A high-quality Crowd Street alternative should tick the following boxes:

- They should invest alongside you. Crowd Street connects investors with third-party sponsors and collects listing fees, but does not invest its own capital in the deals it promotes. This misalignment of financial incentives has allowed low-quality investment options to accumulate on the platform, as Crowd Street has no financial skin in the game.

- They should offer more downside protection. Crowd Street deals are structured as equity positions, so investors are paid last from the sales proceeds, leaving them more exposed to market downturns. For example, if a $1 million property carries $750,000 in debt and $250,000 in investor equity, a 25% drop in property value wipes out the entire equity investment while debtors recover every dollar.

- They should offer more liquidity. Crowd Street deals typically have holding periods of 3 to 5 years with no secondary market or liquidity options. If your financial situation changes or market conditions deteriorate, there is no practical way to exit early.

- They should have a low minimum investment requirement. You need at least $25,000 to invest in Crowd Street deals. If you want to diversify across multiple real estate properties rather than concentrating a large amount in a single deal, that threshold is a meaningful barrier. This is especially true for beginner investors who are just starting to build a real estate portfolio.

In this article, we cover the best Crowd Street alternatives evaluated against these four factors.

We start with Constitution Lending, our real estate investing platform, and how we fulfill the four criteria above. Finally, we cover additional alternatives you may come across while researching your options.

Create a free investment account to explore our available real estate loans and get started with just $1,000.

1. Constitution Lending: A Real Estate Debt Platform That Invests Alongside You

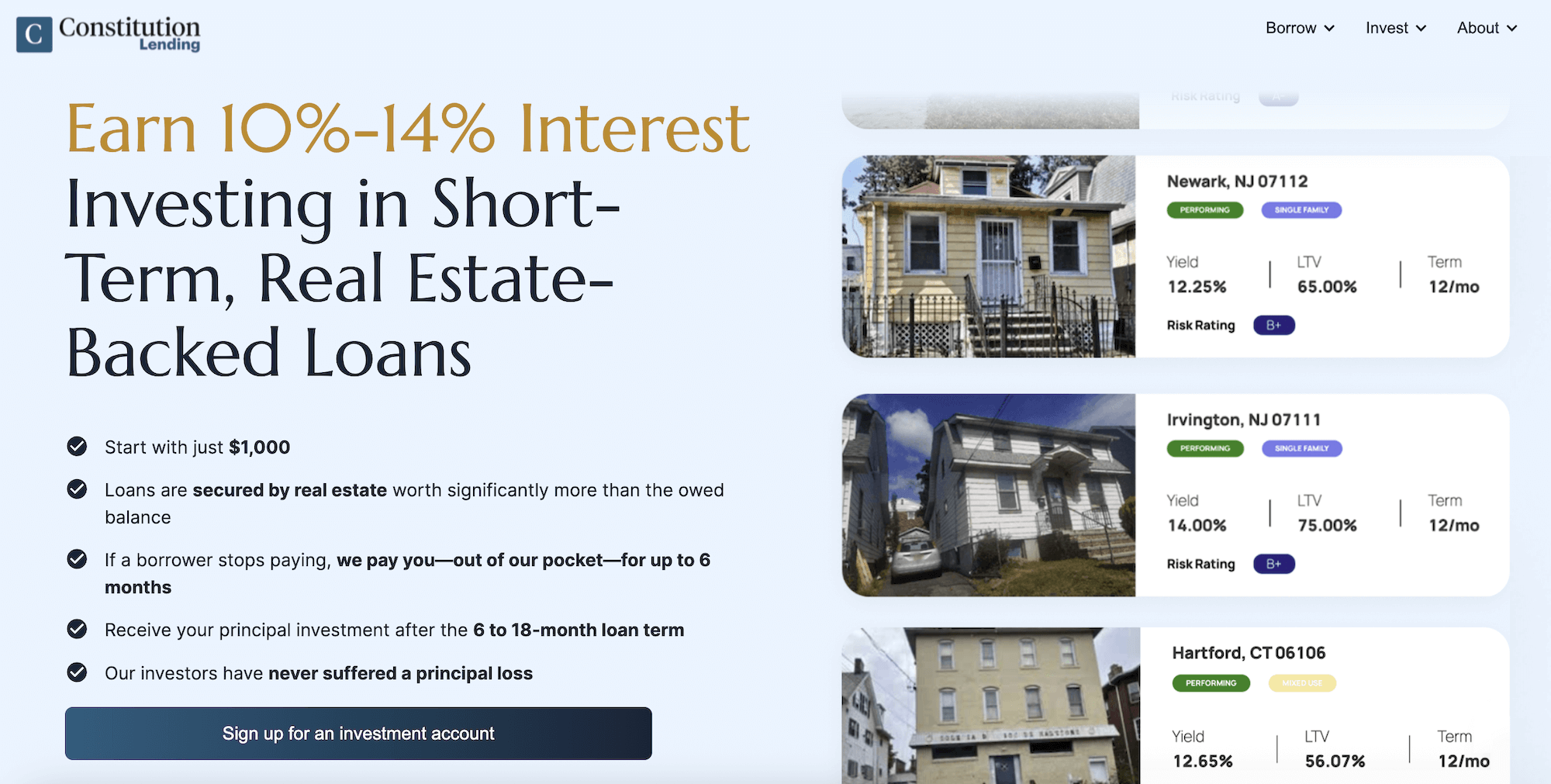

Constitution Lending is a direct private lender that originates hard money loans for real estate investors across the U.S., including fix-and-flip, bridge, and construction loans on residential and commercial real estate properties.

Using our investment platform, retail investors can purchase fractional shares in our loans starting with as little as $1,000 and earn high-yield interest payments from borrowers ranging from 10% to 14%.

Unlike Crowd Street, Constitution Lending lets you invest in the debt securing the property, not the property itself, and you do so alongside a lender that has its own money in every deal. We cover exactly what that means for you in the sections below.

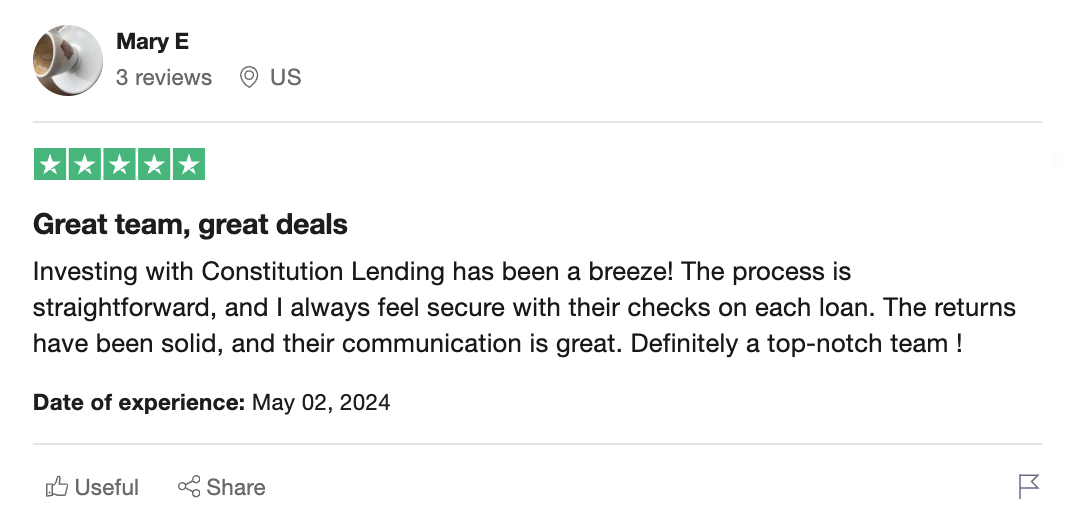

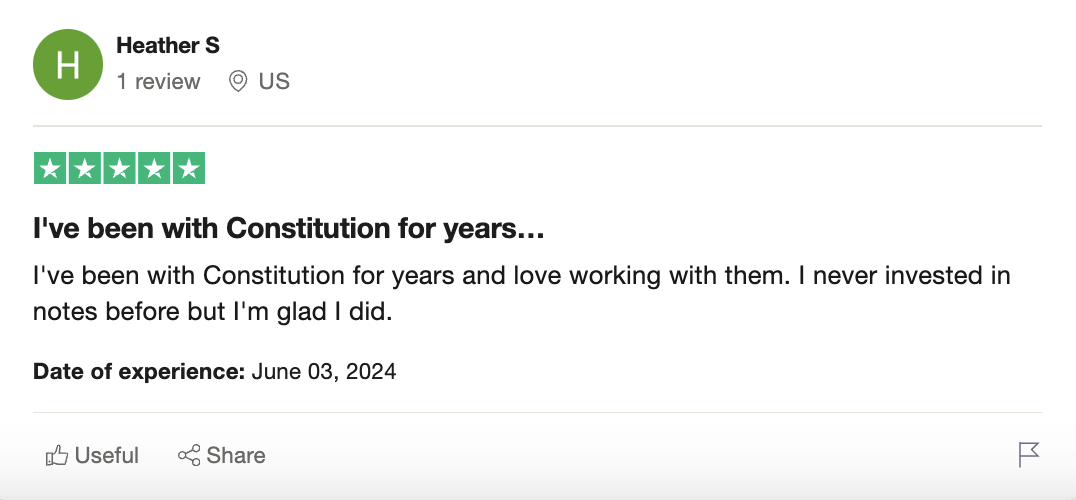

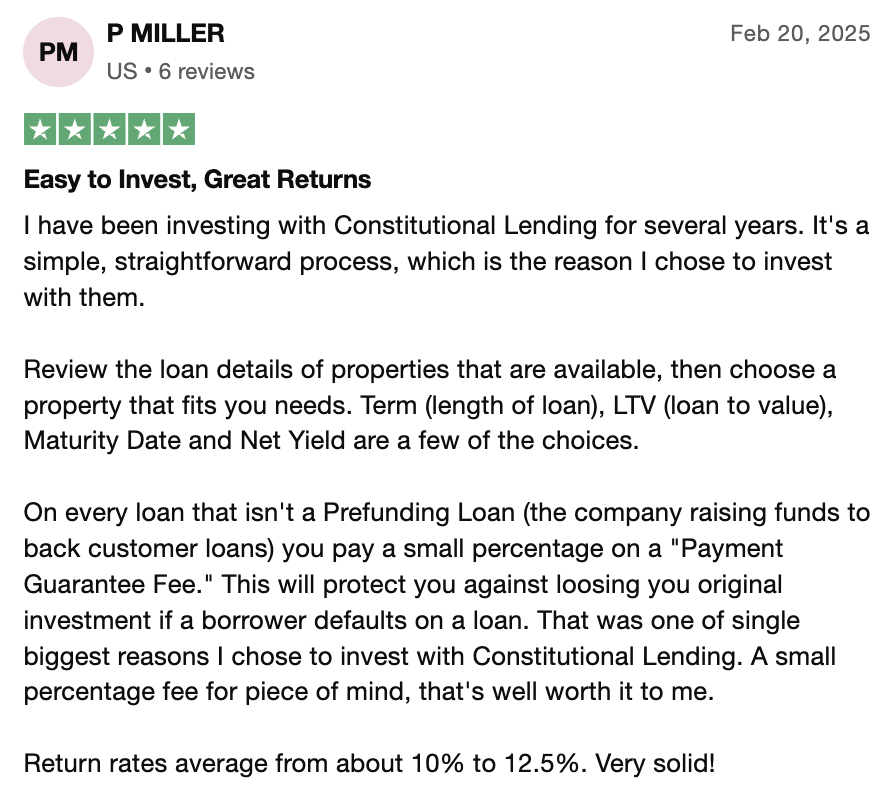

Here's what our investors say about our debt investing options:

We Invest Alongside You on Every Deal

As we mentioned above, Crowd Street operates as a marketplace. It identifies sponsors, lists their deals on the platform, and earns commissions and listing fees. Crowd Street has no financial stake in whether the deal performs. Your money is in the deal and not theirs.

This fee-based model incentivizes them to maximize the number of deals listed, often at the expense of quality. This leaves the platform littered with poor investment options. There is no vetting process strong enough to compensate for the fact that the platform itself has nothing to lose if a deal fails.

This problem became apparent during the Nightingale scandal, in which a sponsor misappropriated tens of millions of dollars in investor funds across multiple deals.

Constitution Lending operates on an entirely different business model. We originate every loan on our platform using our own capital and maintain a 50% or greater stake for the entire term. When you invest with Constitution Lending, we are in that same loan alongside you from the day it is funded to the day it is repaid.

That co-investment model aligns our financial incentives. We must underwrite deals conservatively, flag problems early, and cannot afford to put bad deals on our platform because our capital is at stake alongside yours.

Your Capital is Protected Against Market Downturns

Crowd Street investors take equity positions in commercial real estate investment projects. When the property is sold, they get paid last after all debt obligations have been satisfied, leaving them more exposed to market downturns.

For example, say you invest in a Crowd Street deal involving a $1 million commercial property. The deal is structured with $750,000 in debt and $250,000 in equity from investors like you. If the property can only sell for $750,000 during a market downturn, the debt holders recover their investment, and you take the hit.

When you invest with Constitution Lending, you are on the other side of that equation because you hold the real estate debt. You are paid first and in full from the sale proceeds before the borrower receives a cent. The borrower has to lose their entire equity investment before your principal is affected.

Using the same example, if you invest in a $750,000 loan on a $1 million property, the borrower has $250,000 in equity. The property's value can fall to $750,000, and you can still recover your full $750,000 principal without losing a cent.

For additional protection, we only originate loans where the balance doesn't exceed 75% of the underlying property's value. That means every deal on our platform comes with a built-in 25% equity cushion from the borrower. A property would have to lose more than a quarter of its value before your investment is affected.

As a result, our investors have never lost a dollar of principal.

Get Your Full Principal Back in 6 to 12 Months, Not 3 to 5 Years

Crowd Street deals are illiquid by design. Once you commit capital to a deal, it is locked up for 3 to 5 years. There is no secondary market to sell your position, and there are no early-exit options that don't come with penalties.

Constitution Lending operates on a shorter investment horizon. The loans on our platform run 6 to 12 months. At the end of the term, the borrower sells or refinances the real estate properties and uses the proceeds to repay the loan in full. At that point, you receive your entire principal back.

You can choose to reinvest in more loans on our platform, diversify into other real estate assets, or withdraw your capital entirely. You are never more than 12 months away from having full access to your principal.

Start Investing with $1,000 Instead of $25,000

Crowd Street requires a minimum investment of $25,000 per deal, which is a significant barrier even for high net worth investors wanting to diversify across multiple real estate opportunities rather than concentrating capital in one deal.

For beginner investors or those building their portfolio incrementally, this pricing structure is extremely restrictive.

Constitution Lending allows investors to get started with as little as $1,000. Rather than concentrating a large amount into a single deal, you can spread your capital across multiple loans simultaneously, diversifying across different borrowers, real estate projects, geographic markets, and loan structures. One loan underperforming doesn't affect your entire investment portfolio.

Read more: Investing in Performing Notes: What They Are, Benefits & How to Start

Additional Benefits of Investing with Constitution Lending

We Have a Borrower Default Rate of Under 2%

The strength of any real estate debt investment platform comes down to the quality of its vetting process and the borrowers it lends to. A borrower who stops making payments is the primary risk you face as an investor, which is why we are transparent about our default rate.

We have a default rate of less than 2%, meaning that out of every 100 loans we originate, fewer than 2 borrowers default. That is less than half the national average default rate on real estate loans, which the Mortgage Bankers Association reported at 4.26%.

This is not a coincidence. We lend exclusively to experienced real estate professionals, including flippers, construction companies, and rental investors with proven repayment records. Over the years, we have built a deep network of these borrowers and apply strict underwriting standards on every loan.

You Receive Payment Guarantees on Every Loan

Even with a default rate under 2%, we understand that investors want to know exactly what happens if a borrower stops paying. That is why every loan on our platform comes with a payment guarantee.

If a borrower misses a payment, the guarantee activates automatically. We pay your monthly interest out of our own funds for up to 6 months while we work to resolve the situation. This could mean getting the borrower back on track or foreclosing on and liquidating the underlying real estate assets.

To our knowledge, no other real estate crowdfunding site offers this level of protection. Most platforms, including Crowd Street, leave investors fully exposed if a sponsor or borrower stops performing.

How to Get Started with Constitution Lending

Getting started takes less than five minutes and requires no commitment to invest until you are ready.

- Create a free investment account by providing your name and email address. We have no accreditation requirements and no minimum deposit to get started.

- Browse available loans on your dashboard. Each listing displays the key details you need to make informed investment decisions, including the property address, loan amount, loan-to-value ratio, projected yield, loan term, borrower credit profile, and investment strategy.

- Dig deeper into any loan that interests you. Click on a listing to access a full breakdown of the deal, including the remaining loan balance, current and after-repair property value, a summary of the borrower's track record, and the deal's exit strategy.

- Connect a funding source. Link a bank account or an individual retirement account (IRA). We accept both standard bank transfers and IRA contributions for investors who want to take advantage of tax-advantaged investing.

- Make your first investment. Select the loan you want to invest in, click the Fund This Loan button, and enter your desired investment amount. You can start with as little as $1,000.

- Receive monthly interest payments from borrowers on the first of every month for the duration of the loan term. When the loan matures, your full principal is returned, and you can choose to reinvest, diversify, or withdraw.

Earn 10% to 14% Borrower Interest on Real Estate Loans with Constitution Lending

Create a free account to explore our real estate loans and start investing with as little as $1,000.

2. Willow Wealth (formerly Yieldstreet)

Willow Wealth, formerly known as Yieldstreet, is an alternative investment platform that you'll likely come across in your research.

Founded in New York, the platform offers access to private market opportunities across real estate, private credit, art, venture capital, and other asset classes. Their Alternative Income Fund is open to non-accredited investors with a $10,000 minimum, while individual deal offerings require $10,000 to $25,000 and are limited to accredited investors only.

Willow Wealth claims a net annualized return of 9.6% since inception, but this figure excludes active and defaulted investments.

A CNBC investigation found that investors lost at least $78 million across 30 real estate deals, with four resulting in total losses and 23 more placed on an internal watchlist.

Sponsor and asset quality are also a concern. As of December 31, 2024, 2.7% of their offerings have defaulted, and an additional 4.3% have a modified outlook. The rebranding to Willow Wealth in October 2025 came directly in the midst of the CNBC investigation, and the platform settled a federal class action for $9 million in 2025.

The SEC previously fined the company $1.9 million in 2023 for failing to disclose known collateral risks to investors. PeerStreet, a comparable real estate debt platform, went bankrupt in 2023, a cautionary reminder that platform stability matters when evaluating real estate investment opportunities.

Considering the four evaluation criteria we outlined earlier: Willow Wealth doesn't invest its own capital alongside yours; advertised returns are significantly overstated once losses are factored in; most investments carry multi-year holding periods with limited liquidity; and there is no payment guarantee protecting your income if a deal underperforms.

Read more: Top 5 Yieldstreet Alternatives | Higher Returns & More Liquidity

3. Fundrise

Fundrise is one of the largest real estate crowdfunding sites in the country, giving both accredited and non-accredited investors access to diversified real estate portfolios through their eREITs and interval funds.

Minimum investments start at $10, annual management fees are low at 0.15%, and investors can contribute through an IRA. Their portfolio spans multifamily properties, single-family rental homes, commercial real estate investment properties, and vacation rentals across multiple markets.

However, returns have been modest relative to the risk involved. Fundrise's Flagship Real Estate Fund has generated annualized returns of approximately 4.3% since inception, below both Constitution Lending's 10% to 14% high-yield returns and the historical average of broad market index funds. By most investment benchmarks, these returns do not adequately compensate investors for the illiquidity and equity risk they are taking on.

The core structural limitation is the same one that applies to Crowd Street and most equity platforms. Fundrise investors hold equity positions in real estate assets, which means they absorb losses in property value before any lender or debt holder is affected. In a declining market, that dynamic exposes individual investors to the full force of the downturn without any buffer.

Fundrise does not invest its own capital alongside investors and does not offer a payment guarantee. Most funds carry multi-year holding periods with limited early redemption options, and investors are last in line on any property sale proceeds after all debt is settled. Platforms like EquityMultiple and RealtyMogul offer similar equity-based structures with comparable structural limitations.

Platform stability is not a meaningful concern here. Fundrise is one of the most established real estate crowdfunding sites in the space, with over $7 billion in assets under management.

Read more: 5 Best Fundrise Alternatives for Higher Yields and More Liquidity

4. Arrived Homes

Arrived Homes is a real estate crowdfunding platform that allows retail individual investors to purchase fractional shares in single-family rental properties and vacation homes starting with as little as $100.

The platform handles all asset management responsibilities, making it a fully passive investment with no accreditation requirement. This makes them a popular entry point for beginner investors looking to access private real estate without the complexity of direct ownership.

Cash distributions are modest. According to Arrived Homes' own published Q3 2025 performance data, individual single-family residential properties earned an average annualized dividend of 4%, and vacation rental homes earned an average of 2.4%. These figures represent the actual cash payments investors receive and fall well short of the high-yield returns available through real estate debt investing.

The holding period is long and illiquid. Arrived investments typically carry holding periods of 5 to 7 years, and exiting before the property sells comes with fees and penalties. For investors who found Crowd Street's multi-year lockups frustrating, Arrived presents the same structural illiquidity at a much lower investment minimum.

The structural risk also mirrors Crowd Street's equity-first dynamic. Arrived’s shareholders hold equity positions in individual real estate properties, which puts them at the back of the line when a property is liquidated. In a market where property values soften, the decline hits equity investors first before anyone else feels it. There is no payment guarantee and no mechanism to protect your passive income if a tenant stops paying or a property sits vacant.

5. Roofstock

Roofstock is an online marketplace that allows individual investors to purchase single-family rental homes outright or through their fractional ownership program, Roofstock One. The platform provides detailed property financials, inspection reports, and tenant information so investors can make well-informed investment decisions before committing capital to individual real estate properties.

Rental yields typically average between 3% and 8% annually, below Constitution Lending's 10% to 14% high-yield returns. Investors are also responsible for asset management costs and closing costs on each transaction, which further reduce net returns. Because Roofstock is a direct property ownership platform rather than a lending platform, investors own real estate equity directly and are last in line on any sale proceeds after all debt is satisfied.

Exiting a Roofstock investment requires going through a full property listing and sale process, which can take months depending on market conditions. There is no payment guarantee, no co-investment from the platform, and no debt-level protection from market downturns.

Platform uncertainty is less of a risk because Roofstock is a well-funded company with over $365 million raised from institutional investors, but the structural limitations on capital protection and liquidity mirror those of other equity platforms on this list.

Investors with a lower risk tolerance or a shorter investment horizon will find that Roofstock's equity structure and variable rental income make it a less predictable option compared to a real estate debt platform with fixed interest payments and a defined repayment timeline.

Read more: 7 Best Roofstock Competitors for More Safety & Higher Returns