Although hard money lenders offer faster funding and easier qualification than banks, the lender you choose still matters because it can directly affect the success of your multifamily investment.

We’ve heard from countless borrowers who work with bad lenders that promise to close in days, but then drag the process out for months. Some are even rejected at the last minute after being assured they’re good to go.

The best hard money lenders close fast, give you confidence early on that your loan will go smoothly, and offer competitive APRs.

Below, we cover 6 factors to consider when choosing a multifamily hard money lender, then show how Constitution Lending addresses each one.

Use our automated pricer to generate instant quotes, term sheets, and pre-approval letters to see what you qualify for.

6 Factors to Consider When Choosing a Multifamily Hard Money Lender

1. Are They a Direct Lender or a Broker?

We always advise getting your hard money loan from a direct lender.

Brokers act as intermediaries and don’t control the final decision. They have to formally submit your loan application to a lender for underwriting before knowing whether you qualify.

A broker may believe you qualify, but if the lender uncovers an issue weeks into underwriting — which is common in multifamily deals — you can be rejected after being told you qualify. We’ve heard of borrowers getting rejected on the day of closing and having to forfeit their earnest money deposits.

Partnering with a direct lender reduces the risk of late rejections because you work directly with the people funding your loan. They know their requirements and can give you a quick, definitive answer after reviewing your documents, without waiting weeks for a third-party lender to complete underwriting.

If there's an issue with your file, a good direct lender can spot it immediately and inform you upfront.

2. How Fast Can They Actually Close?

Nearly every hard money lender advertises fast closings, but from our conversations with borrowers, few actually deliver. Many report being promised a one-week close, only for the process to stretch 30+ days.

Because of this, we don’t recommend relying on a lender's stated closing timelines.

A more reliable way to gauge speed is to look at how quickly they issue term sheets, quotes, and pre-approval letters. A lender that takes several business days to produce these documents won’t suddenly move faster as you approach closing.

The fastest commercial lenders use automated systems that allow borrowers to generate same-day quotes, term sheets, and pre-approval letters. That’s a strong signal they prioritize speed and have the infrastructure to move your loan forward quickly.

3. What Is the Cost of the Loan?

Interest rates and fees are another area where brokers can cost you.

Brokers add fees and markups on top of lenders’ interest rates, which can inflate your all-in borrowing costs. When you work directly with a lender, you're getting their actual rates without a layer of broker fees.

Another way to secure lower rates is to evaluate a lender’s experience funding multifamily properties and other types of commercial real estate.

Lenders who mainly focus on single-family loans often treat multifamily deals as riskier than they are. Common scenarios in multifamily investing (e.g., a unit or two sitting vacant during a transition, a value-add property operating below market rents) can trigger rate increases from an inexperienced lender.

An experienced multifamily lender understands the difference between a red flag and standard operating conditions. They won't penalize you for the realities of multifamily investing, helping you secure better rates.

4. What LTV Do They Fund?

Consider the lender’s LTV (loan-to-value) ratio — in other words, how much they’re willing to lend relative to the value of the investment property.

For example, if you purchase a $1 million multifamily property and the lender provides $700,000, your LTV is 70%.

Opt for hard money lenders that offer higher LTVs, as this reduces the down payment needed at closing. When refinancing multifamily properties, higher LTVs also allow you to pull out more equity and secure larger loan amounts.

The best hard money lenders can finance 70% to 80% of a property’s value for borrowers with strong credit.

5. How Do They Handle Draws for Value-add and Construction Projects?

If you're rehabbing or constructing a multifamily property, analyze the lender’s draw process. This is another common area where lenders create delays.

Hard money lenders reimburse you after each phase of work is completed, which is normal. But the speed of that reimbursement varies dramatically. Some lenders take days to process a draw request, which means your contractors stop working while you wait for funds.

Look for a private money lender who can process and fund draws within 24 hours after a stage of work is complete. This keeps project delays to a minimum.

6. Can They Help You Refinance Into Long-Term Financing?

Hard money loans typically have terms of 12 to 24 months. Once the term ends, borrowers generally sell the property and use the proceeds to repay the loan.

However, it’s becoming increasingly common for borrowers to refinance their hard money loans into long-term, 30-year loans, rent out the property, and generate monthly income.

If you plan to renovate and hold (or build and hold), we recommend choosing a lender that offers both short-term and 30-year loans. This allows you to secure long-term financing from a lender who already knows the deal, your property, and your situation — without having to re-explain everything to a new underwriting team under time pressure.

Read more: Mixed-Use DSCR Loans: Requirements, Rates, and How to Apply

1. Constitution Lending: Fast, High-LTV Lender for Multifamily Real Estate Investments

Constitution Lending was built by real estate investors who had been burned too many times by lenders who overpromised and underdelivered.

We've had countless lenders promise two-week closings, only to drag the process out for three months — or give early approvals, then reject the deal the day before closing. As a result, we lost millions in investment opportunities.

So we built our loan processes to eliminate those problems.

To date, we’ve lent hundreds of millions of dollars to real estate investors across the country, including multifamily real estate, apartment buildings, mixed-use properties, and other types of commercial properties.

Here's what borrowers say about working with us:

Let's walk through how Constitution Lending addresses each of the factors above.

We Are a Direct Lender, Meaning No Middlemen or Last-Minute Surprises

At Constitution Lending, you're speaking directly with the people funding your hard money loan. There are no brokers, no intermediaries, and no additional approval layers introducing uncertainty into your closing.

Because we've funded hundreds of millions of dollars of our own capital, we know our requirements inside and out. That means we can give you a clear yes-or-no decision within hours of receiving your documents.

If we see a problem with your loan application, we'll tell you early so you can address it. When we say you're approved, you're approved.

We Close in 7 to 14 Days Using Our Automated Pricer and Documents Portal

We don't ask you to take our word for our closing speed — you can test it yourself.

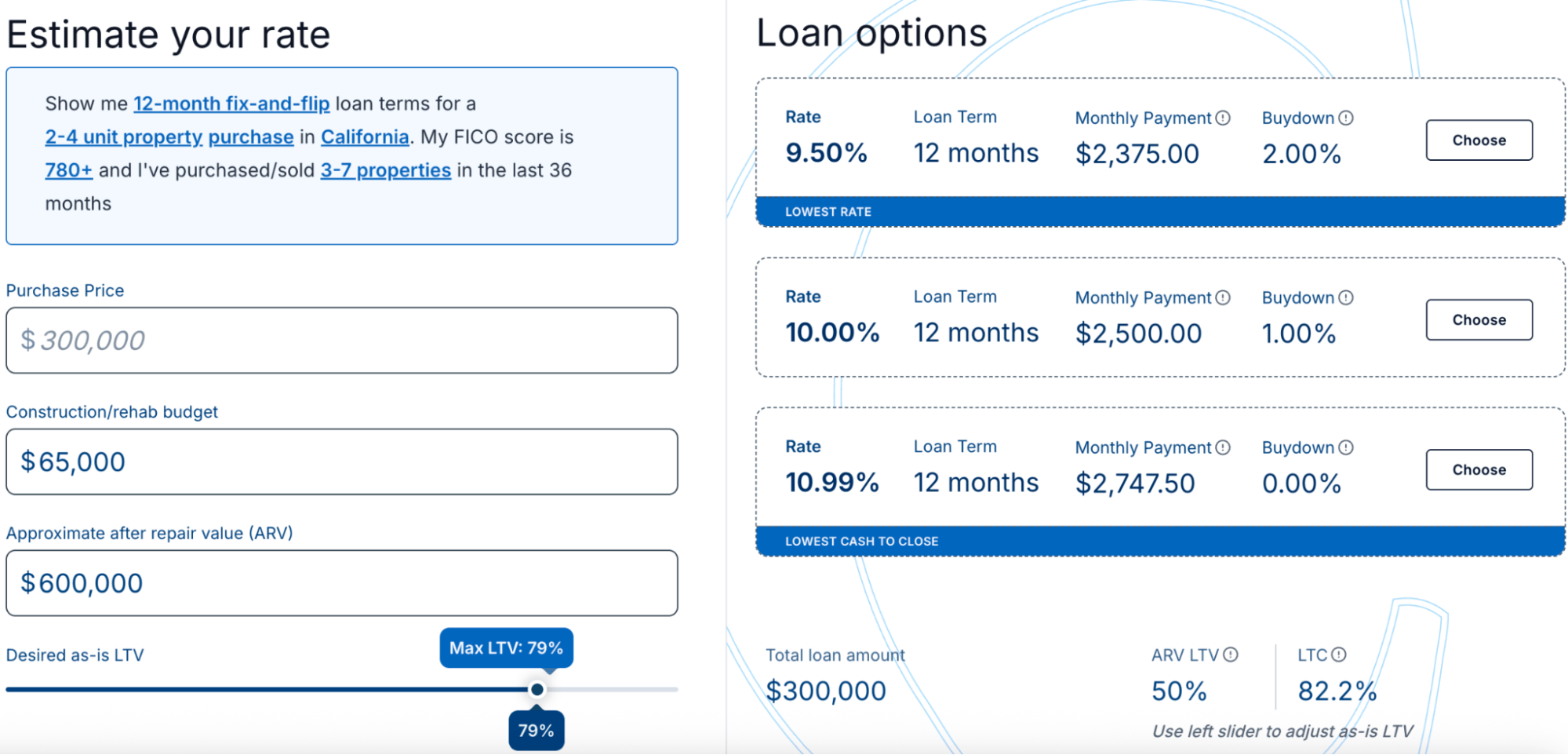

Enter your deal into our automated loan pricer to receive instant quotes, a term sheet, and a pre-approval letter.

There’s no need to book an appointment with a loan officer or wait weeks for these documents.

Here’s what our process looks like from loan application to closing:

- Start by entering your deal into our automated pricer. This includes property address, property type, purchase price, the loan amount you're looking for, and your credit score.

- The pricer instantly returns three financing options, each showing your interest rate, monthly payment, loan term, maximum LTV, prepayment penalties, and any available buydowns.

- You can run multiple loan scenarios. Adjust the loan amount, construction budget, after-repair value (ARV), and LTV to explore how each variable shapes your loan options and interest-only terms in real time.

- Select your preferred quote and enter your contact information. You can download a term sheet, pre-approval letter, and a copy of your quote on the spot.

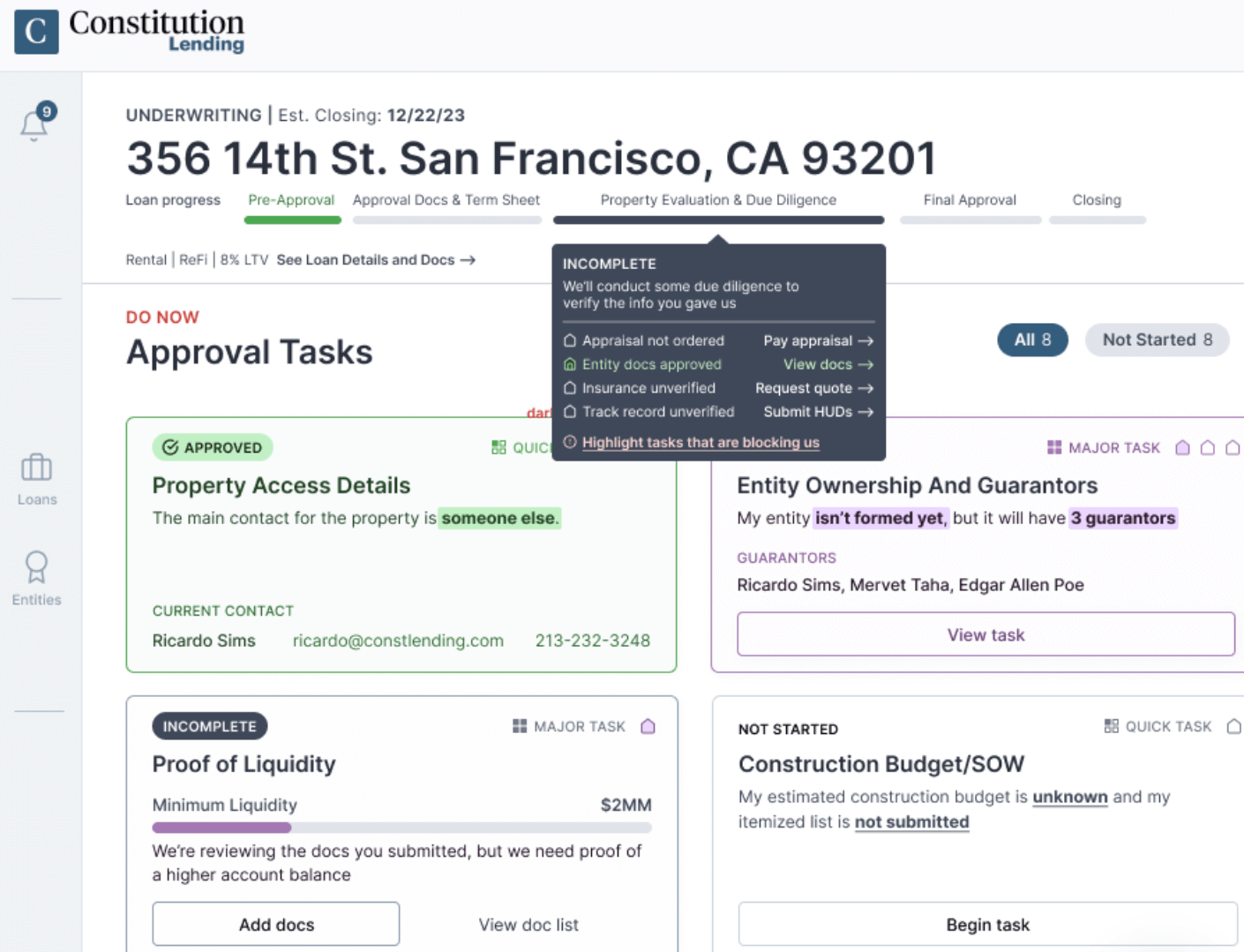

- You'll receive access to our documents portal, where you can upload everything we need to move forward. The portal lays out exactly what's required based on the loan product you're applying for. This typically includes bank statements, proof of insurance, entity documents, and a construction or renovation budget.

- Submit your documents, and we'll give you a definitive yes or no within a couple of hours. No vague feedback. No “we'll circle back with you.”

- We close in 7 to 14 days. When borrowers have been burned by a slow lender and their earnest money deposit is on the line, we've stepped in and closed in under four days.

High LTV, Accessible Credit Requirements, No Broker Markups

Because we're a direct lender, the rates and terms you receive are our actual rates — not a broker's rates with added fees.

Here's how our terms compare to what you'll typically find elsewhere:

Fast, Same-Day Draw Funding for Renovation and Construction Projects

For fix-and-flip and construction loans, we release renovation budget draws the same day each stage of work is completed. For example, once you've installed new windows and doors, you notify us, and we release that draw within a few hours so your project continues smoothly.

Read more: 5 Best Fix and Flip Lenders + Reviews

We Have Experience Underwriting and Funding Multifamily Real Estate

We’ve originated hundreds of millions of dollars in multifamily hard money loans, so we understand the nuances of these deals and don’t treat them as inherently risky like many single-family lenders do.

This experience allows us to offer lower rates and fees on multifamily real estate compared to lenders who primarily focus on single-family loans.

We Offer DSCR Loans for Long-Term Financing

In addition to multifamily hard money loans (fix-and-flip, construction, bridge loans), Constitution Lending offers 30-year DSCR loan programs as an exit strategy for long-term rental investors.

DSCR loans are the most popular long-term exit for multifamily investors because they’re underwritten based on your property's ability to generate cash flow rather than your personal income, W-2s, or debt-to-income ratio.

You can learn more about the pros and cons of DSCR loans here.

If that's your strategy, you can get your hard money loan with Constitution Lending and transition to a DSCR loan with us when the property is ready.

Read more: DSCR Loan Pros and Cons: A Detailed Guide for Investors

Get Fast Multifamily Hard Money Loans with Constitution Lending

Use our automated pricer to explore different loan scenarios and see what you qualify for.

A Few Alternatives to Consider

We believe Constitution Lending is the strongest option for most multifamily borrowers, but we still encourage you to compare lenders before committing. Here are four others worth considering.

2. Stratton Equities

Stratton Equities is a nationwide private money and non-QM lender that funds multifamily, commercial, mixed-use, and other investment properties.

They offer loan amounts from $100,000 to $5 million with LTVs up to 75–80% and no minimum credit score requirement, which makes them more accessible than traditional lenders or bank loans that require strong credit and extensive documentation.

We like that Stratton Equities is a direct lender with in-house funds and not a broker. This means you’re speaking directly with the people funding your loan and can get early confidence that your deal will move forward.

That said, their average closing time runs 21 to 25 days, longer than most hard money lenders. In contrast, Constitution Lending’s average closing time is around 7 to 14 days.

Stratton Equities also doesn't appear to offer an automated pricer or documents portal based on publicly available information, which means borrowers typically need to go through a loan officer to get quotes and move through the application process. For borrowers with tight deadlines, that may be a limiting factor.

3. Wilshire Quinn Capital

Wilshire Quinn is a bridge loan lender that funds non-owner-occupied multifamily and commercial properties with loan amounts from $200,000 to $10 million. Like Stratton Equities, Wilshire Quinn is a direct lender, so you’re unlikely to face last-minute rejections or complications caused by brokers.

They make lending decisions based on property value rather than borrower financials, and on their website, they state they can close in as few as 5 to 7 business days on straightforward deals.

However, we couldn’t find anything on their website about automated tools or systems used to generate instant quotes, term sheets, and pre-approval letters. It appears you need to speak with a loan officer and wait for these initial documents, which may introduce delays.

Another limitation is LTV. They typically cap out at 60 to 65% on multifamily properties, which means more cash out of your pocket at closing.

They also charge prepayment penalties and origination fees that aren't always reflected in the quoted rate, so make sure you're comparing the all-in cost rather than the interest rate alone.

4. Easy Street Capital

Easy Street Capital offers hard money and DSCR loans for residential and multifamily properties up to 20 units, including fix-and-flip loans and rental properties. Their flip loan program funds up to 90% of total project costs, and they're known for fast closings on straightforward deals.

Easy Street is a direct hard money lender, which reduces many of the complications and uncertainties associated with brokers.

They also offer the ability to refinance your hard money multifamily loan into a longer-term loan, simplifying the transition for investors.

That said, it’s unclear how quickly Easy Street can close. They don’t appear to have a publicly available automated pricer or documents portal, so borrowers need to engage directly with a loan officer to get firm numbers. This can introduce the same uncertainty around closing speed seen with many hard money lenders.

Easy Street also doesn’t provide clear information about its draw process or whether same-day funding for draws is available.

5. North Coast Financial

North Coast Financial is a direct private money lender with over 40 years of experience and more than $1 billion in loans funded. They lend on multifamily properties — including duplexes, triplexes, fourplexes, and larger apartment buildings — with loan amounts up to $10 million and LTVs up to 70–75%.

Unlike amortizing bank loans that require full income documentation and lengthy underwriting, they can approve loans the same day and fund in as few as 5 to 7 days.

The most significant limitation is geography. North Coast Financial lends exclusively in California. They also rely on a traditional loan officer consultation process rather than an automated system, so early-stage quotes and approvals aren't available instantly.

Secure Fast, High-LTV Hard Money Loans for Your Multifamily Property with Constitution Lending

Enter a few details about your deal into our automated pricer and receive instant quotes, term sheets, and pre-approval letters.