From our conversations with investors, three main reasons come up when people look for Arrived Homes alternatives:

- Low returns: According to Arrived's own financial performance reports, investors earned an average annualized return of 4%, and vacation rental homes earned an average of 2.4%. For context, total market-weighted index funds and REITs (real estate investment trusts) have historically returned around 10%.

- Long holding periods: Arrived Homes investments carry holding periods of 5 to 7 years, and exiting your position before the property is sold comes with fees and penalties. This makes them extremely illiquid because your capital is effectively locked up for almost a decade, with limited options to access it early.

- Limited downside protection: With Arrived Homes, you invest in real estate itself rather than the debt that secures it. This exposes you to market downturns because debt investors are paid first and in full from any sale. Equity investors receive only what remains after all debts are settled, so a decline in property values affects you first.

A strong alternative to Arrived Homes should address all three of these limitations. It should offer higher annualized returns, a shorter investment horizon, and a debt-based structure that protects your principal from market volatility.

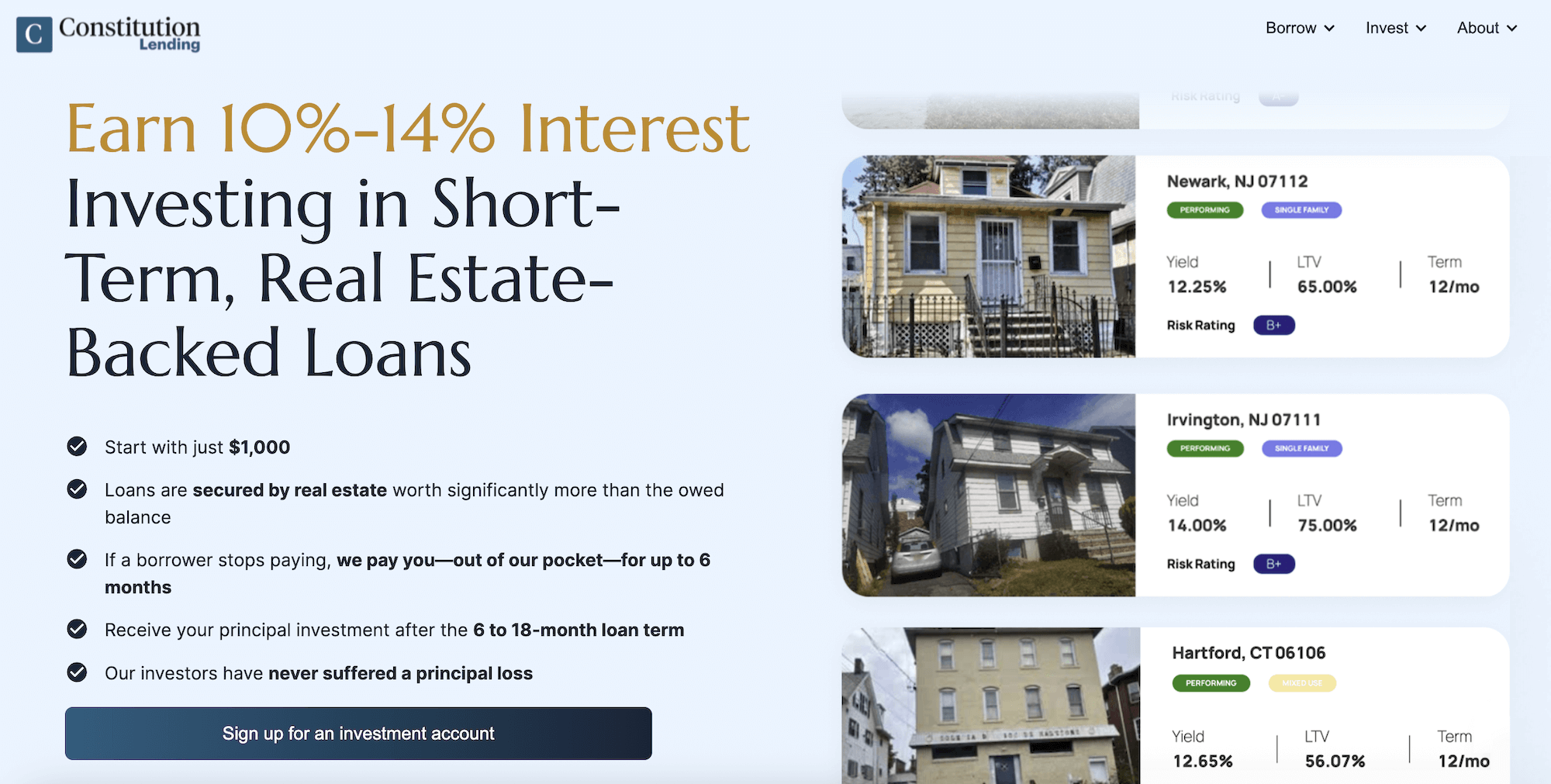

In this article, we cover the best Arrived Homes alternatives evaluated against those three factors. We start with ourselves, Constitution Lending, and how our real estate debt investment platform allows investors to earn 10% to 14% annually, receive their principal investment in 6 to 12 months, and benefit from stronger capital protection.

We also cover a few other alternatives worth considering.

Sign up for a free investment account here and browse through our debt investment options.

1. Constitution Lending: Earn 10% to 14% Interest Returns Investing in Hard Money Loans

Constitution Lending is a private lender that originates hard money loans for real estate investors. This includes fix-and-flip, bridge, and construction loans on residential and multifamily properties.

Via our investment platform, retail investors can purchase fractional shares in the loans we originate, starting with just $1,000, and earn monthly interest payments from borrowers ranging from 10% to 14%. You can also invest through an IRA to take advantage of tax-advantaged compounding on your returns.

This is slightly different from what Arrived Homes does because you aren't investing directly in rental homes or residential properties. Instead, you're investing in the loan used to purchase or renovate the property. (We cover the benefits of this distinction in more detail below.)

Earn 10% to 14% Interest From Borrowers

The reason our borrowers pay 10% to 14% interest rates comes down to closing speed. We close loans in 7 to 14 days, while traditional banks typically take 30 to 60 days. For a real estate investor moving quickly on a deal, that speed is worth the premium.

This means our investors earn 10% to 14% annually in interest payments from borrowers, which is more than double the 2.4% to 4% of Arrived Homes, with no property management responsibilities, closing costs, or tenant headaches to deal with.

Every loan on our platform also comes with a payment guarantee, which acts as insurance in case a borrower defaults. If that happens, we pay you up to 6 months of interest payments while resolving the situation, whether that's a foreclosure, short sale, or loan modification.

In practice, this guarantee is rarely needed. Our borrower default rate is under 2%, compared to a national average of around 4%. That’s because we lend exclusively to high-quality, experienced real estate professionals with strong track records and low loan-to-value ratios.

Read more: How to Invest in Hard Money Loans: A Comprehensive Guide

Get Your Full Principal Investment Back in 6 to 12 Months, Not 5 to 7 Years

Hard money loans on our platform have terms of 6 to 12 months. At the end of the term, the borrower either sells the property and uses the proceeds to repay the loan in full or refinances into a longer-term loan. Either way, you receive your entire principal investment back at that point.

From here, you can choose to reinvest in more loans, diversify into other property investments, or simply withdraw your capital. Unlike Arrived Homes, where your investment strategy is locked in for years, Constitution Lending gives you full flexibility at the end of every loan term.

Compare that to Arrived Homes, where your capital is tied up for 5 to 7 years while you wait for the platform to sell the underlying rental homes or vacation rentals.

Stronger Capital Protection by Investing in Real Estate Debt

Arrived Homes offers little protection from market downturns because you own equity in the property itself. When the property is sold, debtors are paid first and in full from the proceeds of the sale. You only receive what remains after all debts are settled.

In a market downturn, that payment order exposes you to losses in the property's value.

For example, say you invest in a property on Arrived Homes worth $1 million. Of that $1 million, $250,000 comes from investors like you, and $750,000 is financed by a lender. If the property's value falls to $750,000 during a downturn, the lender recovers their $750,000 investment and equity investors lose their $250,000.

When you invest in real estate debt through Constitution Lending, the dynamic flips entirely in your favor. You are the debtor, which means you are paid first and in full from any proceeds of a sale. The borrower's equity is what absorbs losses in the property's value. The borrower has to lose their entire equity investment before your principal is affected.

Staying with the example above, say you invest in a $750,000 loan on a property worth $1 million. The borrower has $250,000 in equity. If the property's value falls to $750,000, the borrower loses their $250,000 equity stake, and you still recover your $750,000 principal.

For greater principal protection, we only originate loans in which the outstanding balance doesn't exceed 75% of the property's value. That means every loan on our platform comes with a built-in 25% equity cushion from the borrower. A property would have to lose more than 25% of its value before your principal is at any risk.

Thanks to this structure, our investors have never experienced a principal loss.

Additional Benefits of Investing with Constitution Lending

Low Borrower Default Rate

As we touched on earlier, our borrower default rate is under 2%, compared to a national average of around 4%.

This is not by chance. We lend exclusively to high-quality, experienced real estate professionals, including seasoned flippers, construction companies, and rental investors with proven track records.

Over the years, we have built a deep network of these borrowers across residential and multifamily property investments, and we know their performance history firsthand. We apply strict underwriting standards on every loan, including minimum credit requirements and low loan-to-value ratios, so the borrowers on our platform are among the most qualified in the country.

Read more: How to Buy Mortgage Notes with as Little as $1,000

We Offer a Payment Guarantee on Every Loan

Every loan on our platform comes with a payment guarantee that automatically activates if a borrower misses a payment.

We pay your monthly interest payments out of our own pocket for up to 6 months. During that time, we work to either get the borrower back on track or foreclose on and liquidate the underlying property, using the sale proceeds to return your full principal and any accrued interest.

No other real estate investment platform we are aware of offers this level of protection.

That said, as we mentioned earlier, our payment guarantee is rarely needed given the quality of our borrower network and our default rate of under 2%.

We Invest Alongside You

Most real estate investment platforms pool investor capital, deploy it across deals, and collect asset management fees regardless of how those deals perform.

Their money is not in the same investments as yours, which means their financial incentives do not fully align with yours when it comes to protecting principal and generating returns. They make money regardless of whether your loan performs.

At Constitution Lending, we originate every loan on our platform using our own capital and maintain a 50% or greater stake in each loan for the entire term.

Our money is in the same deals as yours from start to finish. If a loan performs poorly, we feel it just as much as you do. That alignment gives you confidence that every loan we put on our platform has been underwritten to a high-quality standard we are personally comfortable with.

How to Start Investing with Constitution Lending

Getting started takes less than five minutes, and you can browse our available loan offerings before making a financial commitment.

- Open a free Constitution Lending by entering your name and email address. No accreditation requirement or minimum deposit needed to open your account.

- Browse available loans on your dashboard. Every active loan on our platform is listed with the key details you need to evaluate it. This includes property address, loan amount, loan-to-value ratio, borrower credit profile, projected yield, loan term, and our internal risk rating.

- Click into any loan that interests you to access the full deal summary, including the remaining loan balance, current and after-repair property value, the borrower's track record, and the planned exit strategy.

- Link your funding source. Connect a bank account or an IRA to your Constitution Lending wallet. Both standard bank transfers and IRA contributions are accepted, so you can invest within a tax-advantaged account if that fits your investment strategy.

- Fund your first loan by clicking the Fund This Loan button, entering your investment amount, and confirming. The minimum is only $1,000, so you can spread your capital across multiple loans for diversification across different borrowers, property types, and markets.

- Collect monthly interest payments from borrowers on the first of every month. When the loan term ends and the borrower repays, your full principal is returned and you decide what to do next — reinvest, diversify, or withdraw.

Start Investing In Constitution Lending Real Estate Loans with as Little as $1,000

Sign up for an investor’s account here and search through our commercial real estate investment opportunities.

2. Willow Wealth (formerly Yieldstreet)

Willow Wealth, formerly Yieldstreet, is an alternative investment platform offering access to private market opportunities across real estate, private credit, art, and other asset classes.

Their Alternative Income Fund is open to non-accredited investors with a $10,000 minimum, while individual deal offerings require $10,000 to $25,000 and are limited to accredited investors. Investors can also access Willow Wealth through an IRA for tax-advantaged investing.

While they can be an option for those looking to purchase fractional real estate and earn passive income, we feel it’s important to point out that returns are lower than they appear.

Since inception, they've claimed a net annualized return of 9.6%, but this figure excludes active and defaulted investments. A CNBC investigation found that investors lost at least $78 million across 30 real estate deals, with four resulting in total losses and 23 more placed on an internal watchlist. The platform's annualized real estate return chart, which showed approximately negative 2% since 2015, was removed from their website shortly after the investigation was published.

Borrower and sponsor quality is also a concern. As of December 31, 2024, 2.7% of their offerings have defaulted, and an additional 4.3% have a modified outlook. Unlike Constitution Lending, which lends exclusively to high-quality, experienced real estate professionals, they deploy capital across a wide range of asset classes and sponsors with varying levels of quality control.

Finally, downside protection is limited. Willow Wealth does not offer a payment guarantee, most investments carry multi-year holding periods with limited liquidity, and if a deal defaults, investors have no income protection while waiting for resolution.

3. Groundfloor

Groundfloor is a real estate debt platform that originates short-term loans for residential fix-and-flip and construction projects, then allows retail investors to purchase fractional shares in those loans starting with as little as $10.

On the surface, this model is similar to Constitution Lending's. The differences become apparent when you look more closely at borrower quality, platform stability, and downside protection.

Advertised returns do not reflect actual investor experience. Groundfloor advertises average historical returns of 10%, but their own website includes a disclaimer stating this figure is calculated before losses. Once defaults are factored in, real investor experiences suggest actual annualized returns land closer to 3% to 5%.

Groundfloor’s default rate is high, and borrower quality is the root cause. Groundfloor's own published data puts their uncured default rate at 4.71%, and some investors with diversified portfolios spanning A through D risk grades have reported default rates as high as 12%. That’s because Groundfloor lends to a wide pool of borrowers, including first-time flippers and higher-risk property investments.

Constitution Lending, on the other hand, lends exclusively to high-quality, experienced real estate professionals with proven track records.

There are also no payment protections for investors. If a borrower defaults, investors stop receiving interest and must wait for foreclosure to resolve.

4. Fundrise

Fundrise is one of the largest real estate crowdfunding platforms in the country, offering both accredited and non-accredited investors access to diversified real estate portfolios through their eREITs and interval funds.

Minimum investments start at $10; investors can contribute through an IRA, and Fundrise charges low fees with an annual management fee of just 0.15%. Their portfolio spans multifamily properties, single-family rental homes, commercial real estate, and vacation rentals across multiple markets.

Fundrise is one of the most established and financially stable platforms in the real estate crowdfunding space, with over $7 billion in assets under management. Platform risk is not a meaningful concern here.

That said, Fundrise returns have been modest. Fundrise's Flagship Real Estate Fund has generated annualized returns of approximately 4.3% since inception, below Constitution Lending's 10% to 14% and the historical average for total market cap index funds.

The most significant limitation is downside protection. Fundrise investors own equity positions in private real estate and are paid last from any property sale proceeds. Most funds carry multi-year holding periods with limited early redemption options, and there is no payment guarantee protecting income during periods of underperformance. Platforms like EquityMultiple and RealtyMogul offer similar equity-based structures with comparable limitations.

5. Roofstock

Roofstock is an online marketplace that allows investors to purchase single-family rental homes outright or through their fractional ownership program, Roofstock One.

The platform provides detailed property financials, inspection reports, and tenant information to help investors do their due diligence on individual properties before committing capital. Unlike Fundrise or Arrived Homes, Roofstock gives investors direct control over which individual properties they invest in and which markets they want exposure to.

Rental yields typically average between 3% and 8% annually. However, investors are also responsible for property management costs and closing costs on each transaction, which can reduce net returns.

With over $365 million raised from institutional investors and a large, established marketplace, platform risk is not a meaningful concern for Roofstock, compared to some of the smaller and newer platforms.

The main limitation is the lack of downside protection. Roofstock investors own rental properties directly and are last in line on any sale proceeds after all debt is satisfied. Exiting an investment also requires going through a full property listing and sale process, which can take months depending on real estate market conditions.