Multifamily lenders are designed specifically to help real estate investors close on multifamily properties quickly, typically within 7 to 14 days.

Unlike a conventional commercial mortgage, approval is driven primarily by the property's financials rather than your personal income or debt-to-income ratio.

By contrast, banks often take 60 to 90 days to close and have strict requirements, including a net worth exceeding the property's value, high income, and low debt-to-income ratios.

Those advantages aside, the private multifamily lender you choose matters. Many multifamily lenders advertise fast closings but operate with the same slow, bureaucratic processes as banks, so it's common for them to take 30 or more days to close.

This long closing time makes it extremely difficult to compete with cash buyers for undervalued Florida real estate.

Here's what to consider to ensure your lender can close quickly and without drama:

- How quickly do they issue quotes, term sheets, and approvals? If a lender takes multiple business days just to issue a quote, don't expect the process to speed up as you near closing. The fastest lenders have automated systems that generate instant quotes and keep things moving fast through to funding.

- Are they a direct lender or a broker? Because brokers aren't the ones funding your loan, they don't have final say on approval. They can think you qualify, but if the lender finds a problem with your file near the closing date, you can get rejected after being assured everything is okay. Go with a direct lender because they deploy their own capital and can provide certainty early in the application process.

Below, we evaluate 7 multifamily lenders in Florida against these factors.

We start with ourselves, Constitution Lending. We'll cover how our automated pricer and documents portal allow us to close in 7 to 14 days, and why lending our own capital means borrowers never get blindsided by a last-minute rejection.

Then we cover other Florida multifamily lenders you're likely to come across in your research.

Use our multifamily loan pricer to play around with multiple loan scenarios and generate instant quotes, term sheets, and pre-approval letters.

1. Constitution Lending

A Direct Multifamily Lender That Closes in 7 to 14 Days

Before Constitution Lending, we were real estate investors ourselves, purchasing and leasing single-family and multifamily properties across the U.S. During those years, we lost out on millions of dollars in undervalued real estate investment opportunities because of slow lenders who couldn't deliver on their promises.

We'd spend weeks or months finding undervalued properties, move quickly, and still lose them to cash buyers.

Even when we did get a deal under contract, we would sometimes get rejected a few days before closing, after being told we qualified, and we would have to forfeit our earnest money deposit.

We built Constitution Lending specifically to eliminate both of those problems.

How Our Automated Pricer and Documents Portal Allow for Fast Closings

The reason most multifamily lenders miss their advertised closing times comes down to process. They're running loans through the same manual, bureaucratic workflows as traditional banks, just without the strict qualification requirements. The loan program structure is more flexible, but the execution is just as slow.

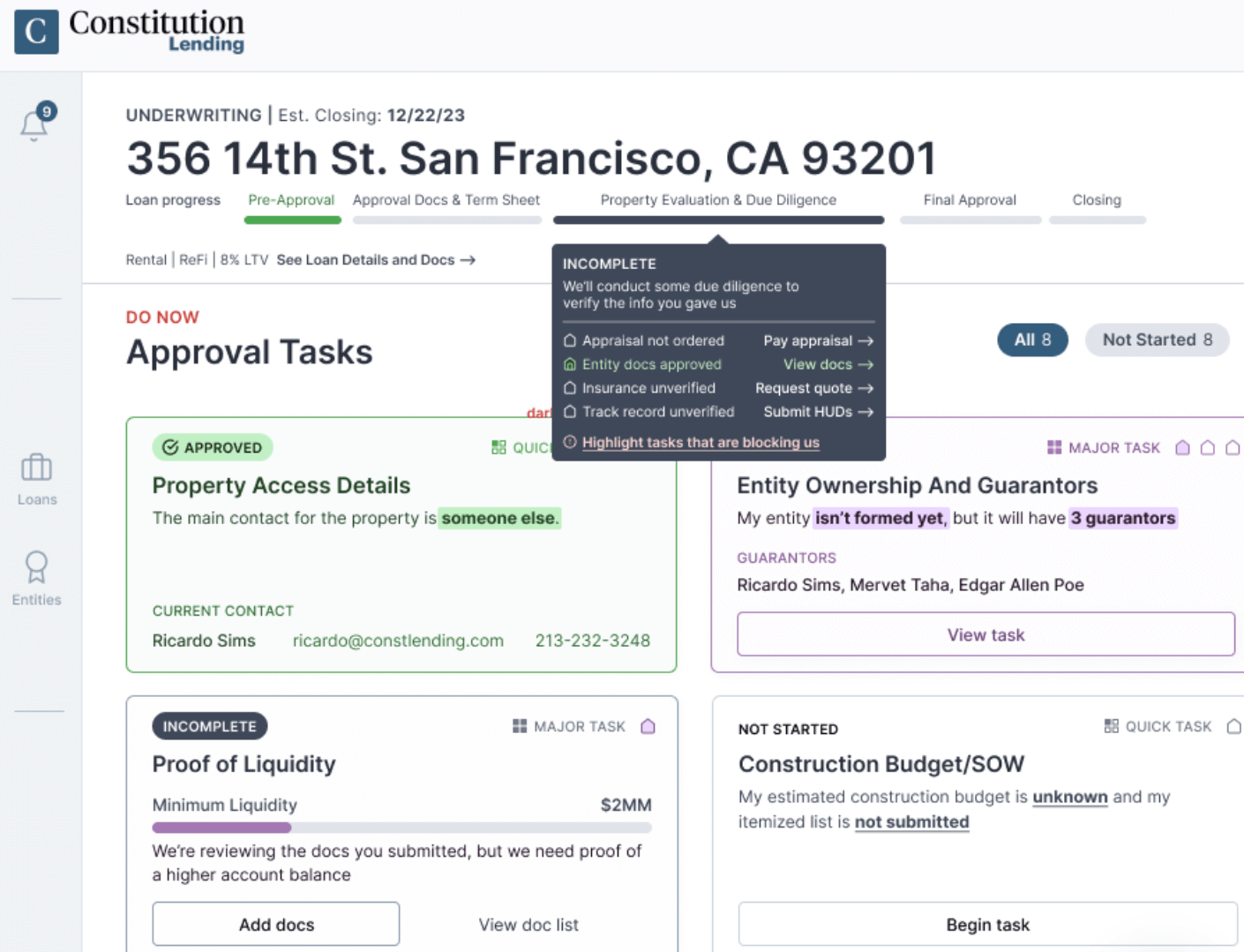

Applications typically sit in a queue for days before a loan officer reviews them. Then comes the documentation back-and-forth, where loan officers ask for information in batches rather than upfront, often realizing mid-process that they need something else. Appraisal delays add even more time on top of that.

We built our origination process differently, with automated tools at every stage so we close faster than most lenders.

Here's how it works from application to closing:

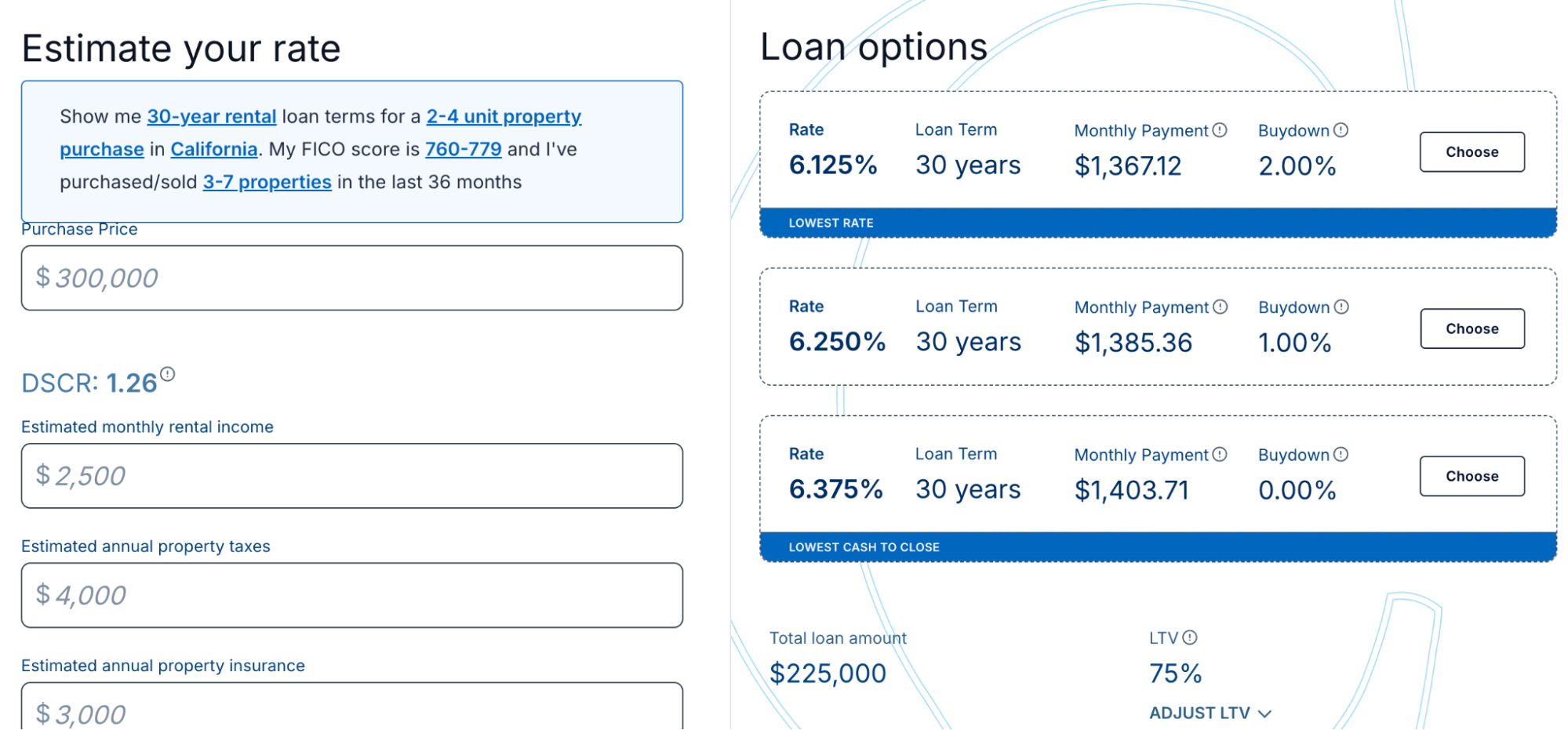

- Enter your deal into our automated pricer. Our pricer will ask for the property address, property type, loan type, purchase price, requested loan amount, and your credit score.

- The pricer immediately returns three quotes to choose from. Each one shows your interest rate, monthly payment, loan term, maximum LTV, prepayment terms, and available buydowns.

- We recommend running multiple scenarios before selecting a quote. Adjust the loan amount, LTV, and after-repair value to see how each variable affects your financing solutions in real time.

- Select your preferred option and enter your contact details. A term sheet, pre-approval letter, and copy of your quote are available to download on the spot.

- You'll receive access to our documents portal at the same time, which outlines exactly what paperwork we need for your loan program. For most multifamily loans, this includes bank statements, entity documents, proof of insurance, and a renovation or construction loan budget where applicable.

- Upload your documents to the portal, and within a few hours, we’ll send you a clear, definitive eligibility decision by email.

- We close in 7 to 14 days. In situations where a borrower's earnest money is at risk because another lender couldn’t deliver, we've stepped in and closed within 4 days.

We're a Direct Lender: No Surprises, No Last-Minute Rejections

As we covered earlier, the core problem with brokers is that they aren't funding your loan, which means they don't have a say in the final decision.

The broker may genuinely believe you'll qualify, but if the person or company funding the loan finds an issue with your file days before closing, something that happens frequently in multifamily real estate deals, you could face a last-minute rejection after being told everything was on track.

When you work with Constitution Lending, you work with a direct lender. We've deployed hundreds of millions of dollars of our own capital across market-rate multifamily and commercial real estate, which means we know our underwriting criteria inside and out.

When you submit your documents, we can tell you within hours whether your loan will close. If something is going to be a problem, we'll flag it immediately so you can address it before you've committed to anything.

Working with a broker also costs more. Broker fees and interest rate markups are added to a lender's base pricing, inflating your total borrowing cost. As a direct lender, our business loans reflect the actual cost of the capital with no intermediary markups.

You Can Refinance Into Long-Term Financing at the End of Your Term

Most multifamily hard money loans carry terms of 12 to 24 months. When the term ends, investors must sell the apartment building or refinance into permanent financing to generate long-term rental housing income.

Constitution Lending offers both. In addition to short-term hard money loans, we offer long-term DSCR financing for investors who want to hold their multifamily housing and build rental income over time.

DSCR loans are 30-year, fixed-rate loan products underwritten on the property's cash flow rather than your personal income, W-2s, or debt-to-income ratio. This article covers the pros and cons of DSCR loans in more detail.

Essentially, this means you can construct or renovate an apartment building or any multifamily property with Constitution Lending and move directly into long-term financing solutions with the same team. No need to start over with a new lender and underwriting team.

Secure Low-interest Multifamily Loans with Constitution Lending and Close within 7 to 14 Days

Use our automated loan pricer to see what interest rates, terms, LTVs, and buydowns you qualify for.

2. CoreVest Finance

CoreVest Finance is one of the larger private multifamily lenders operating in Florida, with over $10 billion in closed loans and financing on more than 172,000 units nationwide.

Their loan programs cover the full real estate investment lifecycle, including short-term financing and long-term DSCR rental loans. Loan amounts range from $1 million on multifamily DSCR loans up to $100 million on larger rental portfolios. All in all, CoreVest's scale and range of financing solutions make them a legitimate option for Florida multifamily investors with larger portfolios.

That said, their loan minimums can create access issues for smaller deals. Portfolio loans start at $500,000 and larger multifamily loans start at $1 million, which may exclude investors working with smaller apartment buildings.

Another limitation is that CoreVest doesn’t offer an automated pricing tool, which means borrowers initiate the process by submitting a loan request and waiting for a loan officer to follow up. This tends to introduce the same early-stage delays that can cost you deals.

3. GRP Capital

GRP Capital is another popular multifamily financing provider in Florida that you’ll likely come across in your research. They are a commercial mortgage broker offering financing solutions for a range of multifamily real estate and commercial property types.

They position themselves as a correspondent lender and advisor that matches Florida borrowers with lenders across their network, covering agency loans through Fannie Mae and Freddie Mac, CMBS non-recourse financing, and construction loans for multifamily projects.

The most important thing to understand about GRP Capital is that they are a broker, not a direct lender. As we covered earlier, brokers submit your application to third-party lenders and wait for a decision just like you do.

Their early assessment of whether you qualify is based on incomplete information rather than a full underwriting review, which means problems that surface late in the process can result in last-minute rejections after weeks of being told your loan is on track.

Working through a broker also adds fees and markups on top of the lender's base loan rates, increasing your total borrowing cost on what is already an expensive real estate investment market.

4. Arbor Realty Trust

Arbor Realty Trust is one of the most established names in multifamily lending nationally and has a meaningful presence in Florida. Their loan programs cover small balance multifamily loans from $1 million to $9 million, larger agency loans, HUD loans for market-rate and affordable housing, and healthcare and student housing financing.

They also offer bridge-to-agency financing, where the same team handles your short-term financing and transitions you into permanent agency financing.

For investors who qualify for agency financing, Arbor is a good option with strong partnerships across Fannie Mae, Freddie Mac, and HUD programs.

The main limitation is qualification. Agency loan programs require full income documentation, strong debt-to-income ratios, and rigorous underwriting standards that many individual Florida real estate investors may struggle to meet. This can be a problem for investors with non-W2 income or complex financial profiles.

It’s also worth noting that Arbor doesn’t offer DSCR loan products like Constitution Lending, so investors who cannot qualify for agency financing will need to look elsewhere.

There is also no self-serve automated pricing tool. Borrowers must request a quote and work with a loan officer to receive preliminary terms before knowing where they stand, which can delay closing.

5. Banyan Commercial Capital

Banyan Commercial Capital is a Boca Raton-based commercial mortgage advisory firm with over $2 billion in closed transactions across multifamily real estate and other commercial property types in Florida.

Banyan positions itself as an independent advisor with no financial ties to any lender or capital source. Their financing solutions span permanent loans, construction financing, CMBS non-recourse products, mezzanine debt, preferred equity, and joint venture equity, with a focus on deals in the $10 million to $50 million range across the Florida multifamily market.

Like GRP Capital, however, Banyan Commercial Capital is a broker and advisor, not a direct lender. They source capital from banks, life companies, Fannie Mae, Freddie Mac, HUD, CMBS conduits, and private lenders on your behalf.

Their independence from any single lender is a genuine advantage in terms of market access and financing solutions, but it introduces the same structural risks we outlined earlier. The actual lender makes the final underwriting decision, and last-minute rejections after weeks of positive feedback can mean losing your earnest money deposit.

For Florida multifamily investors who need a fast, reliable close with certainty of execution from day one, working directly with the lender funding your loan removes that risk entirely.