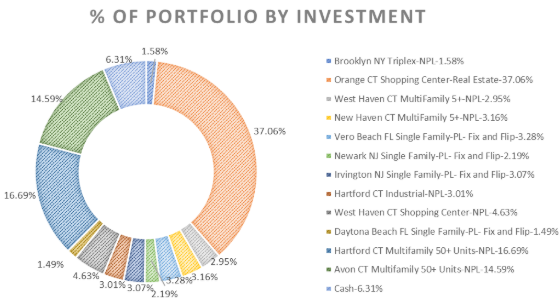

Portfolio Insights and Highlights

- Our retail deal is performing well; we have a signed LOI for a ground lease with a national coffee drive through franchise; should be executing the lease before the end of November.

- The retail deal also caught a lucky break: we were made aware that the previous owners had started the tax appeal process before we took title. This means we will get a credit for the 2023 Grand List taxes and the full 5 years of benefit from the appeal since the town did their re-valuation in 2023.

- We have also bought a couple more small NPLs in the fund in the 45% LTV range as those can accrue safely at 18-24% rate while they slowly get paid off.

- Fund is under contract for buying our first judgment lien that came about from a slip and fall suit. That judgment is collateralized by a 20,000 sqft retail where the defendant is not-appearing. We estimate LTV on this to be below 50%.

- We continue to look for credit opportunities on the secondary market that provide a healthy risk-adjusted return. If you know any lenders/banks looking to sell notes, please reach out.

- Additionally, we are looking for institutional capital sources to partner with on some of our pipeline opportunities that are beyond our reach today for capacity reasons.

Pipeline Update

- A couple of deals we have been working on since Q1 are showing signs of life. This is part of the long life cycle of acquiring NPLs. It can take months from the time you spot the opportunity to be able to convince the current lender it’s in their best interest to sell the loan

- We are underwriting a fully occupied medical office non-performing loan

- We have a 28mm non-performing multifamily loan under contract that will be seller financed by the bank we’re purchasing it from

General Company Updates

- As the fund grows we are growing too! In September we closed on the acquisition of a 45,000 square foot office building in Greenwich, Connecticut that will be our new corporate office. If you are in town feel free to stop by and say hi!

- We took on a couple of college seniors for academic year internships with the intention of hiring them full time upon graduation next spring. One of our bigger issues we’ve had recently is we are seeing more opportunities in the distressed space than we have the ability to chase down and underwrite. We aim to be able to use our new analysts to be able to truly use all of the data and information and opportunities that we see in the market.

- That judgment lien that originally came from a slip and fall mentioned earlier, was found by our data, but chased down by one of our new analysts!

- As we move into the fourth quarter of our funds first year, we want to extend our sincerest thanks for your support. Looking forward to closing the year out with a strong final quarter!

Learn more about investing in the Constitution Real Estate Credit Fund

Yours truly,

Ricardo, Kyle, and Joe

200 Pemberwick Rd, Greenwich CT 06831