Commercial lenders are supposed to be a faster, more accessible alternative to large banks and credit unions. Unlike consumer loans, they evaluate the property's financials rather than your personal income, debt-to-income ratio, or net worth, which in theory should make funding faster and approval easier.

In practice, however, most commercial lenders in California run their loans through the same slow, disorganized internal processes as large banks and credit unions. For example:

- You submit an application and have to wait days for a loan officer to call and provide a quote and term sheet.

- Your application sits untouched in a queue for days before an underwriter reviews it.

- Loan officers ask for documents in batches rather than upfront because they realize mid-process that they need something else.

- They order appraisals late in the process instead of at the start, causing delays.

Each delay stacks on top of the last, and a deal that was supposed to close in two weeks drags on for months.

A larger problem is that some lenders will tell you for weeks that everything looks fine, only to reject your application days before closing — after you have already committed your earnest money deposit.

So, we wrote this article to help you identify and avoid both of those problems. We examine 5 commercial real estate lenders in California based on their ability to close fast, starting with ourselves at Constitution Lending.

Generate instant quotes, term sheets, and pre-approval letters using our automated loan pricer and see what rates and terms you qualify for.

1. Constitution Lending: Fast, High LTV Commercial Real Estate Lending

Before founding Constitution Lending, we spent years on the other side of the table, acquiring and managing income-producing commercial real estate properties across the U.S. We know what it feels like to find a great deal, move quickly, and then watch it fall apart because your lender couldn't keep up.

We lost properties we had no business losing. Deals that were undervalued and within our budget slipped away because lenders promised two-week closings that dragged on for months.

We also had lenders tell us for weeks that our loan application was in good shape, only to surface a problem days before closing, with our earnest money already on the line.

That experience is what drove us to start Constitution Lending. We built our processes specifically around the problems that cost us deals as borrowers, so you don't have to go through the same thing.

To date, we have funded hundreds of millions of dollars in commercial real estate loans across the country, including multifamily, mixed-use, office, and retail properties.

How Our Automated Pricer and Documents Portal Allow Us to Close in 7 to 14 Days

Nearly every commercial real estate lender in California will tell you they close fast. In fact, that claim is so common that it has become meaningless.

A more reliable way to evaluate a lender's speed is to look at how quickly they can produce a quote, a term sheet, and a pre-approval letter. These are the simplest, most straightforward documents in the entire lending process, and if a lender takes multiple business days to produce them, that reflects their inefficiency. They won’t suddenly move faster as you approach closing.

At Constitution Lending, we built our process around automated in-house tools. We don't route applications through the same manual, bureaucratic workflows as other commercial lenders. This allows our borrowers to generate instant quotes, term sheets, and pre-approval letters, and close within 7 to 14 days.

Here is how our lending and approval process works:

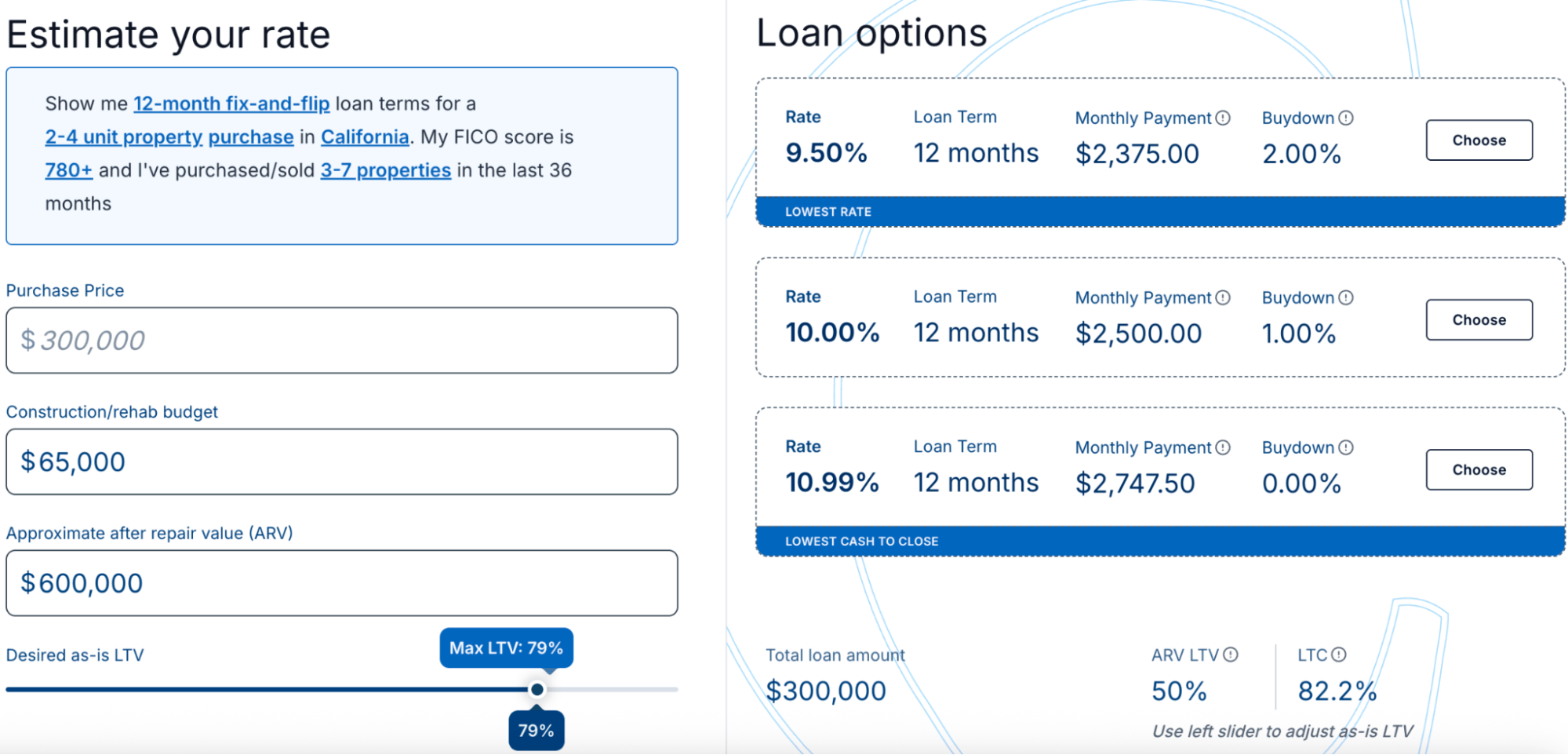

- Run your deal through our automated pricer. Enter the property address, property type, purchase price, requested loan amount, your credit score, and whether you want to purchase or refinance.

- The pricer instantly returns three financing options, each showing your interest rate, monthly payment, loan term, maximum LTV, prepayment terms, and available buydowns.

- Adjust the loan amount, LTV, and after-repair value in real time to see how different variables affect your options before committing.

- Select your preferred quote and enter your name, email address, and phone number. You can download your term sheet, pre-approval letter, and copy of your quote immediately.

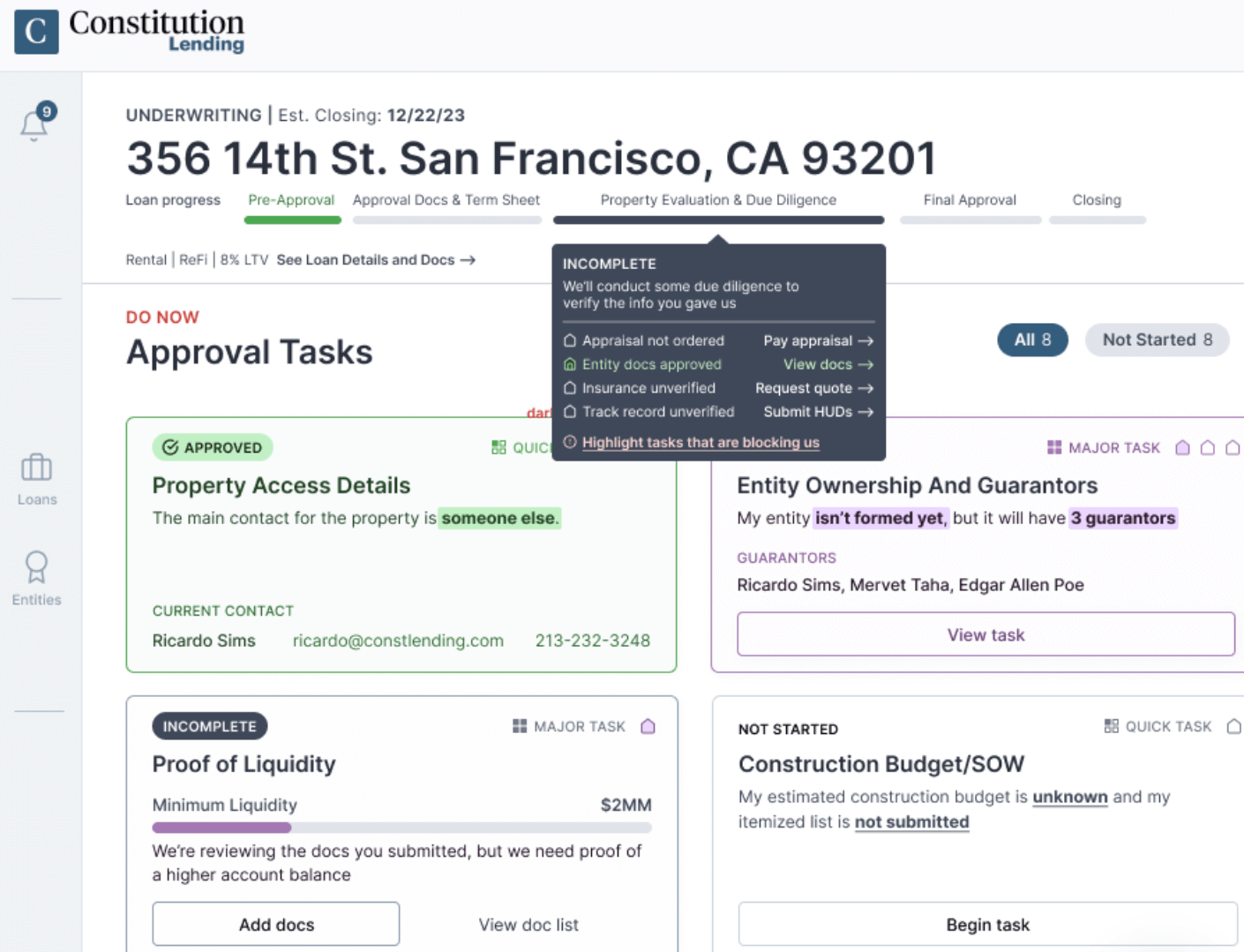

- You receive access to our documents portal, where you can view and upload all the necessary paperwork. Our documents portal speeds up closing because you can submit everything at once, rather than going back and forth with lenders requesting additional documents mid-process.

- Submit your documents and receive a definitive yes or no within a few hours.

- We close in 7 to 14 days. In situations where a borrower's earnest money was at risk because another lender failed to deliver, we have stepped in and closed within 4 days.

Read more: 5 Best Hard Money Lenders for First-Time Investors

We Are a Direct Lender: No Brokers or Last-Minute Rejections

Brokers are intermediaries, not the ones financing your loan. They review your file, give you early feedback, and say whether they think you qualify, but they are not the ones making the final decision. They submit your application to an actual lender and wait for an answer, just like you do.

The problem is that a broker's early assessment is based on surface-level information: a rough property description, a credit score, a general sense of the deal. The actual lender underwrites complete documentation such as operating statements, rent rolls, leases, bank statements, and full DSCR calculations.

This means a broker can spend weeks telling you that everything looks good while the real underwriting has not even started yet. If the lender raises an issue late on, you may get rejected days before closing, with your earnest money already on the line.

When you work with Constitution Lending, you work directly with the team deploying the capital. Because we have funded hundreds of millions of dollars of our own capital across commercial real estate transactions, we know exactly what we need to approve a loan and what will cause a problem. When you submit your documents, we give you a clear yes or no within hours, not a preliminary opinion based on incomplete information.

All in all, working with Constitution Lending gives you something brokers cannot offer: genuine certainty, early in the process, that your commercial real estate deal will close.

Read more: How to Get a Loan for an Apartment Complex Guide

Commercial Loan Programs We Offer in California

Regardless of your investment strategy, we have a loan program to support you:

- DSCR loans: Long-term, 30-year fixed-rate financing underwritten on the property's cash flow rather than your personal financials. No tax returns, W-2s, or income verification required.

- Bridge loans: Short-term financing for investors acquiring or repositioning properties that are not yet stabilized or generating full income.

- Fix-and-flip loans: Lending solutions for investors purchasing underperforming commercial properties, renovating them, and selling for a profit.

- Construction loans: Ground-up financing for developers building new commercial properties from scratch.

Get Your Commercial Property Financed in as Little as 7 to 14 Days with Constitution Lending

Get instant quotes, term sheets, and pre-approval letters through our automated loan pricer, and see the rates and terms you are eligible for.

2. Banc of California

Banc of California is one of the larger California-focused commercial real estate lenders, positioning itself as the only midsize bank dedicated exclusively to the state.

They offer on-balance-sheet lending programs across major commercial property types, including multifamily properties of five units or more, mixed-use buildings, and office buildings in Los Angeles and other major markets.

Their loan programs include permanent financing, bridge loans, structured finance, and business loans for qualifying commercial borrowers, with both fixed and floating-rate options available. Loan amounts range from $2 million to $35 million on multifamily deals.

The main limitation for most investors is their loan minimums. With multifamily loans starting at $2 million, smaller investors working with 5 to 20-unit properties may fall below their threshold.

On the process side, Banc of California does not offer a publicly available automated pricing tool. Borrowers work with a relationship manager to discuss their financing needs and receive preliminary terms, which means the back-and-forth that slows down the early stages of the approval process is likely.

There is no way to self-serve a quote, term sheet, or pre-approval letter, making it difficult to gauge how quickly they can actually move a loan from application to closing.

3. Provident Bank

Provident Bank is a California-based community bank offering commercial real estate loans on multifamily and commercial properties throughout Southern California and the Bay Area.

They finance a range of property types, including multifamily, office buildings, industrial, retail, and mobile home parks, with loan amounts starting at $350,000 and going up to $6 million on a standard basis, with larger loans considered on a case-by-case basis. They offer term loans with amortization up to 30 years and both adjustable and fixed rate options.

However, there are a few limitations worth noting. Provident requires full recourse on all commercial loans, meaning that if the deal goes sideways, the lender can pursue your personal assets beyond the collateral. They also require two years of tax returns, which adds documentation requirements that investors with non-traditional income structures may find restrictive.

For owner-occupied properties, their programs follow similarly strict income verification standards. Like most community banks, there is no automated pricing tool or self-serve application process. You will need to contact a commercial loan officer directly to work through your financing needs, and the loan approval process is handled manually from start to finish, which introduces a relationship-driven timeline that tends to slow things down.

4. CalPrivate Bank

CalPrivate Bank is a Southern California-based private bank offering commercial real estate financing across a wide range of property types, including multifamily, retail, office buildings, mixed-use, and industrial properties in Los Angeles and surrounding areas.

They position themselves as a relationship-focused alternative to large institutional banks, with approval based on the property’s income potential rather than standardized loan structures.

Business owners and investors can access flexible financing options covering purchases, refinances, and property improvements for both owner-occupied and investment properties.

The trade-off is that CalPrivate's relationship-driven model operates without a publicly available automated pricing system. There is no way to generate a quote or pre-approval letter independently. To discuss your financing needs and get preliminary terms, borrowers need to fill out a contact form and wait to be connected with a banking professional.

This can introduce delays in the approval process and make it difficult to close quickly.

5. California Coast Credit Union

California Coast Credit Union, known as Cal Coast, is a San Diego-based credit union offering commercial real estate loans for both owner-occupied and investment properties.

They finance office buildings, retail, industrial, multifamily, and specialty property types, and their team is described as Southern California-focused with strong local market knowledge.

Business owners and investors can access purchase, refinance, and business loan options, including term loans for qualifying commercial borrowers. Cal Coast positions itself as a long-term partner rather than a transactional lender.

The most notable limitation is membership eligibility. To borrow from Cal Coast, you must live or work in San Diego or Riverside County, which makes them inaccessible to investors based elsewhere in California.

Beyond that, like most credit unions, Cal Coast does not offer an automated origination process. There is no self-serve pricing tool, and business owners work directly with loan officers from start to finish to discuss loan structures and financing needs, which is consistent with the slower, manual approval process common across credit union commercial real estate lending.