In our experience as both real estate investors and private lenders, choosing the right Connecticut DSCR lender comes down to three considerations:

- How quickly can they close? Check how fast a lender issues quotes, term sheets, and pre-approval letters, as this reflects their internal efficiency and is a good proxy for their overall closing speed. These are the simplest documents in the entire process, and if they take days to issue, it's unlikely they'll close quickly.

- Are they a direct lender or broker? Brokers aren't the decision makers on your loan. This can lead to situations where you're reassured for weeks that everything is on track, only to get rejected later when the actual lender identifies issues the broker missed. Work with direct lenders because they are the decision makers and can provide certainty early on.

- Are they actually based in Connecticut? We advise working with Connecticut-based DSCR lenders rather than ones that can lend in Connecticut. That's because Connecticut-based lenders understand local market dynamics and state-specific legal requirements, which translates into faster closings, less drama, and often lower rates (we explain how in more detail below).

Below, we review 5 DSCR lenders in Connecticut against these three factors. We start with Constitution Lending, then cover other lenders you are likely to encounter in your research.

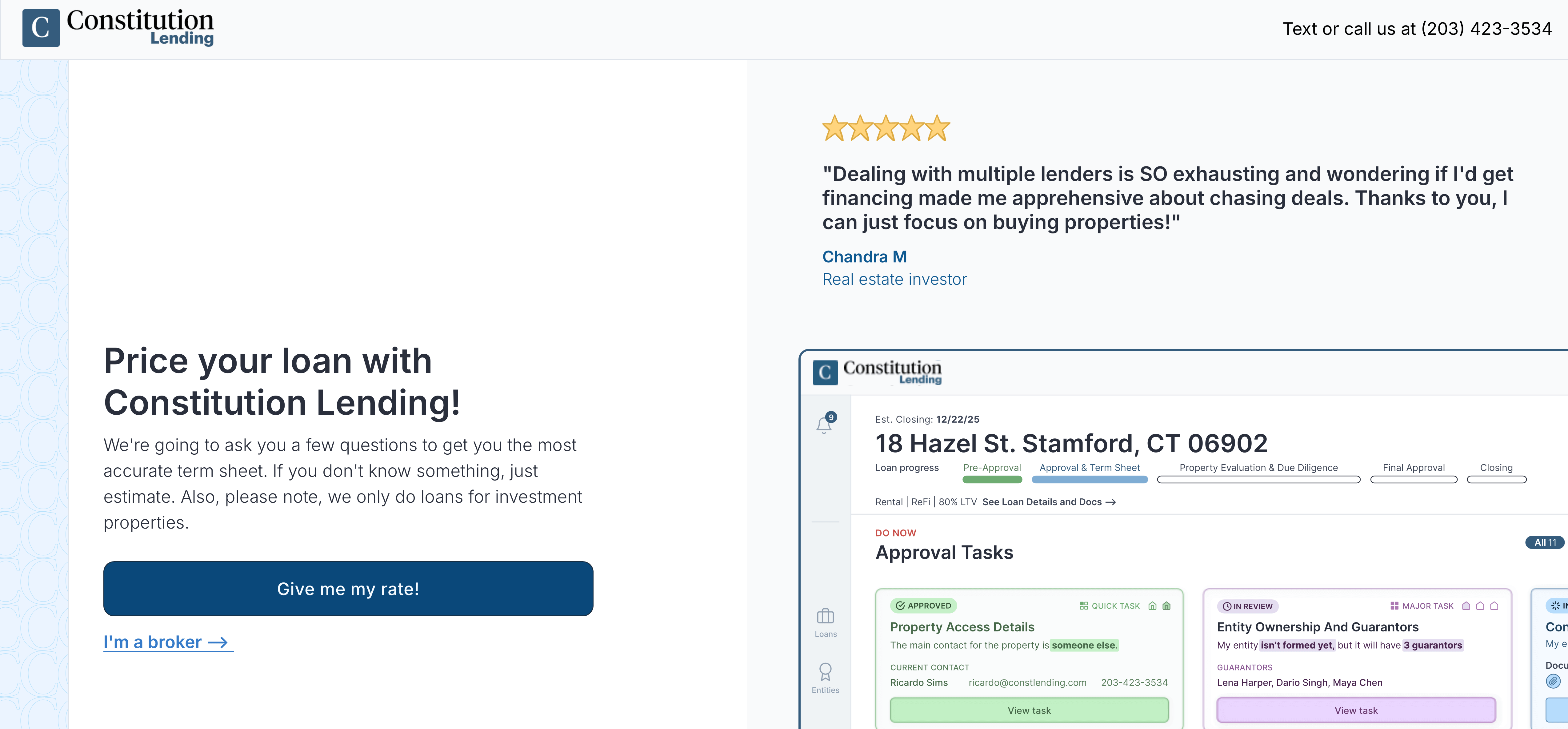

Use our automated DSCR loan pricer to generate instant quotes, term sheets, and pre-approval letters and see what rates and terms you qualify for.

1. Constitution Lending: A Connecticut-based DSCR Lender That Reliably Closes Within 7 to 14 Days

Before we were lenders, we were real estate investors working in Connecticut. During our investing years, we lost out on countless undervalued properties because our lenders took months to close after promising a one-week turnaround.

We also had lenders tell us that everything is on track and that we can easily qualify, only to surface a problem days before closing, with our earnest money already committed. So, we built our lending business with the processes to ensure that this doesn't happen to you.

To date, we have funded hundreds of millions of dollars in DSCR loans in Connecticut, helping property investors grow their long-term rental portfolios without the income verification requirements of conventional mortgages.

This is how we deliver on the three criteria mentioned above:

How Our Automated Pricer and Documents Portal Allow Us to Close in 7 to 14 Days

Most DSCR lenders in Connecticut promise to close in a week or two, but very few can actually deliver. That's because they run applications through the same slow, bureaucratic processes as banks.

For example, loan officers only review your application days after you submit it. When they get to your file, they ask for documents one at a time rather than all at once, which means constant back-and-forth that stretches across weeks. It's also common for them to schedule appraisals late, which causes further delays.

At Constitution Lending, we built our internal process around automated systems to minimize delays and help property investors close faster. Here's how it works:

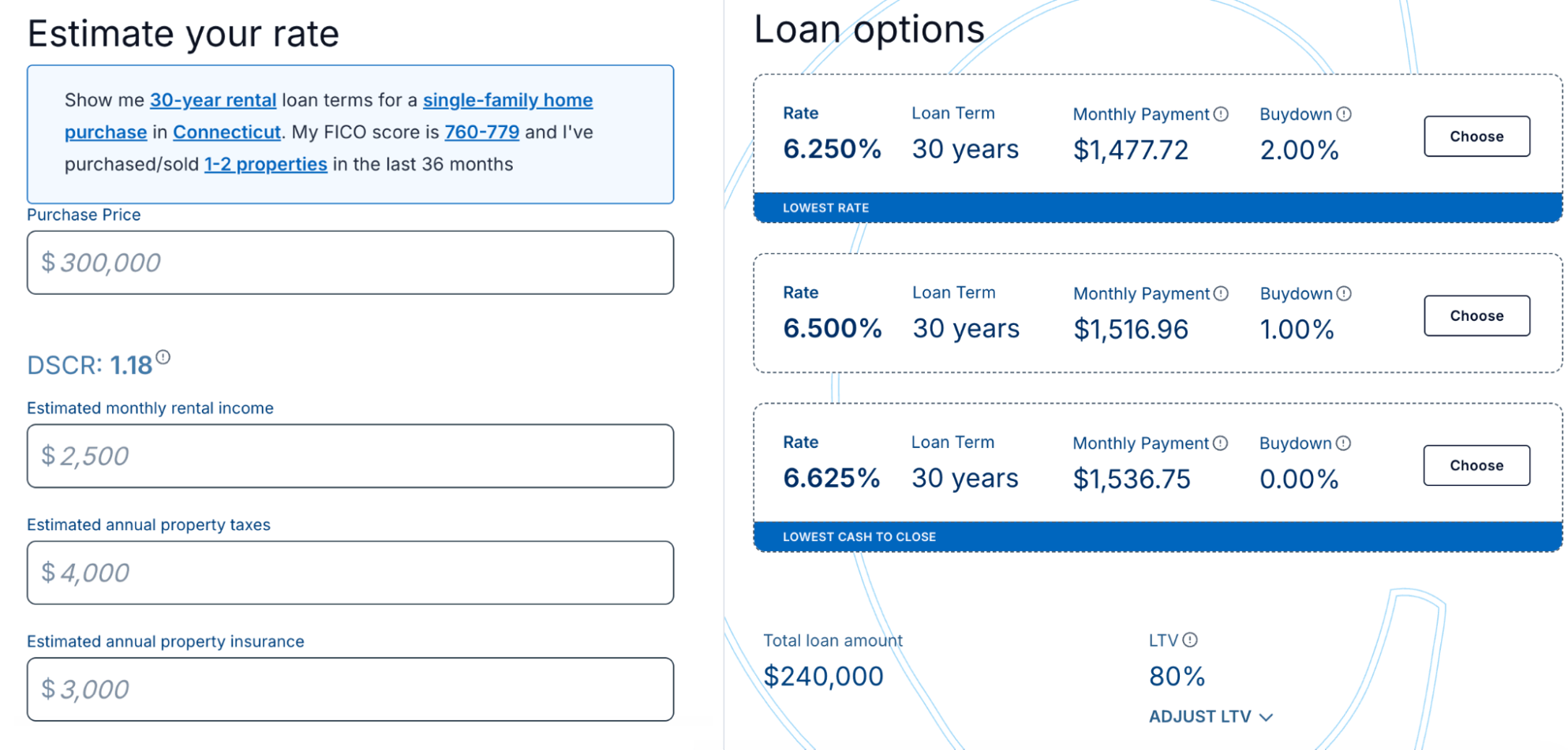

- Submit your deal through our automated pricer. All we need is the property location, property type, purchase price, loan amount, and your credit score.

- The pricer instantly returns three quotes, each showing your interest rate, monthly payment, loan term, maximum LTV, prepayment penalties, and available buydowns.

- Adjust the loan amount, LTV, and after-repair value in real time to see how different inputs affect your financing options.

- Select your preferred quote and enter your name and email address. A term sheet, pre-approval letter, and copy of your quote are available to download immediately.

- You'll get access to our documents portal at the same time. The portal lists every document required for your DSCR loan in one place, including bank statements, entity documents, proof of insurance, and any applicable renovation or construction budget. You can submit everything in one shot rather than responding to a new request every few days.

- Submit your documents and receive a clear yes or no within a few hours.

- We close in 7 to 14 days. When a borrower's earnest money is at risk because another lender fails to deliver, we have stepped in and closed within 4 days.

Read more: How to Get a Loan for an Apartment Complex Guide

We Are a Direct Lender: No Brokers, No Last-Minute Rejections

Brokers don't fund loans and therefore aren't the decision makers. They review your file, give you early feedback, submit your application to a third-party lender, and then wait for a decision, just like you do.

Their early assessment is based on incomplete information: a credit score, a rough property description, and a general sense of the deal.

The actual lender bases its decision on full documentation, such as rent rolls, leases, bank statements, and complete DSCR calculations, so it's common for the lender to find problems later that the broker missed. That's why many borrowers get rejected a few days before closing, even after being reassured that everything is fine.

At Constitution Lending, you work directly with the team funding your loan. We've funded hundreds of millions of dollars in property loans using our own capital, so we know our underwriting criteria inside and out. When you submit your documents, we can give you a definitive yes or no within hours, not a preliminary opinion based on a surface-level review.

Working with a direct lender also costs less. Brokers layer their fees and markups, including origination fee inflations, on top of a lender's base rates. As a direct lender, our rates reflect the actual cost of our capital, with no intermediary markups added.

Read more: DSCR Loan Pros and Cons: A Detailed Guide for Investors

Are They Actually Based in Connecticut?

In your research, you will come across many DSCR lenders who are licensed to lend in Connecticut but are headquartered in Texas, California, New York, or other states. Connecticut is simply one of many states on their lending map.

That distinction matters more than most borrowers realize because a lender who does not operate locally is applying generic national underwriting assumptions to a market they don't know firsthand. That can work against you in a few ways:

- It's common for them to charge higher interest rates on your mortgage loan because they don't understand the nuances of the Connecticut real estate market. They may underestimate market rent and the property's cash flow potential, for example, and think your deal is riskier than it actually is.

- They are less likely to have established relationships with Connecticut appraisers and title companies, which means slower vendor turnaround and a higher risk of local compliance issues that affect your eligibility for financing.

Constitution Lending is based in Connecticut and we originate the majority of our loans here. Before we were lenders, we were real estate investors buying and managing long-term rental properties in this state.

We know what market rent and the property's rental income potential look like in Hartford, Greenwich, and New Haven. We know Connecticut's transfer tax requirements, title norms, and disclosure rules inside and out. We have established relationships with local appraisers and title companies, whom we trust to move quickly.

For you as a borrower, that translates into three concrete advantages:

- Lower interest rates: Because we understand Connecticut's rental markets, we assess your deal the way a local investor would, not through a generic national lens. This often translates into lower interest rates, a smaller down payment requirement, and fewer unnecessary conditions.

- Faster appraisal and title turnaround. We have established relationships with Connecticut appraisers and title companies, keeping your closing timeline on track.

- Fewer last-minute complications. Connecticut has specific transfer taxes, title norms, and disclosure requirements. Because we have closed hundreds of deals in this state, we have already encountered every local wrinkle. If something comes up during your closing, we know exactly what it is and who to call to resolve it fast.

Secure Fast High LTV DSCR Loans with Constitution Lending

Enter a few details about your deal into our automated pricer and generate instant quotes, term sheets, and pre-approval letters.

2. Easy Street Capital

Easy Street Capital is a Texas-based private lender that you'll likely encounter in your research. Their EasyRent program offers DSCR financing options on single-family homes, condos, duplexes, triplexes, and multifamily properties up to 10 units, with rates starting at 5.75%.

They can lend up to 80% LTV on purchases, requiring a larger down payment of at least 20%, and 75% on cash-out refinances. They also have no minimum DSCR requirement, so borrowers can qualify even if the property's cash flow doesn't fully cover its debt obligations.

Easy Street Capital operates as a direct lender, so you aren't dealing with a broker submitting your file to a third party.

On the process side, however, Easy Street doesn't offer an automated pricing tool comparable to Constitution Lending's pricer. Borrowers initiate the process by requesting a quote directly, after which a loan officer follows up to discuss terms.

For Connecticut property investors who need to move quickly, that manual front-end process introduces the same early-stage delays that can cost you a property before underwriting even begins.

Finally, Easy Street is based in Texas, meaning they do not bring the same on-the-ground familiarity with Connecticut's specific markets, market rent levels, or local investment opportunities that a locally rooted lender can offer.

3. Griffin Funding

Griffin Funding is a California-based mortgage lender offering DSCR loans in Connecticut as part of a broader national lending platform.

Their Connecticut DSCR loan program covers single-family homes, multifamily properties, and vacation rentals, with up to $20 million in financing. No income or employment verification is required for self-employed borrowers and those with non-traditional income, and they offer an unlimited cash-out option. They serve borrowers throughout Connecticut, including Bridgeport, Hartford, New Haven, Stamford, and Greenwich.

Griffin Funding also positions itself as a direct-to-consumer lender, which removes the broker layer from the transaction.

That said, their DSCR loan process is largely relationship and form-driven. Borrowers fill out an application form online and are then contacted by a loan officer to move forward. There is no self-serve automated pricing tool that lets you generate a quote, term sheet, and pre-approval letter on the spot.

That lack of instant pricing visibility is a significant limitation for Connecticut property investors looking to move quickly on real estate investment opportunities.

Griffin Funding is also a California-based national lender, which means Connecticut investors are working with a team that does not have the same local market knowledge, understanding of market rent dynamics, or familiarity with Connecticut's specific financing options as a lender based in the state.

4. MoFin Loans

MoFin Loans is a New York-based lender offering DSCR rental loans for Connecticut real estate investors. Their program covers single-family homes, 2 to 4-unit properties, and multifamily buildings up to 10 units, with a focus on long-term rental and buy-and-hold investment goals.

They also offer bridge loans and ground-up construction financing for property investors who need short-term capital before transitioning into permanent DSCR financing to grow their rental portfolio.

We like that MoFin Loans has published Connecticut-specific content and positions themselves as knowledgeable about the state's rental market, which is a step above purely national lenders with no local context.

On the process side, MoFin uses a scenario builder tool on their website that allows borrowers to enter deal details and receive preliminary terms, which is faster than a fully manual process. However, this tool does not instantly generate a downloadable term sheet or pre-approval letter like Constitution Lending's automated pricer. There's still some follow-up and back-and-forth required before you have documents in hand.

MoFin is also a New York-based lender. Although they lend in Connecticut, they do not bring the same depth of local market experience, knowledge of market rent, or understanding of the property's cash flow potential in specific Connecticut markets as a lender who has operated and invested in the state firsthand.

5. Visio Lending

Visio Lending is a Texas-based lender specializing in long-term DSCR rental loans for real estate investors nationwide, including in Connecticut.

Their loan program covers single-family homes, condos, townhomes, and 2 to 4-unit properties, with loan amounts from $75,000 to $2 million, and 30-year fixed and interest-only options. No personal income verification is required, making them a popular financing option for self-employed borrowers and investors with non-traditional income structures.

That said, their process follows a traditional application model where borrowers submit a loan request online and are connected with a loan officer to receive preliminary terms.

There is no automated pricing tool that generates instant quotes and pre-approval letters independently. Visio also caps loan amounts at $2 million, which may limit Connecticut property investors pursuing higher-value multifamily or mixed-use investment opportunities.

And like the other lenders on this list, Visio is a Texas-based national lender without the local market grounding, knowledge of Connecticut market rent levels, or familiarity with state-specific financing options that comes from actually investing and operating in Connecticut.