There are four main reasons investors look for Groundfloor alternatives:

- Modest returns: According to Groundfloor's own website, their real estate debt investments generate returns of 4.75% to 8.25%. For context, REITs (real estate investment trusts) and total market cap index funds have historically returned around 10%.

- High default rates: Groundfloor's own published data puts their uncured default rate at 4.71%, but some investors with diversified portfolios have reported default rates of 24% to 35%. For context, the national average default rate on real estate loans is around 4%.

- Platform risk: Groundfloor has never turned a profit since its 2013 founding, and its auditors have issued a going concern warning in its SEC filings, which include a disclaimer about substantial doubt regarding the company's ability to continue operating. They have also accumulated a deficit of $55.8 million as of its most recent audited financials.

- Misaligned financial incentives: Groundfloor originates loans and then offloads them to investors. Groundfloor has no ongoing financial stake in whether the loan actually performs. Your capital is in the deal for the full term and theirs isn't. That creates a misalignment of incentives that makes it difficult for investors to have full confidence in the quality of loans on the platform.

In this article, we cover five Groundfloor competitors that address one or more of those limitations. We start with ourselves, Constitution Lending, which addresses all four, then cover other platforms you may encounter in your research.

Create a free investment account to explore our available real estate assets and start building passive income with as little as $1,000.

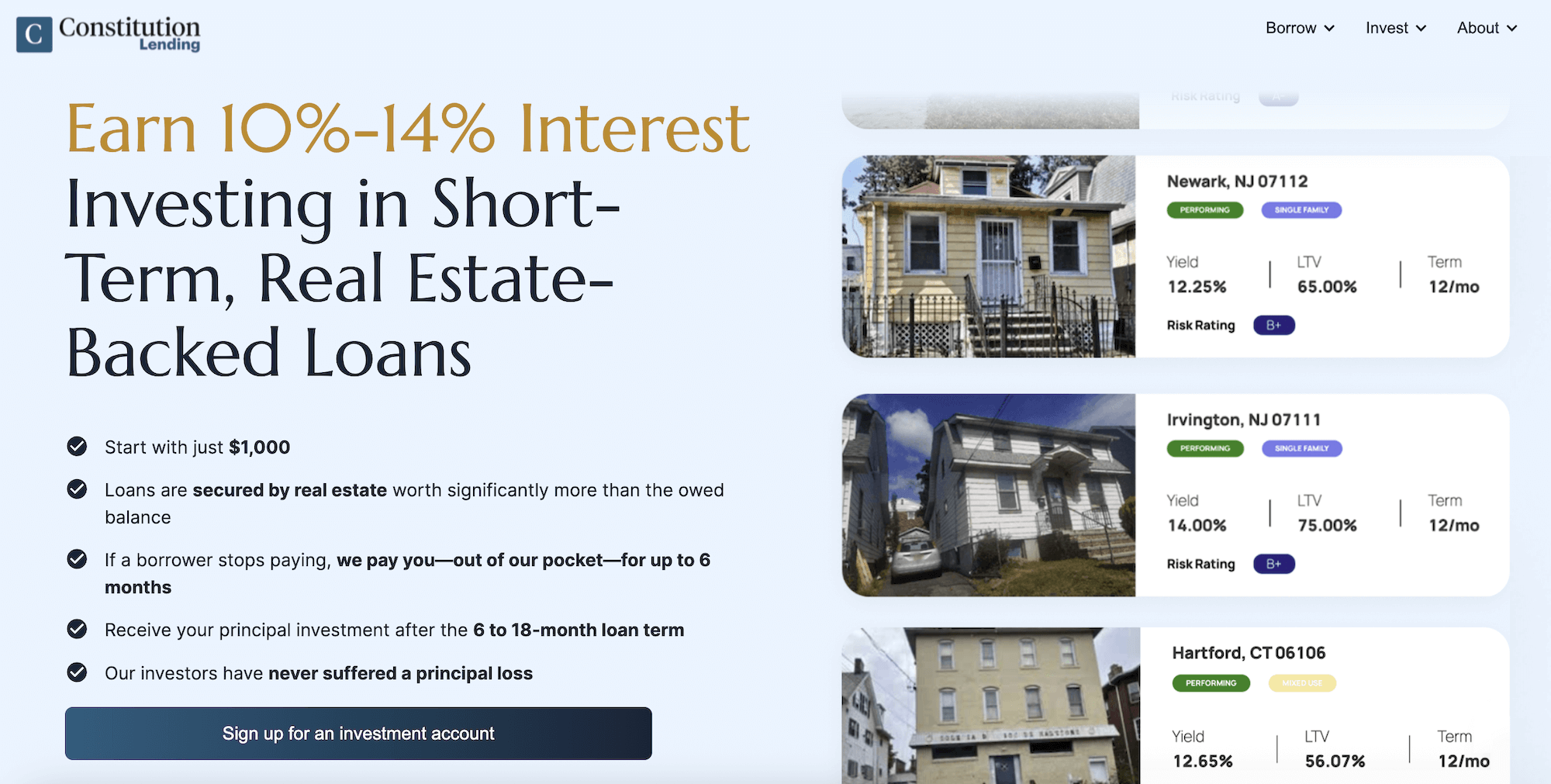

1. Constitution Lending: Earn 10% to 14% Interest by Investing in Real Estate Debt

Constitution Lending is a private money lender based in Connecticut. We deploy our own capital to fund short-term loans for real estate investors, primarily fix-and-flip, bridge, and construction financing on residential and multifamily properties.

Through our investor platform, individual investors can buy into those same real estate debt investments starting with as little as $1,000, a low minimum that makes it easy to diversify across multiple loans. They can then collect monthly payouts from borrowers at rates between 10% and 14%. Investors can also invest through a self-directed IRA for tax-advantaged returns.

Earn 10% to 14% Annually, Compared to Groundfloor's 3% to 5%

As we covered above, Groundfloor advertises returns of 4.75% to 8.25%, while total-market-cap index funds and REITs have historically returned around 10%.

In effect, Groundfloor investors are taking on an asset with less liquidity than a REIT or index fund while also earning less.

With Constitution Lending, investors earn between 10% and 14% annually in monthly payouts from borrowers.

The reason we can generate higher returns comes down to our closing speed. We close loans in 7 to 14 days, while traditional banks typically take 30 to 60 days. For a real estate borrower trying to beat a cash buyer on an undervalued property, that speed is worth paying a higher interest rate. Borrowers come to us specifically because we can move faster than anyone else, and that urgency is what drives the higher rate your investment earns.

We Have a Borrower Default Rate of Under 2%, Compared to Groundfloor's Reported 4.71% or Higher

Groundfloor claims a 4.71% uncured default rate, which is on par with the national average. But that figure may significantly understate the real picture. Multiple investors with diversified Groundfloor portfolios have publicly reported default rates of up to 35% on their own holdings.

At Constitution Lending, we have a default rate of under 2%, well below the national average.

That performance comes down to our underwriting standards and the quality of borrowers we work with. Over the past decade, we have built deep relationships with some of the most experienced and credible borrowers in the country, including established construction companies, institutional flippers, and professional rental investors with long track records of repayment.

That said, we also offer a payment guarantee on every loan. If a borrower misses a payment, we pay your monthly interest out of our own pocket for up to 6 months while we resolve the situation and return your principal and accrued interest.

Read more: How to Invest in Hard Money Loans: A Comprehensive Guide

We Operate a Profitable Lending Business, Reducing Your Platform Risk

Platform risk is worth considering for any investment platform because your returns depend not just on the underlying real estate assets performing, but on the platform itself remaining operational to service them, process your payouts, and manage any defaults. If a platform enters bankruptcy, your capital can be tied up for years with an uncertain outcome.

Groundfloor has never turned a profit since its founding in 2013. Their own auditors have formally flagged doubt about the company's ability to continue operating, and Groundfloor has accumulated over $30 million in losses since its founding. Their SEC filings include a disclaimer about this going concern risk.

PeerStreet, a platform with an almost identical business model, went bankrupt in 2023. When that happened, investors had no clear path to recovering their capital and were left waiting for a bankruptcy process to play out.

Constitution Lending operates with an entirely different business model. We are a direct lender with a profitable lending business that generates revenue on its own, independent of the number of retail investors on our platform. That is what makes platform risk a non-issue for our investors.

We Invest Alongside You on Every Deal

Most real estate platforms connect individual investors with borrowers and collect fees in the process, giving them no financial stake in whether those loans actually perform. Their incentive is to facilitate as many deals as possible, not to ensure every loan passes a rigorous vetting process or meets a high underwriting standard.

The result is a platform filled with low-quality investment opportunities where the borrower carries all the risk and the platform collects its fee either way. Your money is in the deal. Theirs is not.

We operate differently. We originate every loan on our platform using our own capital and maintain a 50% or greater stake for the entire term. When you invest in a loan through Constitution Lending, we are in that same loan alongside you from the closing date to the day it is repaid.

We cannot put a poorly structured loan on our platform without feeling the consequences ourselves. Every loan we approve is a decision we make with our own money on the line alongside yours, which is what gives our investors confidence in the quality of deals on the platform.

Additional Benefits of Investing in Constitution Lending's Real Estate Loans

Stronger Capital Protection by Investing in Real Estate Debt

When you invest in Constitution Lending's loans, you are secured by real estate assets worth significantly more than the total loan amount. We only originate loans where the outstanding balance does not exceed 75% of the property's value, protecting your investment from volatility in the real estate market and losses in property value.

For example, if you invest in a $750,000 loan on a $1 million property undergoing renovation, the borrower has $250,000 in equity sitting between you and any loss. The property's value can fall to $750,000 in a declining real estate market, and you still recover your full principal because you, the debt holder, are paid first and in full. The borrower has to lose their entire equity investment before your principal is affected.

All our loans carry a minimum borrower equity cushion of 25%, which is a core part of our underwriting standards and why our investors have never experienced a principal loss.

Get Your Full Principal Back in 6 to 12 Months

Most real estate investment platforms lock your capital up for years, making them illiquid and difficult to exit if your investment goals or financial situation change. Equity platforms like Crowd Street, Arrived Homes, and Fundrise have holding periods of 3 to 7 years with limited or no early-exit options.

Constitution Lending's loans run 6 to 12 months. At the end of the term, the borrower sells or refinances the property and repays the loan in full. You receive your entire principal back at that point and decide what to do next. You can reinvest in more real estate debt investments, diversify your investment portfolio into other asset classes, or withdraw.

Read more: Investing in Real Estate Notes: The Ultimate Guide for Investors

How to Start Investing with Constitution Lending

You can browse our loan portfolio before committing a single dollar. Here is how to get started:

- Open a free account by visiting constlending.com and entering your name and email. No accreditation status, credit check, or upfront deposit required — making it accessible to beginner investors and experienced ones alike.

- Browse active loans. Every loan currently available on our platform is visible on your dashboard, with key metrics including the property location, loan size, loan-to-value ratio, expected yield, term length, borrower credit profile, and our internal risk profile assessment.

- Review any loan that catches your attention. Click through to see the complete picture — outstanding balance, current and after-repair property valuation, the borrower's history with us, and how they plan to exit the loan.

- Link your funding source. Connect a personal bank account or a self-directed IRA. Investing through a retirement account is an option for investors who want to earn tax-advantaged passive income.

- Place your first investment. Pick a loan, enter your amount, and confirm. The low minimum of $1,000 makes it easy to spread your capital across several loans and build a diversified investment portfolio from the start.

- Receive monthly payouts. Borrower payments are debited to your account on the first of each month for the life of the loan. Once the term ends and the borrower repays, your principal is returned in full.

Earn 10% to 14% Interest Returns with Constitution Lending

Create a free investment account here to review our real estate debt investment options and earn 10% to 14% interest.

2. Willow Wealth (formerly Yieldstreet)

Willow Wealth, formerly known as Yieldstreet, is an alternative investment platform founded in New York that gives individual investors access to private real estate and other private market investment opportunities across real estate, private credit, art, venture capital, and other asset classes. Their Alternative Income Fund is open to non-accredited investors with a $10,000 minimum, while individual deal offerings require $10,000 to $25,000 and are limited to accredited investors only.

Returns are lower than they appear. Willow Wealth claims a net annualized return of 9.6% since inception, but this figure excludes active and defaulted investments. A CNBC investigation found that investors lost at least $78 million across 30 real estate deals, with four resulting in total losses and 23 more placed on an internal watchlist.

Sponsor and borrower quality have also been a persistent issue. As of December 31, 2024, 2.7% of their offerings have defaulted and 4.3% were modified, reflecting a platform that deploys capital across a wide range of asset classes and sponsors without the rigorous vetting and underwriting standards that Constitution Lending applies to every loan.

Platform stability is also a significant concern. The rebranding to Willow Wealth in October 2025 came directly in the midst of the CNBC investigation. The platform settled a federal class action for $9 million in 2025, and the SEC previously fined the company $1.9 million in 2023 for failing to disclose known collateral risks to investors.

Finally, downside protection is limited. Willow Wealth does not offer a payment guarantee, most investments carry multi-year holding periods with limited liquidity, and investors have no income protection if a deal underperforms or defaults. The fee structure also adds to the cost, with minimum investments from $10,000 to $25,000 compared to Constitution Lending's low minimum of $1,000.

Read more: Top 5 Yieldstreet Alternatives | Higher Returns & More Liquidity

3. Fundrise

Fundrise is one of the largest and most established real estate crowdfunding platforms in the country, giving both accredited and non-accredited individual investors access to diversified private real estate portfolios through their eREITs and interval funds.

Fundrise’s main strength is their low minimum investments, which start at $10. Their fee structure is also transparent at 0.15% annually, and investors can contribute through an IRA.

Returns have been modest relative to the real estate market and stock market benchmarks. Fundrise's Flagship Real Estate Fund has generated annualized returns of approximately 4.3% since inception, well below Constitution Lending's 10% to 14% and the historical average of broad market index funds. For investors coming from Groundfloor who are accustomed to real estate debt investments with fixed monthly payouts, Fundrise's equity-based structure and variable distributions represent a step backward in both predictability and yield.

Fundrise investors are equity holders in commercial properties and multifamily properties, which means they are paid last from any property sale and absorb losses in real estate assets before any debt holder is affected. In a declining real estate market, that payment order exposes investors directly to downside risk without any buffer.

Platform stability is not a concern here. Fundrise is a well-capitalized, established business with over $7 billion in assets under management. However, they don’t invest their own capital alongside investors, don’t offer a payment guarantee, and most funds carry multi-year holding periods with limited early redemption options, making them illiquid relative to Constitution Lending's 6 to 12-month loan terms. Platforms like EquityMultiple and RealtyMogul offer similar equity-based structures with similar limitations on downside protection and liquidity.

Read more: 5 Best Fundrise Alternatives for Higher Yields and More Liquidity

4. Crowd Street

Crowd Street is a commercial real estate investment marketplace that connects accredited investors with institutional-grade deals across office, multifamily properties, retail, and industrial commercial properties. Minimum investments start at $25,000, making it inaccessible for individual investors who prefer a low minimum entry point. The platform has facilitated over $4 billion in investments since its founding.

Advertised returns look strong on paper. Crowd Street claims a 15% to 20% annual return across completed deals. However, those figures reflect completed transactions and exclude deals that are still active or have gone into distress.

The platform's fee structure is built around listing fees collected from sponsors, meaning Crowd Street earns revenue regardless of whether individual deals perform. That misalignment of financial incentives contributed directly to the Nightingale scandal, in which a sponsor on the platform misappropriated tens of millions of dollars in investor funds, with Crowd Street having limited visibility because it had no financial stake in the outcome.

On borrower and sponsor quality, Crowd Street's vetting process has been questioned following the Nightingale situation. Sponsors manage their own deals independently, and investors are ultimately relying on third parties whose financial incentives are not aligned with theirs.

Platform stability has been tested by the Nightingale scandal, a subsequent federal class action, and ongoing reputational damage. Crowd Street depends on continued deal flow from sponsors to generate revenue, which creates its own platform risk.

Downside protection is the most significant structural limitation. Crowd Street investors are equity holders in commercial real estate, meaning they are last in line on any sale proceeds from those real estate assets. Most deals carry 3 to 5-year holding periods with no secondary market, leaving investors with an illiquid investment and no practical exit if market conditions deteriorate.

5. Arrived Homes

Arrived Homes is a real estate equity platform that allows retail individual investors to purchase fractional ownership in single-family rental properties and vacation homes starting with as little as $100. The platform handles all property management responsibilities, making it a fully passive income investment with no accreditation requirement — a popular entry point for beginner investors looking to access private real estate.

Cash payouts are modest. According to Arrived Homes' Q3 2025 performance data, single-family residential properties earned an average annualized dividend of 4%, and vacation rental homes earned an average of 2.4%. Those are the actual cash payments investors receive, well below Constitution Lending's 10% to 14% in monthly payouts from real estate debt investments.

Because Arrived is an equity platform rather than a lending platform, the default rate is not a directly applicable metric. The relevant risk is tenant non-payment, vacancy, and real estate market volatility, none of which are covered by any payment guarantee or debt-level cushion.

The primary limitation is downside protection and liquidity. Arrived investors own equity in individual real estate assets and are paid last from any sale proceeds after all debt is satisfied. Holding periods run 5 to 7 years, making them illiquid for investors whose investment goals require shorter time horizons, and there is no payment guarantee protecting passive income if a tenant stops paying or a property sits vacant.