The advantage commercial mortgage lenders offer over traditional banks is speed. The fastest ones can close in 7 to 14 days, while banks normally take 30 to 60 days, sometimes longer.

That speed matters everywhere, but especially in New York City, where the real estate market moves extremely fast. Cash buyers are everywhere, and sellers typically receive concrete cash offers within days of listing.

However, not all commercial lenders can actually deliver fast closings. Many lenders advertise 7 to 14-day closings, then take 30 days or more.

That's because they use the same inefficient and bureaucratic processes as banks. Applications routinely sit in queues for days, loan officers go quiet, appraisals fall behind, and title work piles up.

Our advice is not to take a lender at their word on closing speed and to instead evaluate them against the following factors:

- How quickly do they respond with pricing and approvals? If a lender is slow to issue quotes and term sheets, don't expect them to speed up as you approach closing. The same inefficiencies that slow down their initial response usually persist. The most efficient lenders can issue instant quotes and same-day term sheets.

- Are they lending their own capital? Working with a broker raises the risk of last-minute rejections because you aren't talking to the decision-maker on your loan (we explain how this happens in more detail below). Direct lenders deploy their own capital and make their own decisions, so they can assess your eligibility and catch issues early.

Using those two factors as our benchmark, here's a look at the top mixed-use commercial real estate lending firms in New York City.

We start with ourselves, Constitution Lending. We cover how our automated pricer and documents portal help you close faster than most commercial lenders while eliminating last-minute drama and complications.

Then we cover a few other New York City-focused lenders you'll likely encounter in your research, and compare them on both factors.

Use our automated pricer to generate instant quotes, term sheets, and pre-approval letters.

1. Constitution Lending

A Direct Lender for NYC Mixed-Use Properties

Before founding Constitution Lending, we were real estate investors operating in Connecticut, New York, and other competitive markets, flipping residential, multifamily, and mixed-use properties. Throughout those years, we dealt with lender after lender who couldn't deliver on their promises.

Lenders would say they close in one week, and take two months. We'd receive approvals after submitting our documents, only to get rejected at the last minute and have to forfeit our earnest money deposit.

So we built Constitution Lending to solve those problems. We designed our origination process with automated tools to close in 7 to 14 days and to give borrowers certainty early on that their loan will close.

Here's what borrowers say about working with us:

Factor #1: You Can Close in 7 to 14 Days Using Our Automated Pricer and Documents Portal

The reason most commercial lenders fall short of their advertised closing times is that they use the same bureaucratic processes as large banks.

That's why we tell borrowers not to take any lender's word on closing speed. Instead, test it by seeing how quickly they come back with quotes and approvals. If this takes long, you can expect delays to continue through closing.

Lenders who can turn around instant quotes, term sheets, and pre-approval letters have built the kind of infrastructure that moves fast throughout the entire process.

Here's how our process works from application to closing:

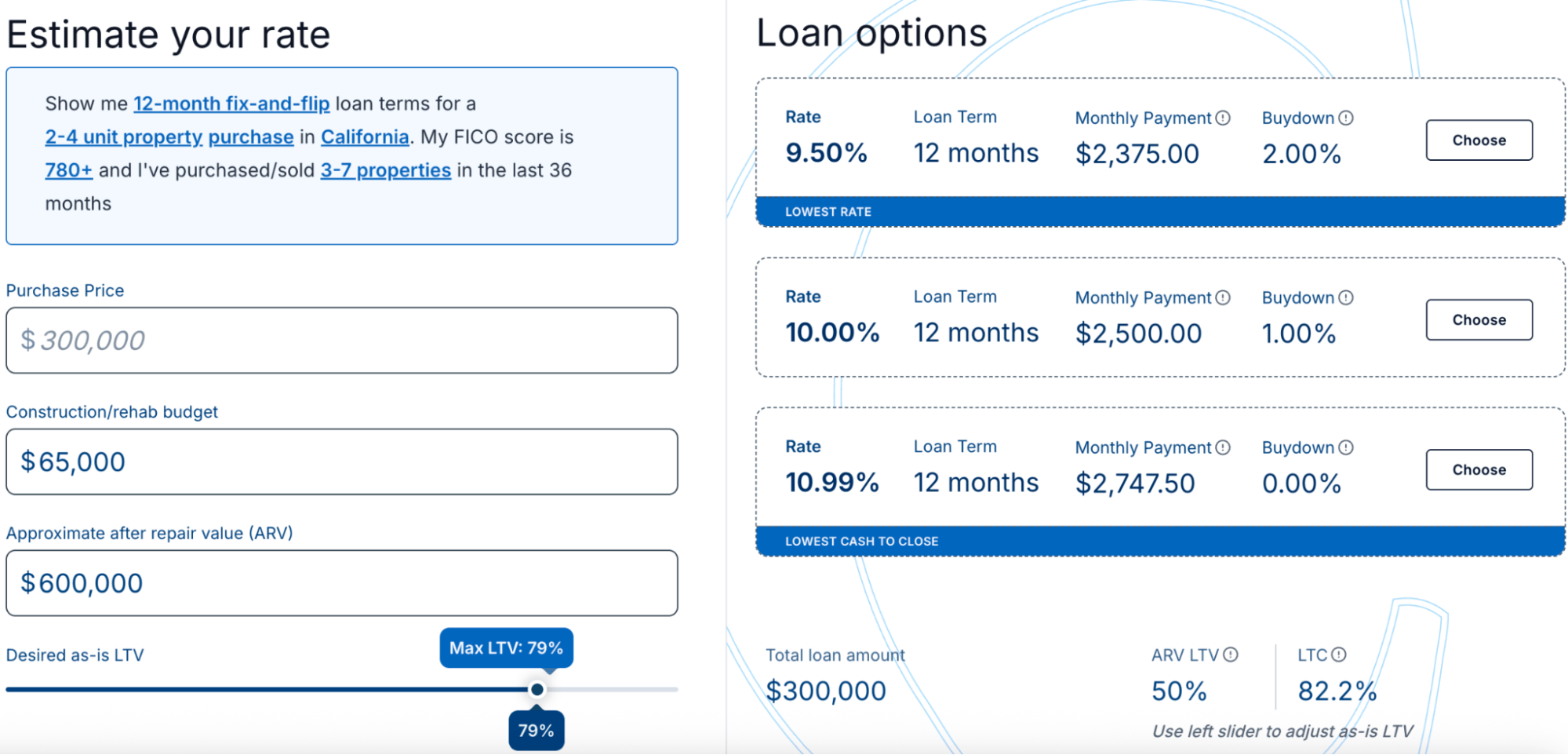

- Enter your deal into our automated pricer. You need to enter the property address, property type, loan type, purchase price, requested loan amount, and your credit score.

- The pricer immediately returns three quotes to choose from. Each one shows your interest rate, monthly payment, loan term, maximum LTV, prepayment terms, and available buydowns.

- We suggest running multiple loan scenarios before choosing a quote. Adjust the loan amount, LTV, and after-repair value to see how different variables affect your financing options in real time.

- Select your preferred option and enter your contact details. A term sheet, pre-approval letter, and copy of your quote are available to download on the spot.

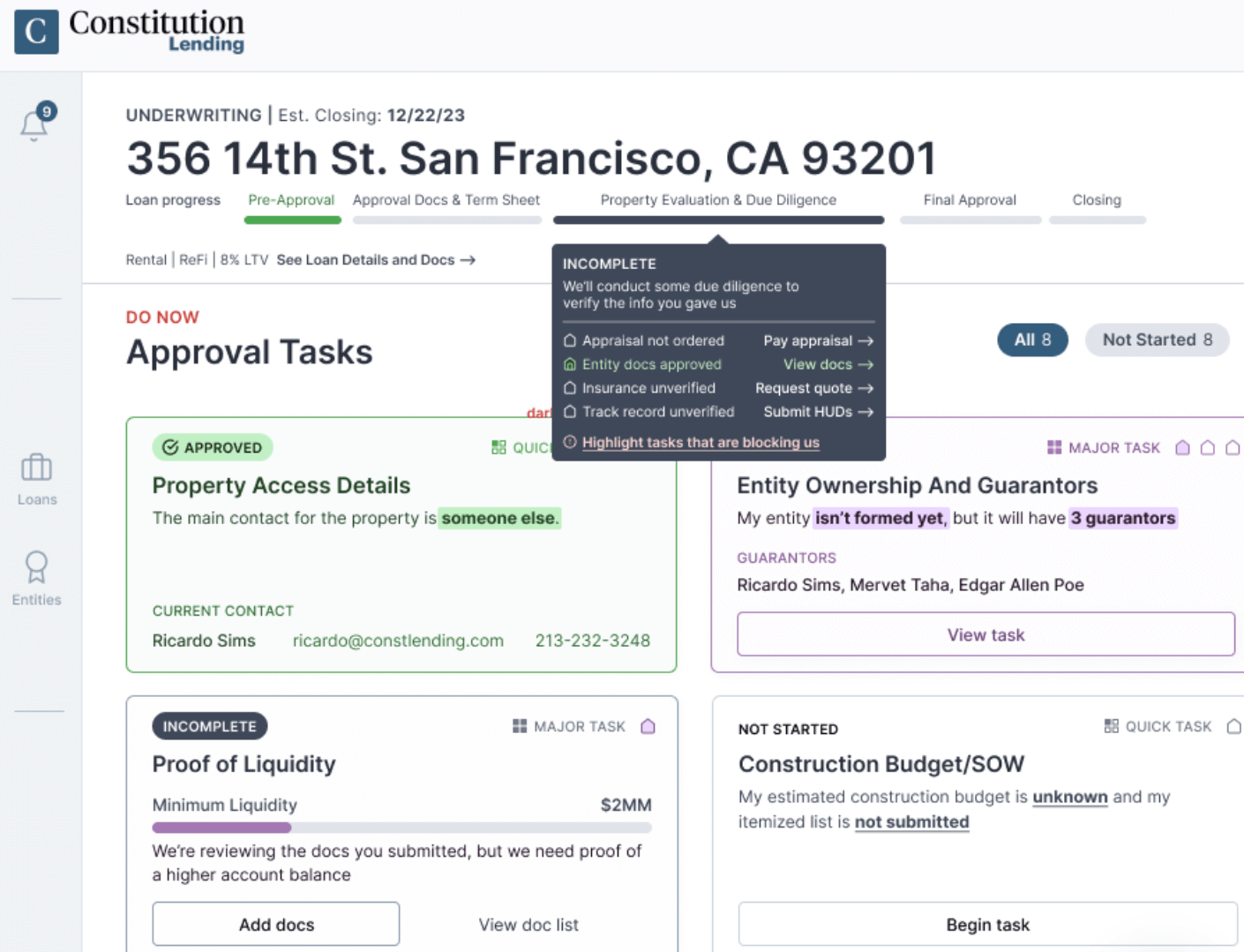

- You'll receive access to our documents portal at the same time, which outlines exactly what paperwork is required for your loan type. For most mixed-use loans and commercial real estate loans, this includes bank statements, entity documents, proof of insurance, and a renovation or construction budget where applicable.

- Submit your documents and receive a definitive answer within a couple of hours.

- We close in 7 to 14 days. In extreme situations where a borrower's earnest money deposit is at risk because another lender dropped the ball, we've stepped in and closed within 4 days.

Read more: How to Get a Loan for an Apartment Complex Guide

Factor #2: We Are a Direct Lender Which Means No Last-minute Rejections or Drama

As we touched on earlier, the problem with brokers is that they don't finance the loan themselves, so they don't have the final say on approval.

Brokers might provide early assurances that you can qualify, but if the lender finds problems after that and near the closing date (which is common in complex mixed-use deals) you can get rejected late on after being told you qualify.

We're a direct lender and have lent hundreds of millions of dollars, so we know our underwriting criteria inside and out.

That means we can review your file and give you a definitive answer within hours. If something in your application is going to be a problem, we'll tell you early, so you can fix it before applying again. We won't tell you on the day of closing and after you've already committed earnest money.

It's also worth noting that brokers introduce additional costs. Broker fees and interest rate markups get layered on top of a lender's base rates, inflating your all-in borrowing cost. As a direct lender, we offer more affordable loan options than brokers.

Bonus: Refinance Into Long-Term Financing At The End of the Term

Most commercial hard money loans carry terms of 12 to 24 months. When the term ends, investors need to either sell the property or refinance into permanent financing.

Constitution Lending offers both short-term commercial loans and long-term DSCR financing for investors looking to earn rental income from their properties.

DSCR loans are 30-year, fixed-rate real estate financing options underwritten on the property's cash flow rather than your personal income, W-2s, or debt-to-income ratio. You can learn more about the pros and cons of DSCR loans here.

This means you can fund your acquisition or renovation with Constitution Lending and immediately transition to long-term financing, avoiding the need to start over with a new lender and underwriting team.

Secure Fast and Affordable Mixed-Use Property Financing with Constitution Lending

Use our pricer to pull instant quotes, find the right loan for your deal, and see what interest rates and terms you qualify for.

2. JP Morgan Chase

JP Morgan Chase has a dedicated commercial real estate division serving NYC investors, with a specific mixed-use property loan product that covers both purchase and refinance transactions. Their loans start at $1 million and go north of $25 million, and they offer both fixed- and adjustable-rate structures.

On the surface, the product looks competitive. Their commercial real estate lending operation has local teams in New York, and the breadth of their banking services, treasury, cash management, and business credit makes them attractive to most real estate investors.

In practice, however, two things stand out.

First, their advertised closing timeline is 45 days. That's their own number for a "fast, efficient" process. This is longer than most commercial lenders advertise and is often too slow to win a deal without a very patient seller.

Second, there's no way to get a quote or term sheet without talking to someone. JP Morgan's Commercial Term Lending process starts with a loan application form or a call to their team. There's no automated pricer, no instant quote, and no self-serve documents portal. You're working on their timeline from day one.

Their long-term financing is Fannie Mae and Freddie Mac agency debt, which means investors who want to refinance into a 30-year hold need to qualify on personal income and debt-to-income ratios. They don’t offer long-term DSCR loans.

JP Morgan is an option for larger investors managing commercial portfolios who already bank with them and don't need to close in under two weeks. For individual investors who need speed, their process isn't built for that.

3. HAB Bank

HAB Bank is a New York-based community bank with a commercial lending program that explicitly covers mixed-use properties, including land purchases, building acquisitions, and renovations across New York, New Jersey, and Connecticut. They position themselves as a relationship lender: experienced professionals who customize loan structures around each borrower's situation rather than fitting them into rigid product boxes.

One area where HAB genuinely stands out is SBA loan programs. They offer SBA 7(a) financing, which can be a legitimate advantage for owner-occupied commercial borrowers — businesses that will occupy at least 51% of the commercial space they're purchasing. SBA 7(a) loan programs can go up to 90% loan-to-value ratio, which is notably higher than most conventional commercial mortgages, and they carry favorable long-term structures.

That said, SBA financing adds a layer of complexity that extends well beyond the bank's own underwriting. Approval requires both HAB's internal credit review and a separate federal process.

For a straightforward investment purchase (e.g., a buyer acquiring a mixed-use building purely as an income-producing asset, without occupying any commercial space themselves), SBA financing isn't an option.

HAB also follows the same bureaucratic path as any bank: a loan officer relationship, a customized underwriting process, and a traditional timeline. There's no automated pricing tool, instant quote functionality, or documents portal.

HAB is worth considering if you're an owner-occupant who can benefit from their SBA program. For investors acquiring non-owner-occupied mixed-use properties and competing against cash offers, the timeline and process fall short.

4. Dime Community Bank

Dime Community Bank is one of the most established multifamily and mixed-use lenders in the New York metro area. They have deep roots in the local market and a loan portfolio that, until recently, was heavily concentrated in mixed-use commercial loans.

Their mixed-use and multifamily loan programs offer terms up to 10 years with amortization up to 25 years. They also offer short-term bridge and mezzanine financing for more complex transactions, giving them a broader product menu than most community banks of their size.

There are two things worth knowing before you approach them, though.

First, Dime is actively pulling back from commercial real estate. As of 2025, management has been working to reduce the bank's CRE concentration — specifically targeting a reduction in multifamily loans from 37% of the loan portfolio down to the 25–30% range. A bank in active portfolio reduction mode is one that's selectively tightening its underwriting. Deals that might have gotten approved a few years ago are getting more scrutiny today.

Second, their process is fully relationship-driven. Dime's approval path runs through an interest form, a consultation with a relationship manager, and traditional bank underwriting. Their 10-year loan cap also means they're not a permanent financing destination — at maturity, investors face refinancing risk and the cost of starting over with a new lender, at whatever rates exist in that environment.

They don’t offer a DSCR exit pathway, an automated pricer, or self-serve tools. For investors who already have a relationship with Dime and are buying stabilized properties with clean documentation and no urgency, they remain a capable lender. For anyone who needs to move fast or wants a clear path to long-term fixed financing, it’s important to consider these constraints.

5. Arbor Realty Trust

Arbor Realty Trust is one of the largest multifamily and commercial real estate lenders in the country.

Their bridge loan programs cover multifamily, mixed-use, and other commercial properties, with loan amounts ranging from $10 million to $100 million, loan-to-value ratios of 65% to 75%, and flexible terms of one to three years with extension options.

They're also a full-stack agency lender, offering Fannie Mae, Freddie Mac, FHA, HUD, and CMBS financing. This means they can theoretically handle both the short-term bridge and the long-term permanent exit under one roof.

Their CMBS program specifically is worth understanding. CMBS loans are securitized and sold on the secondary market, which can enable non-recourse structures and accommodate deal profiles that don't fit traditional agency boxes. For larger, more complex commercial transactions, that flexibility matters. For smaller mixed-use deals, CMBS adds underwriting complexity without much corresponding benefit.

Construction loans are also part of their program: Arbor's construction financing accommodates mixed-use projects with a portion of income generated from non-residential components.

The main limitation is straightforward: There's no automated pricing tool or self-serve origination system. Borrowers work through loan officers and regional teams. Getting preliminary terms takes a relationship and lead time, not a one-minute form and an instant quote.

Their long-term financing follows the same pattern as other agency lenders: Fannie, Freddie, and HUD rather than DSCR loans. Investors with non-W2 income who want to refinance into 30-year real estate financing based on the property's cash flow won't find that option here.

Arbor is a serious lender for institutional investors managing large multifamily and commercial portfolios who need scale and a bridge-to-agency execution path. For individual investors working on smaller NYC mixed-use deals where speed, flexibility, and loan size matter more than institutional infrastructure, they're not the right fit.