Dear Partners,

Please find below an overview of the fund’s performance year-to-date and our thoughts on the market environment as we move into the second half.

Performance

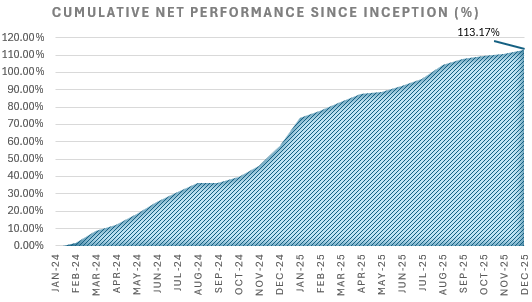

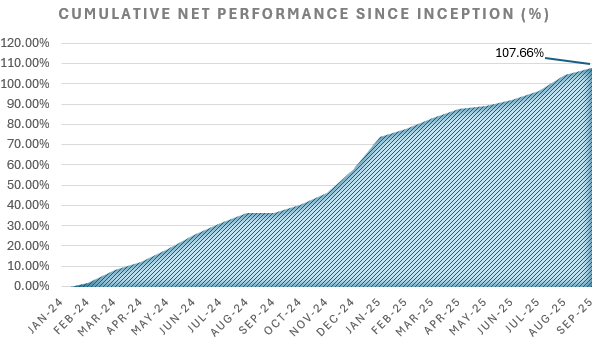

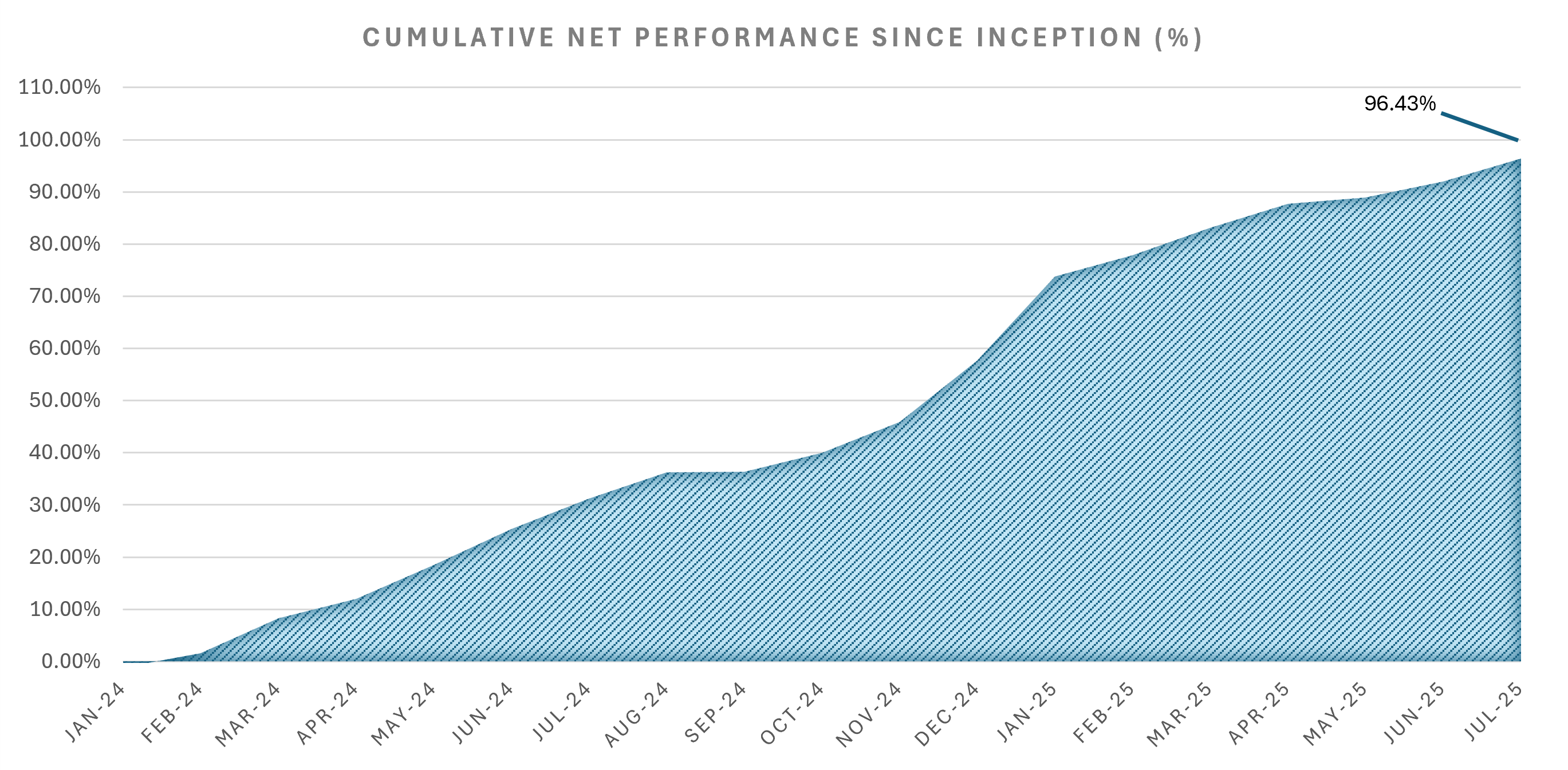

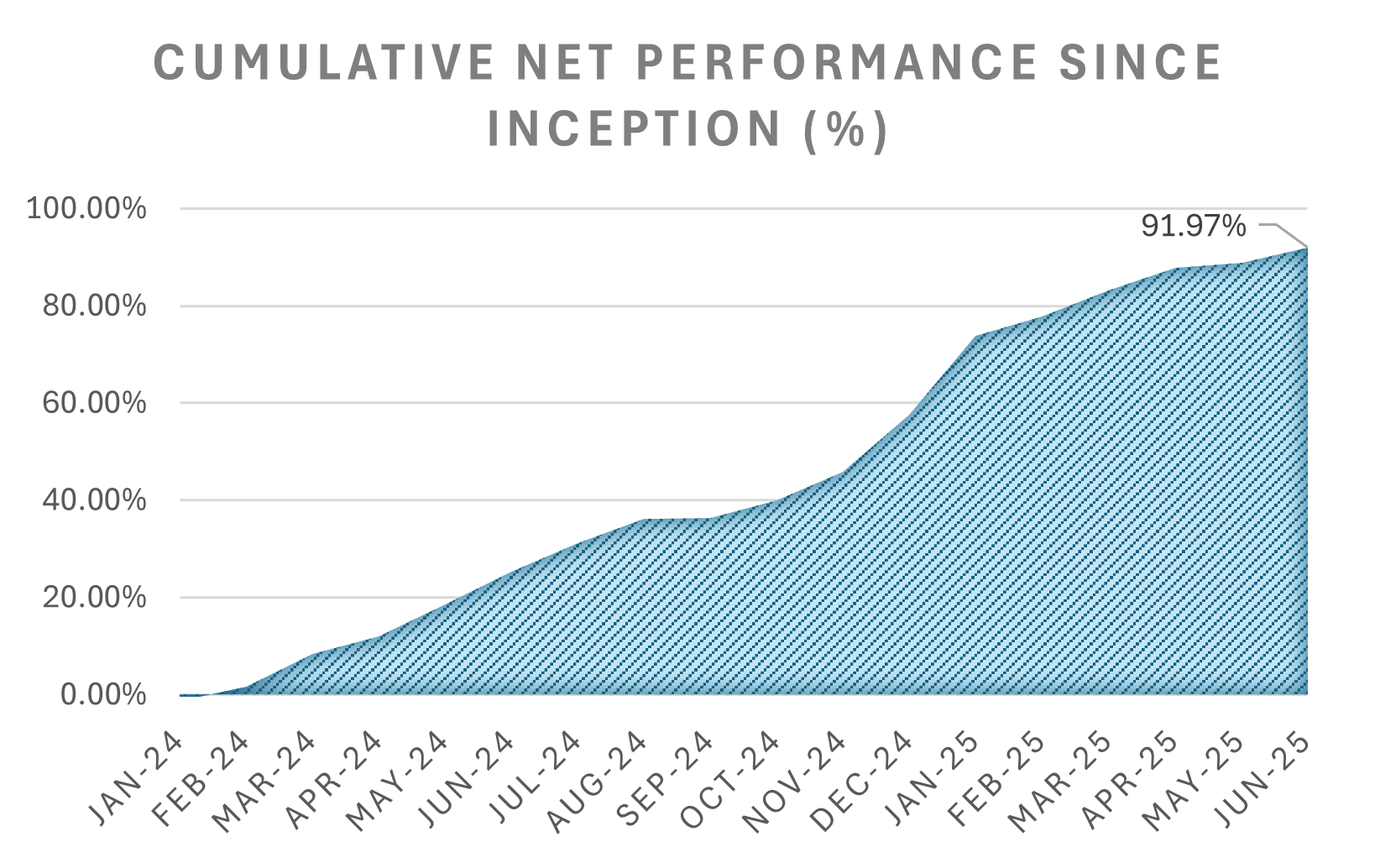

- The fund had a net return of 25.33% through the second quarter of 2024

Net P/L Performance by Month Breakdown

Jan 2024

-1.21%

Feb 2024

2.85%

Mar 2024

6.59%

Apr 2024

3.38%

May 2024

5.84%

Jun 2024

5.78%

YTD

25.33%

Market Thoughts - “Pretend and Extend” becomes “Admit and Split”

Since the rates selloff began in 2022, market participants have been predicting a commercial real estate firesale. While equity players wait for this other shoe to drop, we are seeing signs of surrender on the credit side.

The market view for all of last year was that the “distress” would be pretended and extended away. A lot has changed, even compared with just 6 months ago. We have heard from borrowers, banks, and credit lines that now loan docs matter; a borrower in default (even non-monetary) will not be able to extend. This is a stance that was laughable even as recently as Q1. The FDIC is the alleged cause for this conservatism as they are now reading loan docs and taking non-monetary defaults seriously.

Here are some of the things we’re seeing that make us think the credit capitulation is upon us:

- Bridge lenders unable to extend non-monetary defaulted borrowers

- Banks looking to sell non-monetary defaulted loans (although still at par)

- Bridge lenders transacting in low 90c of principal for sub 70% LTV loans

- Credit lines forcing their lenders to sell or buyout maturing loans instead of extending

- General desired transaction speed; we were asked by a lender to close in 2 weeks when in q1 or before, this lender had told us they had no interest in selling any loans

As we survey the market and our pipeline, we are bullish on the opportunity set. There are now and will continue to be many maturity defaulted loans that cannot be refinanced without a significant capital injection to pay down the loan. Indeed, even selling in some cases will be challenging without marking the equity to zero. Despite the capital stack issues, rents in our markets continue to climb and vacancy remains low for all non-office asset classes. It is the perfect storm of debt driven liquidity squeezes on quality collateral and we’re excited to continue taking advantage of these tailwinds.

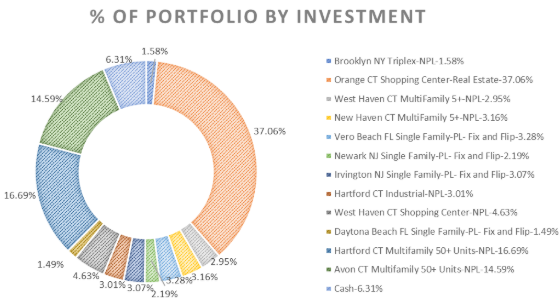

Portfolio Insights and Highlights

- 3 non-performing loans paid off in Q2. We ended up owning them for an average of about 80 days, which is a shorter life cycle than usual for an NPL, but we were glad to get the capital back for reinvestment.

- In May, we closed our largest fund NPL acquisition to date, details below:

Collateral Location: Orange, Connecticut

Collateral Type: Multi-Tenant Retail

Purchase Price: 4.18mm

Est. As-is Collateral Value: 5.35mm

Est. Stabilized Collateral Value: >7.50mm

Timeframe: 12-15 months from loan purchase

- The loan was purchased at a substantial discount to payoff amount and also current and potential property value. We are ahead of schedule, having negotiated a consensual foreclosure with the borrower. This will likely allow us to begin any required renovations and leasing in the next couple of months and have a fully stabilized shopping center within 15 months of purchasing the loan.

- We continue to look for credit opportunities on the secondary market that provide a healthy risk-adjusted return. If you know any lenders/banks looking to sell notes, please reach out.

- Additionally, we are looking for institutional capital sources to partner with on some of our pipeline opportunities that are beyond our reach today for capacity reasons

Learn more about investing in the Constitution Real Estate Credit Fund

Yours truly,

Ricardo, Kyle, and Joe

500 Post Road East, Westport CT 06880

Invest@ConstLending.com

203-423-3534