Almost all multifamily bridge lenders advertise fast closings, but few actually deliver.

According to borrowers we've spoken with, the gap between what lenders promise and their actual closing times is one of the biggest problems in the industry. Deals that were supposed to close in 10 days routinely drag on for 30 days or longer.

Another common issue is that some bridge lenders will greenlight applications early on, only to reject them at the last minute. This forces borrowers to forfeit their earnest money deposits and lose out on potentially undervalued real estate.

To avoid both problems, here's what we recommend looking for in a bridge lender:

- How quickly do they issue term sheets, quotes, and approval letters? The speed at which a lender can produce these early-stage documents reflects its efficiency. Lenders who are slow at this don't suddenly pick up the pace as you get to closing. The fastest bridge lenders can issue instant quotes, term sheets, and pre-approval letters.

- Are they a direct lender? As we explain later, last-minute rejections are almost always caused by brokers. Because brokers aren't the decision makers, you never speak directly to the person who is, and that disconnect often leads to problems. A broker may think you qualify based on your documents, only for the actual lender to flag discrepancies the broker missed.

Below, we review some of the top multifamily bridge lenders and evaluate them against these two factors.

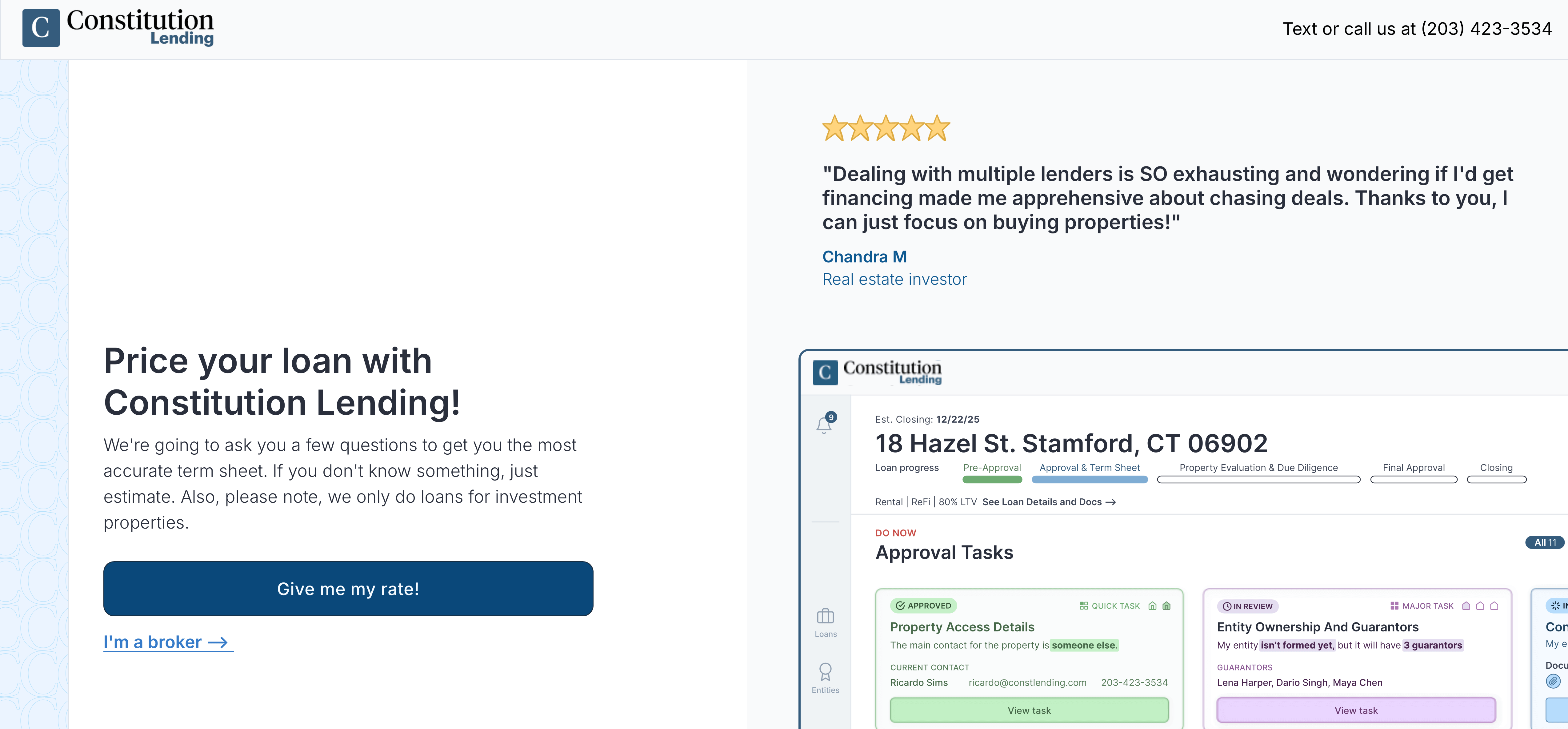

We start with an overview of Constitution Lending: how we close faster than most lenders and give you certainty early on in the application process that everything will go smoothly.

Use our automated bridge loan pricer to generate instant quotes and see what you qualify for.

1. Constitution Lending

A Direct Bridge Lender That Consistently Closes in 7 to 14 Days

Before founding Constitution Lending, we were real estate investors ourselves, and we missed out on millions of dollars in undervalued properties because bridge lenders couldn't follow through on their promises.

For example, we frequently dealt with bridge lenders who promised one-week closings and ended up taking over a month. We've also had loans approved early, then watched them fall through weeks into underwriting.

We deeply understand the problems you’re facing; we've experienced them firsthand. So we structured Constitution Lending from the ground up to close loans more quickly and reliably than other lenders.

Today, we've funded hundreds of millions of dollars in multifamily and commercial real estate loans, including apartment buildings, mixed-use properties, and value-add acquisitions.

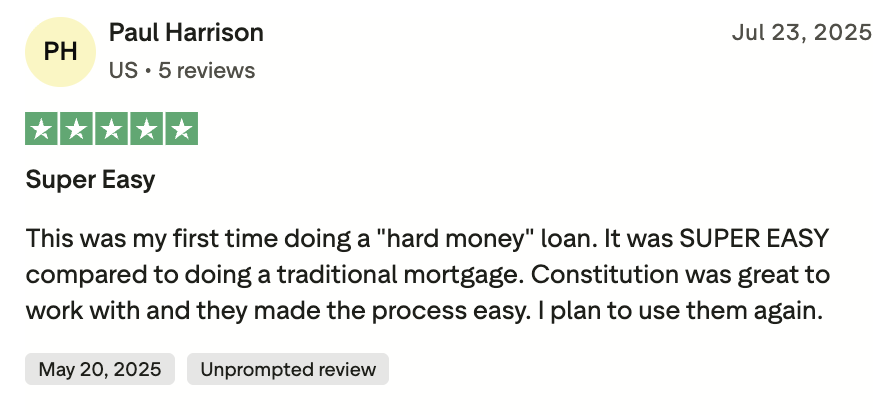

See what borrowers say about our closing speed and reliability:

Let’s dig into how Constitution Lending addresses the two problems above.

You Can Reliably Close Within 7 to 14 Days Using Our Automated Pricer and Documents Portal

Most delays trace back to one source: slow, manual processes on the lender's end.

After you submit an application, it typically sits in a queue for days. Eventually, a loan officer reviews it. Then come the calls, follow-up emails, and more waiting for quotes, term sheets, and pre-approval letters.

These bottlenecks compound as you approach closing, leading to 30+ day closing times that defeat the entire purpose of bridge financing.

That's why we advise against taking a lender's word on closing speed. Instead, look at how quickly they issue quotes, term sheets, and pre-approval letters. Lenders who can turn these around quickly likely have the infrastructure to move fast throughout the entire process. Conversely, lenders who take multiple days to provide these won't speed up all of a sudden as you get to closing.

At Constitution Lending, we built our origination process around an automated pricer and documents portal that eliminates friction entirely.

Here's how the process works from when you first apply to when you close:

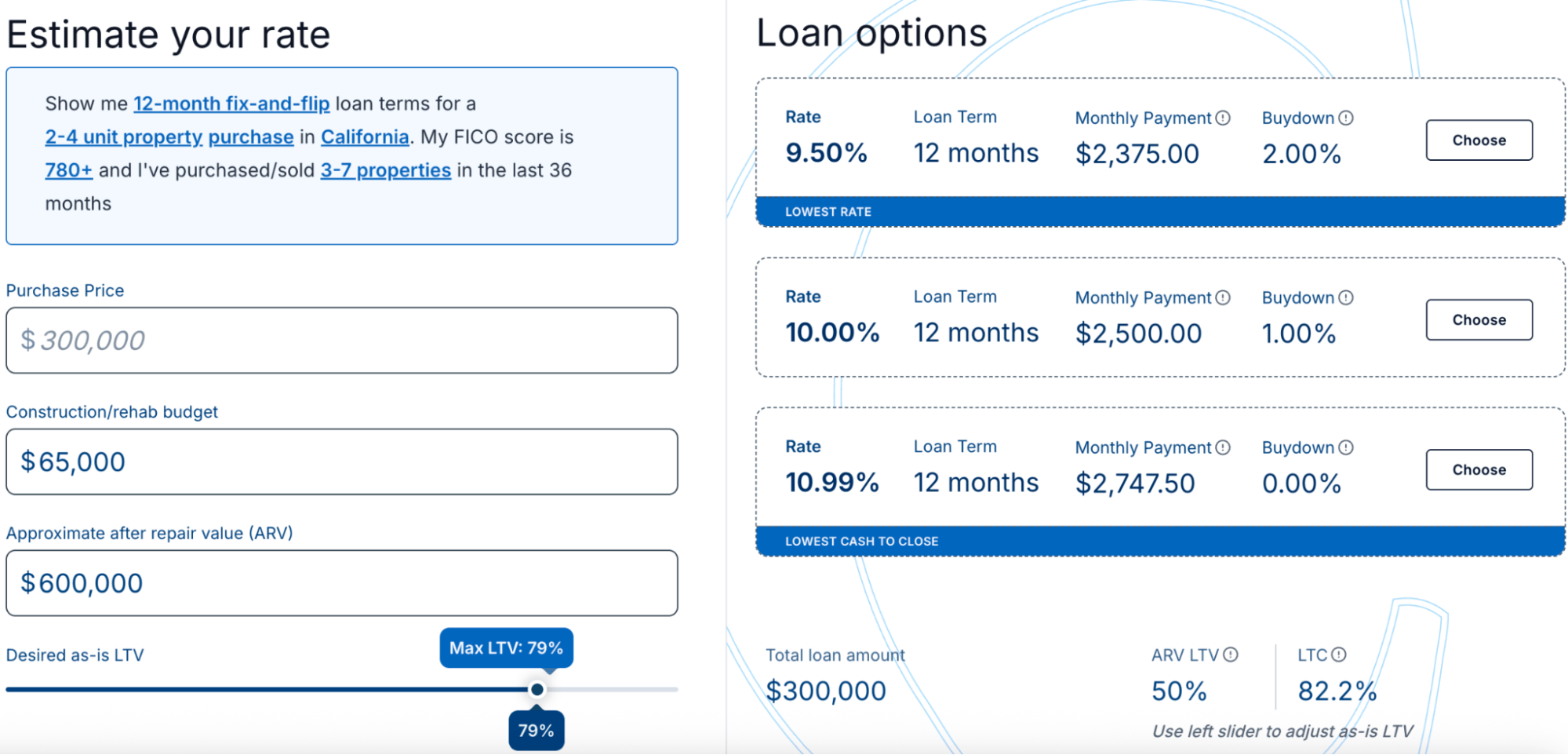

- Enter your deal information into our automated bridge loan pricer. This includes the property’s address and type, purchase price, requested loan amount, and your credit score.

- The pricer instantly returns three bridge loan options. Each quote shows your interest rate, monthly payment, loan terms, maximum LTV, prepayment terms, and available buydowns.

- Adjust the loan amount, LTC, after-repair value, and interest-only options to see how different variables affect your three financing options before committing to one.

- Select the quote that best fits your needs and situation, and enter your contact details. A term sheet, pre-approval letter, and copy of your quote are available to download immediately. No appointment needed, no waiting on a loan officer to respond.

- You'll receive access to our documents portal at the same time, which outlines the paperwork you need to submit. This typically includes bank statements, entity documents, proof of insurance, and a renovation or construction budget (if applicable).

[source: loan-progress-san-francisco-example-v2]

- Submit your documents and receive a definitive yes or no within a couple of hours. No vague responses, no promises to follow up.

- We fund in 7 to 14 days through the title company. When a slow lender puts a borrower’s earnest money at risk, we've stepped in and closed in under four days.

We Are a Direct Lender So You Get Certainty Early in the Application Process That You Qualify

Most last-minute rejections and complications stem from loan brokers.

Brokers don't fund loans themselves but instead submit your application to an actual lender and wait for a decision. They may tell you early on that you're good to go based on their assessment, but if the lender uncovers a problem during underwriting that they missed, you can get rejected after weeks of assuming everything was on track.

We've heard stories from borrowers who lost their earnest money deposits this way, rejected days before closing after receiving an early green light from the broker weeks prior.

At Constitution Lending, you work directly with the team funding your loan. There are no brokers, no intermediaries, and no third-party underwriting decisions that can unravel your deal at the last minute.

Having funded hundreds of millions of dollars of our own capital in multifamily real estate, we know our underwriting criteria inside and out. We can evaluate your file quickly and give you a clear answer within hours of receiving your documents. If there's a problem, we identify it early so you can correct it before applying again.

It's also worth noting that working through a broker adds broker fees and markups to a lender's base rates. As a direct bridge lender, we help you secure lower rates by eliminating broker fees.

Read more: Commercial Loans for Mixed-Use Properties: Top 3 Options

Bonus: You Can Get Your Bridge Loan and Long-Term Financing from the Same Lender

Bridge loans are short-term financing (12 to 24 months), so most real estate investors plan to refinance into permanent financing.

As a result, we recommend coordinating both your bridge loan and your long-term refinancing with a single lender, as this has several advantages.

Namely, the lender who originated your bridge loan already knows the property, the business plan, and your track record as a borrower. That continuity speeds up the transition to permanent financing and eliminates the risk of finding a new lender willing to refinance your property before the term ends.

Constitution Lending offers both multifamily bridge loan programs and 30-year DSCR financing solutions for rental investors. So you can move from acquisition to long-term financing without switching teams.

For a deeper look at DSCR loans and their pros and cons, read our full breakdown.

Get a Fast Multifamily Bridge Loan from Constitution Lending

Enter some details into our automated pricer to see what bridge loan terms you qualify for.

2. Ready Capital

Ready Capital is one of the larger non-bank commercial real estate lenders in the country. They have a dedicated multifamily bridge loan program built for transitional and value-add deals. These programs offer loan amounts up to $75 million, which is ideal for large, institutional real estate investors looking to purchase apartment complexes and other large commercial properties.

They also offer non-recourse financing, meaning that if a borrower defaults, the lender can only claim the collateral, not the borrower's personal assets. This reduces risk on your end.

That said, Ready Capital doesn’t offer true 30-year fixed-term loans like residential DSCR loans. From what we could find, their longest-term loans are 5 to 10 years long, so they aren’t the best option if you’re looking to refinance into longer-term financing soon after your purchase.

In addition, Ready Capital operates like an institutional lender. There's no publicly available automated pricing tool or self-serve quoting system, so it’s unclear how quickly they can actually close.

Instead, borrowers work through a Relationship Manager to receive preliminary terms. For investors working with 5 to 20-unit properties, their minimum loan thresholds and relationship-driven process may not be a great fit. This lender is designed for larger, more complex bridge transactions.

2. Greystone

Greystone is one of the most established names in multifamily lending. They're the number one HUD multifamily lender in the country by firm commitments and generated over $13 billion in commercial real estate transaction volume in 2023. Their bridge loan program is purpose-built for value-add, lease-up, and repositioning deals.

Unlike Ready Capital, Greystone offers a direct pathway from bridge financing into 30-year financing. That bridge-to-permanent transition, handled in-house by the same team, is one of the cleanest exit strategies available to multifamily investors.

However, Greystone doesn’t offer DSCR loans like Constitution Lending. Instead, their long-term financing options are limited to Fannie Mae, Freddie Mac, FHA, and HUD loans, which are significantly more difficult to qualify for.

Another limitation is who Greystone is actually built for. Based on publicly announced deals, their bridge loans routinely range from $9.5 million to over $100 million. Individual investors working with 5 to 20-unit properties are unlikely to meet their minimum loan thresholds.

On the process side, there's no publicly available automated pricing tool, self-serve origination tool, or documents portal, so it’s unclear how quickly they can close.

Read more: 6 Best Rental Property Lenders & How to Pick the Right One

4. J.P. Morgan

J.P. Morgan has been aggressively marketing their bridge-to-agency program for multifamily investors. The core pitch is compelling: one institution handles both your bridge loan and your long-term agency financing. The same team that underwrites your bridge loan manages the transition to permanent financing, reducing friction at the refinance.

JPMorgan is a money-center bank with a massive balance sheet, funded by deposits and cheap institutional capital. This makes them a good option for larger, more complex deals as they can price competitively.

However, like Greystone, J.P. Morgan mainly refinances into 30-year Fannie Mae or Freddie Mac agency debt rather than DSCR loans. This can make it more challenging for real estate borrowers with high debt-to-income ratios and non-W2 income to qualify.

Their much-publicized selling point is closing "under 30 days." For a major bank, that may be impressive. For a borrower trying to beat a cash offer and needing to close in a few days, 30 days is not fast. J.P. Morgan is a strong option for large institutional multifamily deals, but not for individual investors who need genuine speed.

5. Renovo Financial

Renovo Financial is a Chicago-based private lender with a multifamily bridge and construction loan program. Their LTV goes up to 70% on multifamily properties. Their draw funding timeline of 24 to 48 hours is among the fastest in the space, which matters a lot for value-add projects.

Renovo is one of the few commercial bridge lenders to offer 30-year DSCR loans, not just Fannie Mae and Freddie Mac loans. This makes them a good option for real estate borrowers looking to refinance their bridge loan into a longer-term loan.

On the review side, the picture is mixed. Renovo holds a 4.5-star rating on Birdeye, based on 163 reviews, with borrowers consistently praising the origination and closing experience. However, a pattern emerges in the critical reviews.

Multiple borrowers on Trustpilot report problems during the loan servicing phase, including missed real estate tax payments and unpaid insurance that created unexpected liability. One reviewer described going three days without reaching anyone on the servicing team.

The BiggerPockets community has surfaced similar complaints from borrowers who had difficulty paying off their loans. Renovo appears to run a smooth origination process. The servicing experience, based on public reviews, is less consistent.

Close on a Multifamily Property within 7 to 14 Days with Constitution Lending

Generate instant quotes, term sheets, and approval letters using our bridge loan pricer and find out what you qualify for.