Almost every multifamily lender in California advertises fast, drama-free closing, but few can actually deliver.

That's because most multifamily lenders use the same slow, manual workflows as traditional banks. For example, it's common for your application to sit in a queue for days before a loan officer evaluates it. When they do, they ask for paperwork in batches rather than all at once. Then, appraisals get delayed because they order them too late.

Each delay creates a domino effect, stretching a one-week closing into more than a month.

In addition, some lenders will tell you for weeks that your application looks good and you can qualify, then reject your loan days before closing, after you've already committed your earnest money.

So, before choosing a multifamily lender in California, we recommend evaluating two factors:

- How quickly do they issue quotes, term sheets, and approvals? A lender's turnaround time on these documents is a reliable proxy for their closing speed. If it takes them multiple business days to simply produce a quote, they won't suddenly move faster as you approach closing. The fastest lenders have automated systems that turn these around instantly and avoid delays.

- Are they a direct lender or a broker? Brokers don't fund loans; instead, they submit your application to a third-party lender. It's common for them to think you qualify, but if the actual lender finds a problem near closing, you may get rejected after weeks of being told you're fine. A direct lender makes the final decision and can provide a reliable answer early in the process.

To help you make the right decision, we assess the best multifamily lenders in California against both factors.

We start with ourselves, Constitution Lending, because we believe we can close faster and more reliably than most lenders in the multifamily financing space (we show you how we do this below).

Then, we cover other lenders you're likely to encounter in your research, and compare their process to ours.

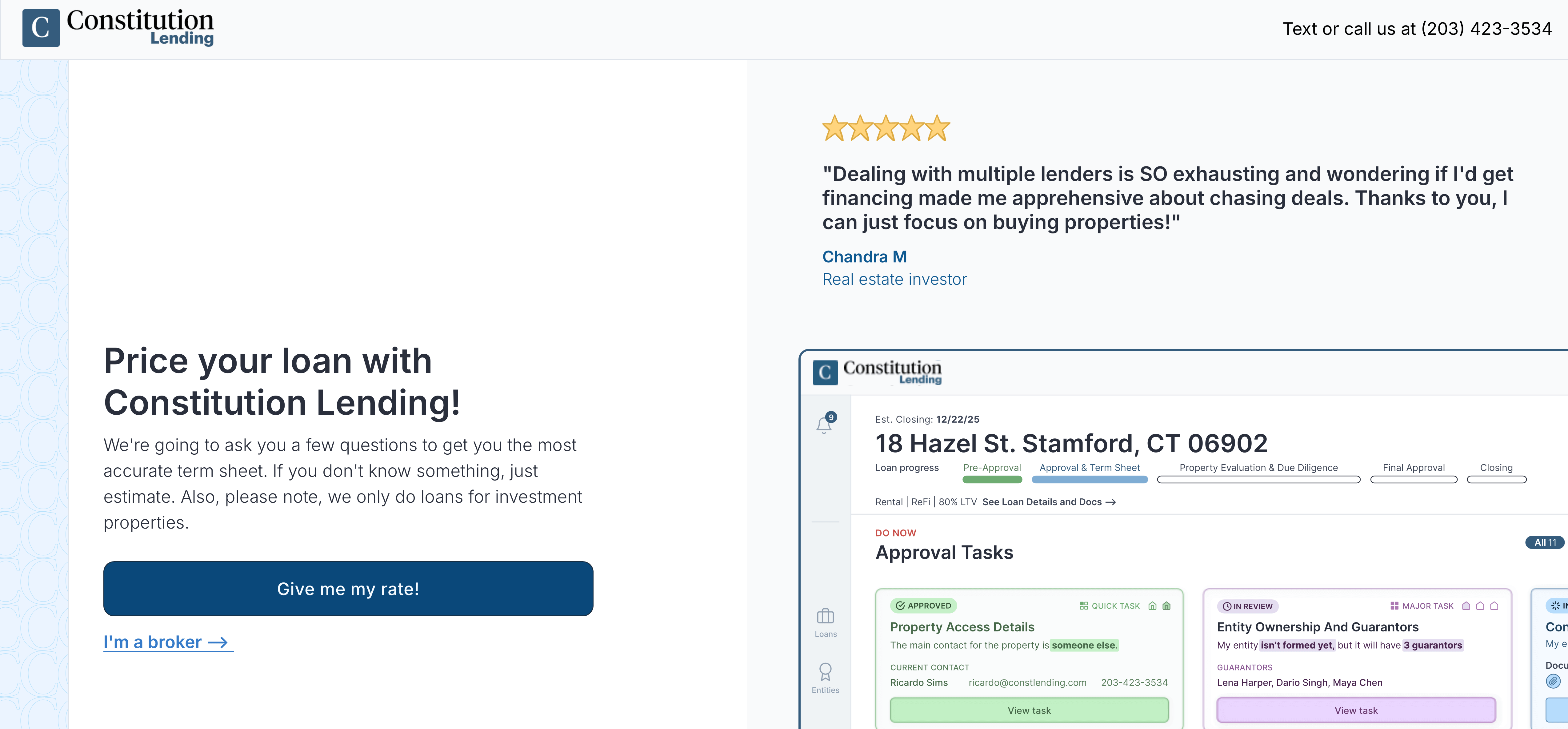

Use our automated multifamily loan pricer to generate quotes, term sheets, and pre-approval letters in under a minute.

1. Constitution Lending: Fast, Low-interest Multifamily Loans for California Investors

Before we were lenders, we were real estate investors purchasing, renovating, and leasing multifamily properties in the U.S, including California. During our real estate investing tenure, we lost out on millions of dollars in undervalued commercial real estate because of lenders who couldn't deliver on their promises.

We'd spend weeks sourcing an undervalued deal, get a loan under contract, and still lose the property to a cash buyer because our lender took 45 days to close.

Other times, we'd make it all the way to the final week, earnest money committed, everything supposedly on track, and get rejected because the lender found an issue they should have caught on day one.

We built Constitution Lending specifically to eliminate both of those problems. Most private lenders can tell you they're fast. But we're one of the few that have been in your shoes, lost deals because of slow lenders, and built our entire operation around making sure that doesn't happen to our borrowers.

To date, we've funded hundreds of millions of dollars in multifamily real estate loans in California, with originations spanning apartment buildings, mixed-use properties, value-add acquisitions, and ground-up construction.

How Our Automated Pricer and Documents Portal Allow Us to Close in 7 to 14 Days

Most lenders ask you to take their word on closing speed. We'd rather show you the automated tools we use internally to close quickly.

Enter your deal into our automated multifamily loan pricer, and you'll have a quote, term sheet, and pre-approval letter in under a minute. There's no need to book an appointment or wait days for a loan officer to call you back.

This reflects a core principle of ours: Rather than moving your application through the same manual, bureaucratic workflows of most lenders, we use automation to go from application to closing and eliminate delays.

Here's how the process works from start to finish:

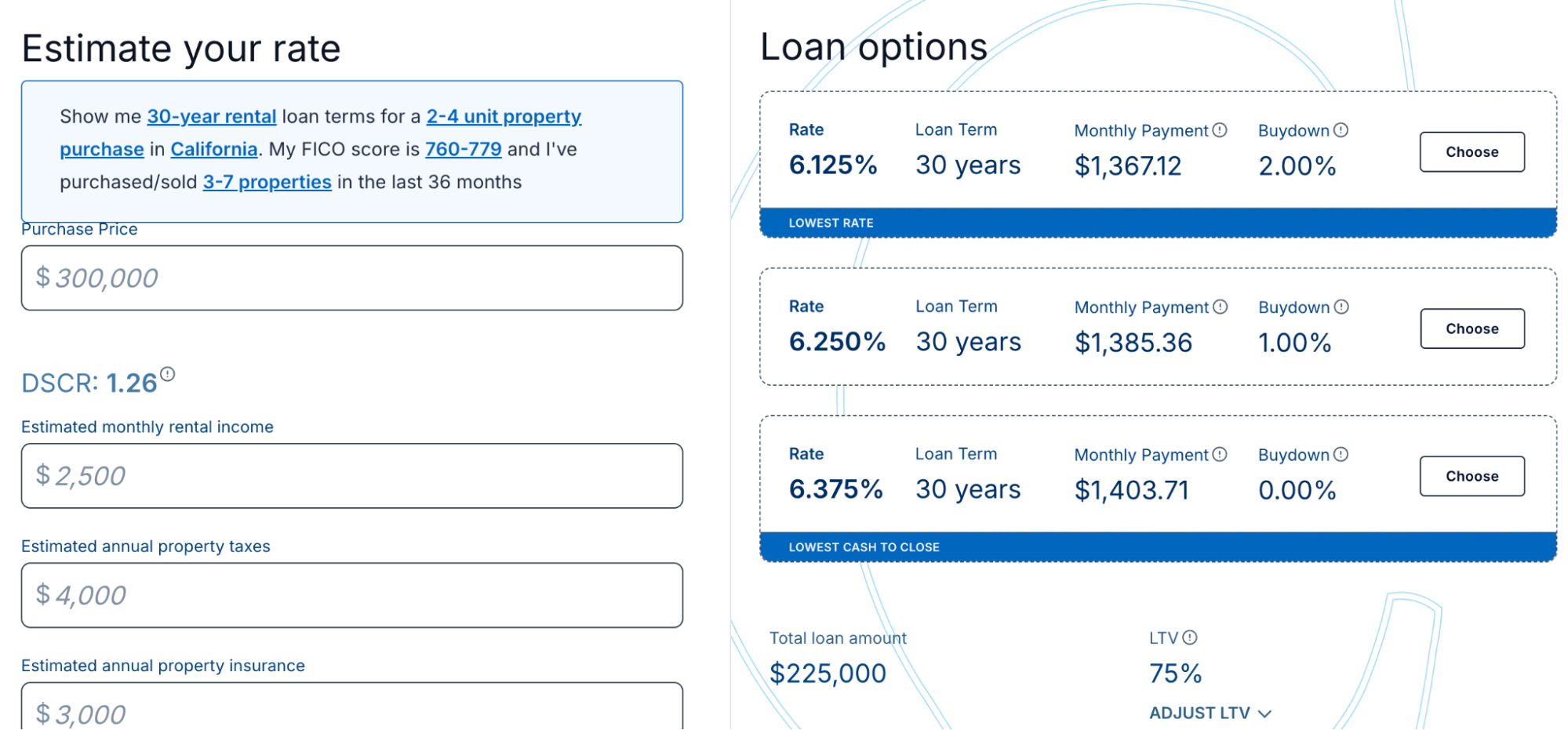

- Run your deal through our automated pricer by entering the property address, property type, purchase price, requested loan amount, and your credit score. It takes under a minute.

- The pricer instantly gives you three quotes showing your interest rate, monthly payment, loan term, maximum LTV, prepayment terms, and available buydowns.

- Run multiple scenarios before committing. Adjust the loan amount, LTV, and after-repair value to see how each variable affects your financing solutions in real time.

- Select your preferred quote and enter your contact details, including your name, email, and phone number. A term sheet, pre-approval letter, and copy of your quote are available to download immediately.

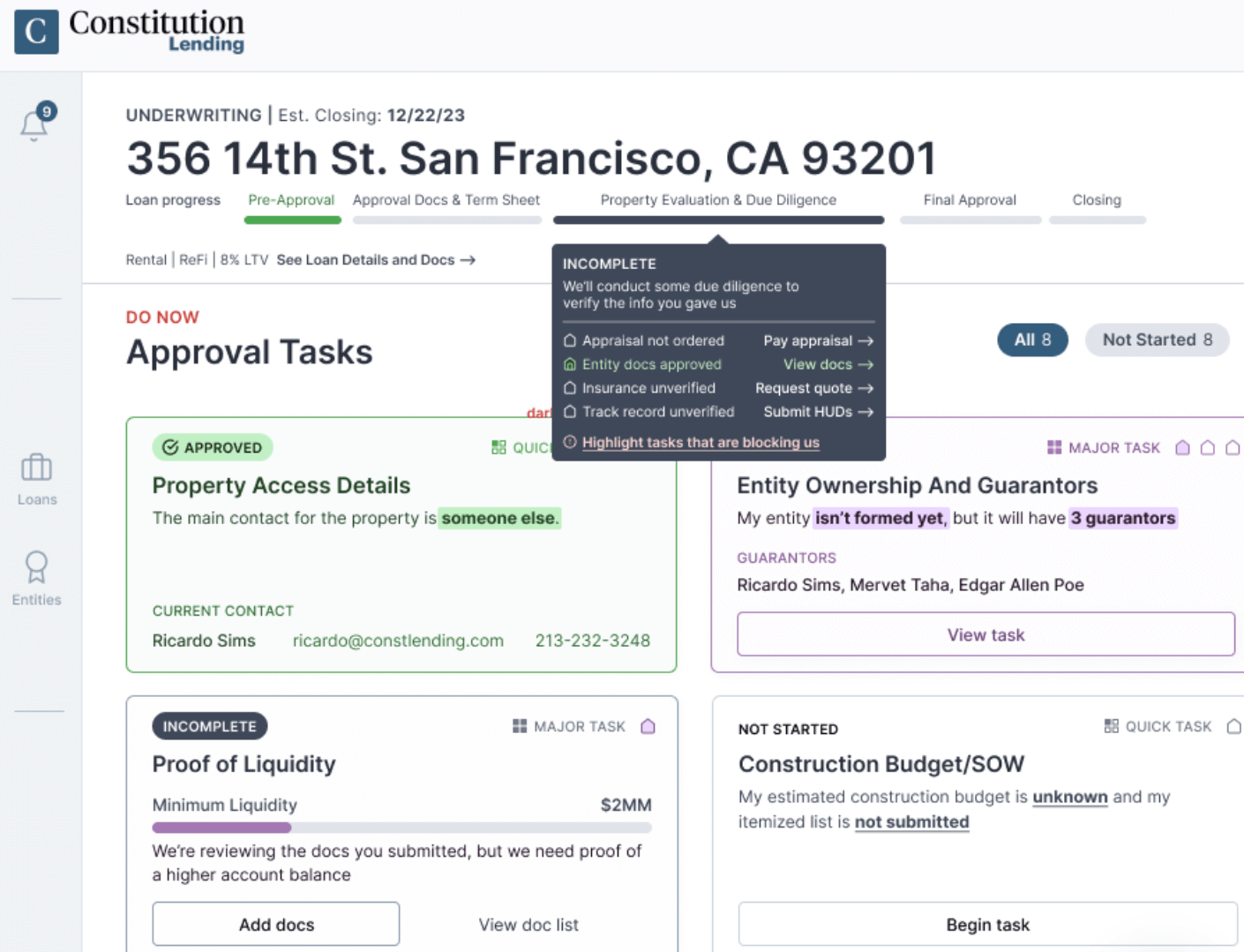

- You receive access to our documents portal at the same time. The portal lists every document required for your loan product (e.g., bank statements, entity documents, proof of insurance, renovation or construction budget), so you can submit everything in one shot rather than responding to a new email every few days asking for something else.

- Submit your documents and receive a definitive yes or no within a few hours.

- We close in 7 to 14 days. In cases where a borrower's earnest money is at risk because another lender couldn’t deliver, we have stepped in and closed within 4 days.

We Are a Direct Lender: No Brokers, No Last-Minute Rejections

The problem with brokers is that they don't fund loans. They submit your application to a third-party lender and wait for a decision, just like you do.

The feedback they give you early on is based on surface-level information (e.g., your credit score, the property type, a rough income figure), not a full underwriting review. The actual lender makes their decision based on complete documentation: rent rolls, leases, bank statements, DSCR calculations, and more.

As a result, it's common for a broker to miss problems with your file during their preliminary review and say that you can qualify, only for the lender to raise a red flag days away from closing with your earnest money already committed.

At Constitution Lending, you work one-on-one with the financiers of your loan. There are no brokers, intermediaries, or third-party underwriting decisions that can unravel your deal at the last minute. We have lent hundreds of millions of our own capital in multifamily real estate deals, so we know our underwriting criteria inside and out. When you submit your documents, we give you a clear yes or no within hours.

Essentially, working with Constitution Lending gives you certainty early in the application process that your deal will close smoothly.

You Can Refinance Into Long-Term Financing with the Same Team

Most short-term multifamily loans (e.g., fix-and-flip, construction, bridge financing) carry terms of 12 to 24 months. When that term ends, investors face a choice: sell the investment property or refinance into permanent financing.

If you plan to hold the property and generate rental income, you need a long-term exit lined up before your short-term loan matures.

Constitution Lending offers both. In addition to our short-term loan programs, we offer 30-year DSCR financing for investors who want to hold their multifamily housing long-term. DSCR loans are underwritten based on the property's cash flow rather than your personal income, W-2s, or debt-to-income ratio. You can learn more about current DSCR loan rates here.

This means you can acquire, renovate, or build a multifamily property with Constitution Lending and transition directly into long-term financing with the same team. That continuity has two significant advantages.

The team handling your refinancing already knows the property, your business plan, and your financial profile. They do not need to start from scratch, which can shave weeks off the refinancing timeline.

When you use two different lenders, your exit depends on a future approval from someone who has never seen your deal. If anything changes between your acquisition and your refinance, a new lender can decline, and you are left scrambling.

When you stay with Constitution Lending, we have already informally underwritten your exit when we approved your short-term loan, protecting your investment's profitability from the start.

Read more: DSCR Loan Pros and Cons: A Detailed Guide for Investors

Types of Multifamily Loans We Offer in California

Whatever your investment strategy is (e.g., buy and hold, fix and hold, ground-up construction, bridge the gap between sale and purchase), we have a multifamily financing solution to help you reach your goals:

- DSCR loans: 30-year, fixed-rate financing options underwritten on the property's cash flow. No W-2s, tax returns, or personal income verification required. With competitive rates starting as low as 6.75%, this is the most popular long-term loan product for multifamily investors.

- Bridge loans: Short-term bridge financing for acquisitions or transitional multifamily properties that are not yet stabilized.

- Fix-and-flip loans: For investors purchasing undervalued multifamily properties, renovating them, and selling for a profit.

- Construction loans: Commercial real estate loans for investors building new multifamily properties, with amortization into long-term financing available upon completion.

Secure Fast and Affordable Multifamily Financing with Constitution Lending

Use our automated pricer to generate instant quotes, pre-approval letters, and term sheets, and learn what interest rates and terms you qualify for.

2. First Foundation Bank

First Foundation Bank is a California-based lender with a dedicated multifamily lending team and a track record of over $1.5 billion in recent originations across the state.

They have funded multifamily real estate across major California markets, including apartment buildings and mixed-use properties. Their pitch to borrowers is straightforward: experienced lenders guiding you through the entire process, competitive rates and fees, and a dedicated point of contact from application to closing.

The main limitation is that First Foundation Bank operates as a traditional bank, which means their multifamily financing process follows a slow, manual process.

There is no automated pricing tool or self-serve origination system, so the loan approval timeline is dependent on the availability and workload of your assigned loan officer. Based on their publicly available information, there is no way to generate a quote, term sheet, or pre-approval letter independently before committing.

3. Banc of California

Banc of California is one of the larger multifamily lenders in California, positioning itself as the only midsize bank focused exclusively on the state.

Their multifamily financing programs cover properties of five units or more, mixed-use properties, and mobile home parks. They offer loan amounts ranging from $2 million to $35 million and up to 30-year amortization.

They also offer competitive rates on both adjustable and hybrid fixed-rate loan products, making them a practical option for investors with larger multifamily real estate portfolios.

However, the primary limitation is their loan minimums. With multifamily loans starting at $2 million, investors working with smaller 5 to 20-unit multifamily properties may fall below their threshold depending on the market.

On the process side, there is no publicly available automated pricing tool. Borrowers work through a Relationship Manager to receive preliminary terms, which introduces the same manual approval process and back-and-forth that slows down most banks. There is no way to self-serve a quote or pre-approval letter, making it difficult to evaluate their actual closing speed before committing.

4. Mechanics Bank

Mechanics Bank is a California community bank with a dedicated multifamily lending team serving investors throughout the state, including Northern California, the Central Coast, and Southern California.

Their loan programs cover multifamily properties and mobile home parks, and they can lend between $1 million to $25 million, with LTVs up to 75% and 30-year amortization. They offer both fixed and adjustable-rate options across 3-, 5-, 7-, 10-, and 15-year fixed terms, and their programs include no impound requirements and flexible step-down prepayment structures.

The trade-off is that Mechanics Bank operates as a traditional community bank, which means multifamily real estate lending decisions run through a conventional relationship-based process.

There is no automated pricing tool, self-serve quoting system, or documents portal. Borrowers work directly with a regional loan officer to discuss their financing solutions and move through the approval process, which introduces the manual timeline and back-and-forth that tends to extend closings well beyond what most multifamily investors need to compete for deals.

5. Fremont Bank

Fremont Bank is a Bay Area-based community bank. They have a dedicated multifamily lending division focused on financing apartment buildings and multifamily housing of five units or more throughout California.

Their loan product lineup covers purchase transactions, refinancing, equity lines of credit, and 1031 exchanges. They offer up to 30-year amortization and competitive loan rates on both fixed and alternative financing structures. They also highlight a streamlined appraisal process and local decision-making as part of their multifamily financing offering.

On the process side, Fremont Bank operates through a traditional relationship-based model. Borrowers speak with a Commercial Relationship Officer or Multifamily Lending Specialist to receive preliminary terms, and there is no publicly available self-serve pricing tool or automated origination system.

That approach may work well for straightforward refinancing transactions where time pressure is low. But for investors trying to close quickly on a competitive acquisition, the manual approval process introduces the same delays that make it difficult to beat cash buyers in the California multifamily real estate market.